A while ago, I wrote a piece called Our Financial Independence Assumption…What About Taxes? In it, I took a close look at what our taxes might look like if we were to live off dividend income. Since tax season is upon us (this year you have to file your 2017 income tax return by April 30), I thought it would be fun to run some scenarios to prepare us for financial independence. What if we were financially independent in 2017 and lived off dividend income? What happens to our 2017 Canadian income tax return?

Rather than base everything on assumptions, I will use some actual numbers from 2017.

Disclaimer: I’m not a tax specialist. This post is simply my interpretation of the Canadian income tax system. Please consult a tax specialist regarding your income tax.

2017 Spending – Real Data

Rather than use $40,000 as our annual spending, we will take a look at real data from 2017. In 2017 we spent a total of $51,144.77, excluding any business expenses.

A quick breakdown of some of our 2017 expenses

- We spent $33,887.68 in Necessities

- We spent $17,257.09 in Give, Play, Education, and Vacations

- We spent $1,104.08 in fitness for Baby 1.0 (swimming)

- We spent $3,905 in childcare (preschool) for Baby T1.0

- We spent $1,492.20 in fitness for Baby T2.0 (swimming, children’s gym)

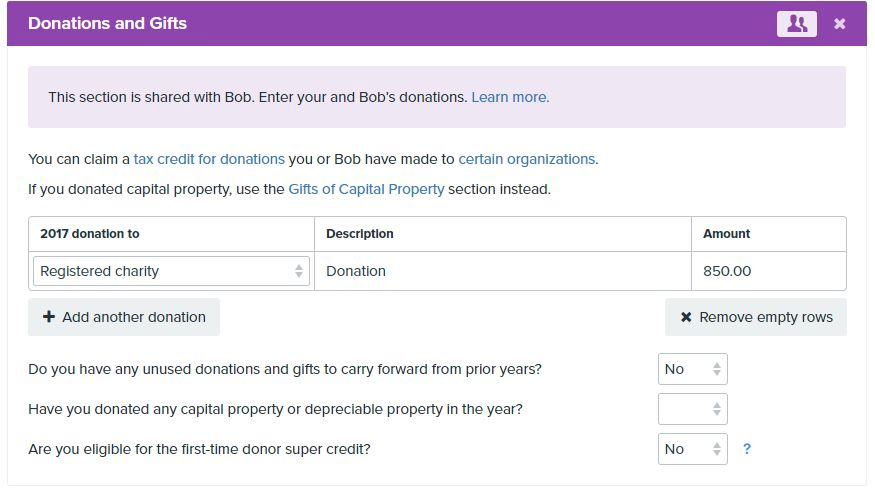

- We donated $850 to charities (about $250 less than previous years because local Christmas Bureau didn’t match us up with a family in time for Christmas giving).

For the sole purpose of this article, we will use these real data from 2017 on our tax returns.

Income Tax Assumptions

We will pretend that we were financially independent in 2017 and lived off dividend income for the entire year. This means we needed to have received $51,144.77 in dividend income in 2017. For mathematical simplicity, we will use $55,000.

Once we are financially independent, we won’t be contributing to RRSP. So another assumption is that we made $0 in RRSP contribution in 2017. (And therefore, no RRSP deduction).

We plan to withdraw from our RRSPs and perhaps collapsing our RRSPs before we turn 71. There are tax consequences when withdrawing money from the RRSP. Therefore, we need to come up with a withdrawal strategy. Our RRSP withdrawal strategy is to split the withdrawal amount between the two of us. Below are the RRSP withholding tax rates:

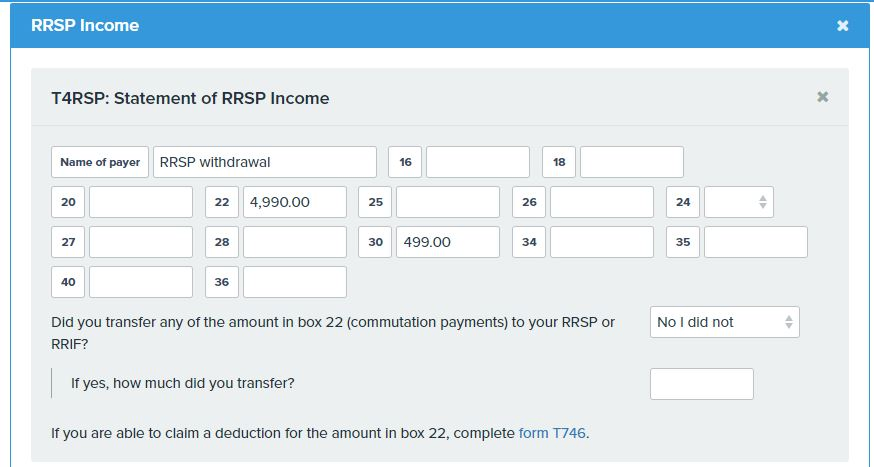

We will assume that we are splitting our RRSP withdrawals. We plan to withdraw less than $5,000 a year to limit the withholding tax amount. Therefore, for the 2017 income tax return simulation, we will assume that we each withdrew $4,990 in 2017 while paid 10% ($499) in withholding tax. We would net $4,491. The $4,491 is then considered as active income when filing for 2017 income tax return.

Our 2017 Dividend Income Breakdown

In 2017 we received a total of $14,834.38 in dividend income. The dividend income breakdown between RRSP, TFSA, and Taxable as below:

- RRSP: $5,589.46 or 37.68%

- TFSA: $5,760.84 or 38.83%

- Taxable: $3,484.08 or $23.49%

But this breakdown will probably quite different once we are financially independent.

For this particular post, we will assume that we received $55,000 in dividend income to cover our 2017 expenses. Since we withdrew $4,990 each from our RRSPs, we needed $45,020 in dividend income from TFSA and taxable accounts. And let’s assume the TFSA and taxable account dividend income breakdown was roughly 30-70, or that we received $13,520 in dividend income from TFSA’s and $31,500 from taxable accounts.

Let’s also assume that Mrs. T and I had a 50-50 split on the $31,500 taxable dividend income, or $15,750 each. And all the dividends received were eligible dividends.

2017 Taxes – Scenario 1

For the first scenario, we will assume that we didn’t make any active income and we had no business income in 2017. The numbers would look like:

My Taxable Income:

- $15,750 in dividend income

- $4,491 from RRSP withdrawal

Taxes I Paid:

- $499 from the 10% RRSP withholding tax

Mrs. T’s Taxable Income:

- $15,750 in dividend income

- $4,491 from RRSP withdrawal

Taxes Mrs. T Paid:

- $499 from the 10% RRSP withholding tax

Our Deductions:

- $1,104.08 in Fitness for Baby 1.0

- $3,905 in Childcare (preschool) for Baby T1.0

- $1,492.20 in Fitness for Baby T2.0

- $850 donation to charities

Note 1: In 2017 the children arts & fitness credits were eliminated federally but some provinces still have such credit. In BC we still have a $500 credit per child.

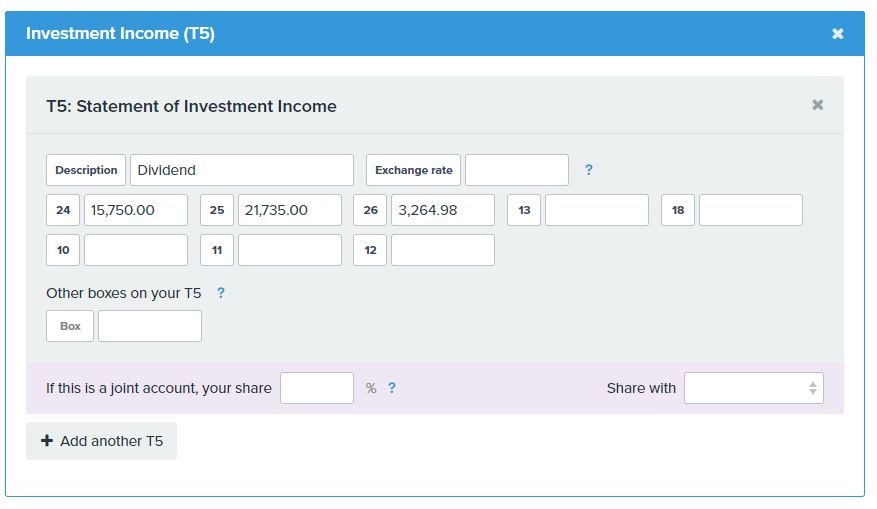

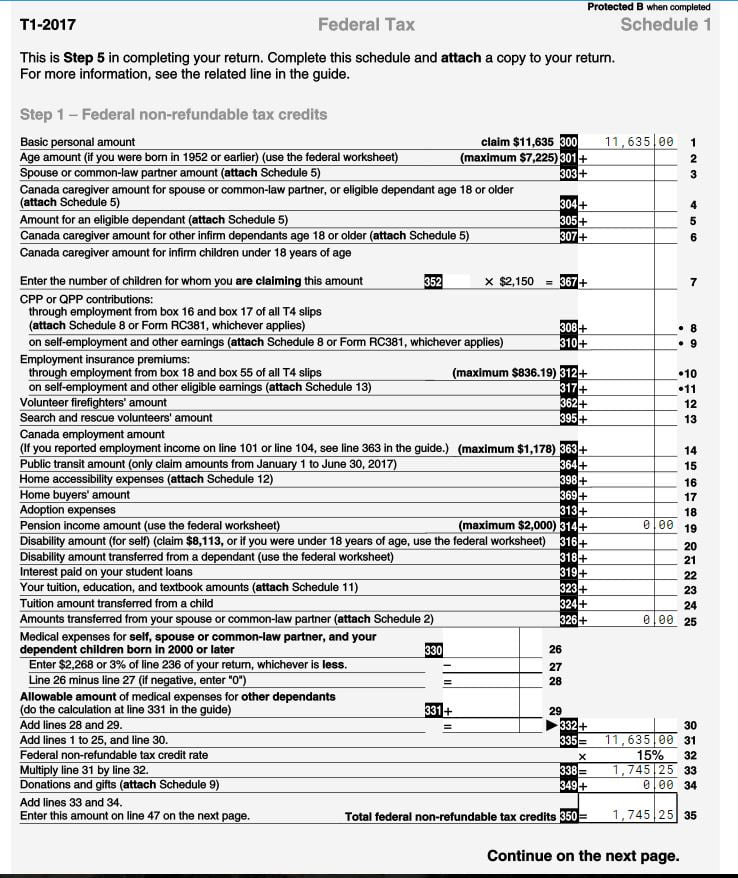

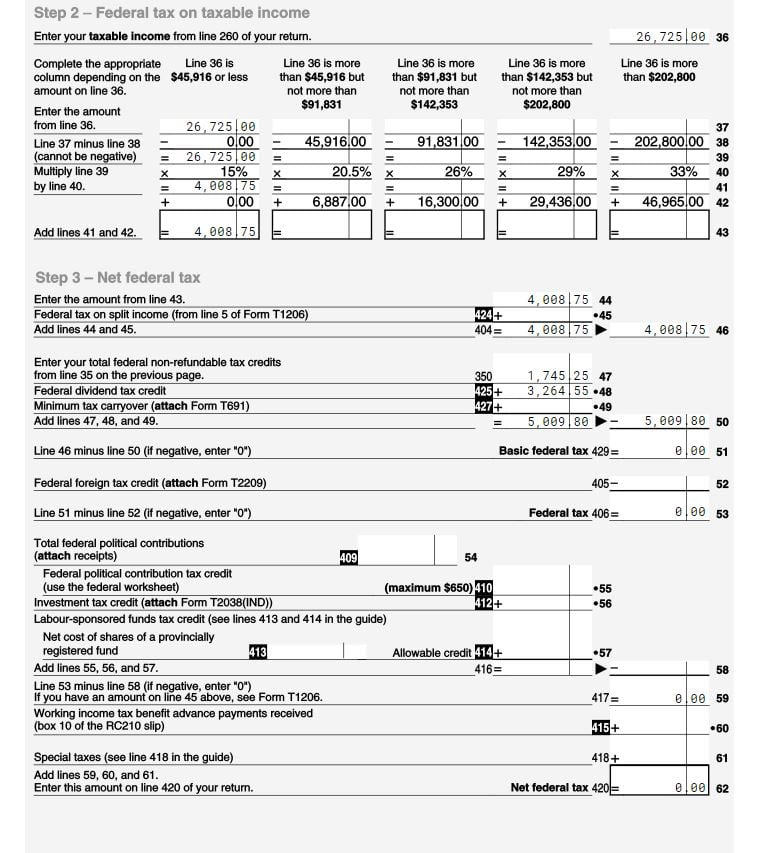

Note 2: Based on the 2017 enhanced dividend tax credit rates, we need to gross-up $15,750 dividend received by 38% ($21,735). We would get a dividend tax credit of 20.73% of the actual dividend amount received ($3,264.98).

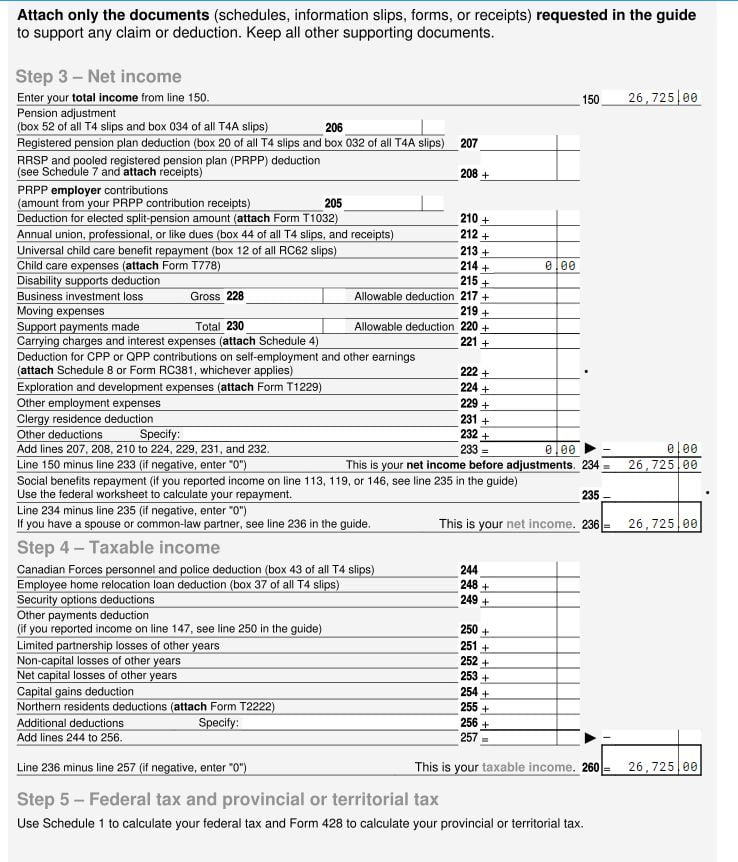

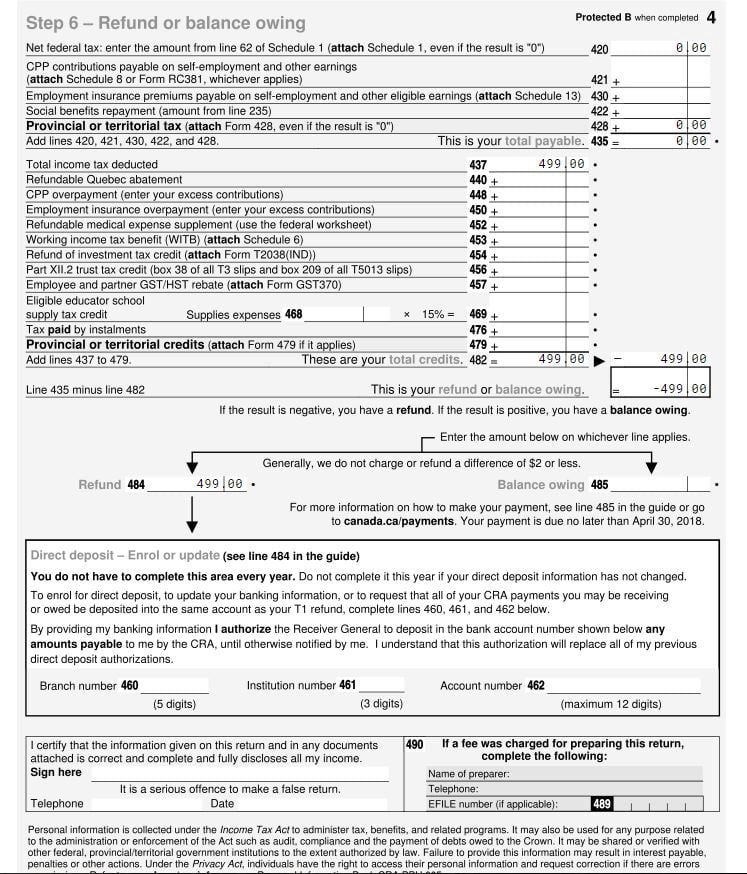

I used Simple Tax to find out what our tax returns would look like for 2017.

And our T1’s would look like:

And Schedule 1

Both of us would be able to recover the $499 RRSP withholding taxes!

Scenario 1 Total Income Summary: $55,000

- $13,520 in dividend income from TFSA’s

- $31,500 in dividend income from taxable accounts

- $8,982 from RRSP withdrawal

- $998 from tax refund

Scenario 1 Total 2017 Taxes Paid: $0

And we paid $0 in taxes. We would also be eligible to receive an estimated $823.92 in tax-free Canada child benefit per month ($9,993.84 per year).

Nice!

How much would our portfolio need to worth to receive this kind of dividend income? For TFSA’s to produce $13,520 in dividend income and taxable accounts to produce $31,500 in dividend income, at 4% yield rate, we would need our TFSA portfolio to worth $338,000 and taxable portfolio to worth $787,500. Or $1,125,500 in total.

2017 Taxes – Scenario 2

In scenario 2, let’s assume the same numbers as scenario 1 but Mrs. T and I made a modest $10,000 revenue each in our side businesses.

My Taxable Income:

- $15,750 in dividend income

- $4,491 from RRSP withdrawal

- $10,000 in business income

Taxes I Paid:

- $499 from 10% RRSP withholding tax

Mrs. T’s Taxable Income:

- $15,750 in dividend income

- $4,491 from RRSP withdrawal

- $10,000 in business income

Taxes Mrs. T Paid:

- $499 from 10% RRSP withholding tax

Our Deductions:

- $1,104.08 in Fitness for Baby 1.0

- $3,905 in Childcare (preschool) for Baby T1.0

- $1,492.20 in Fitness for Baby T2.0

- $850 donation to charities

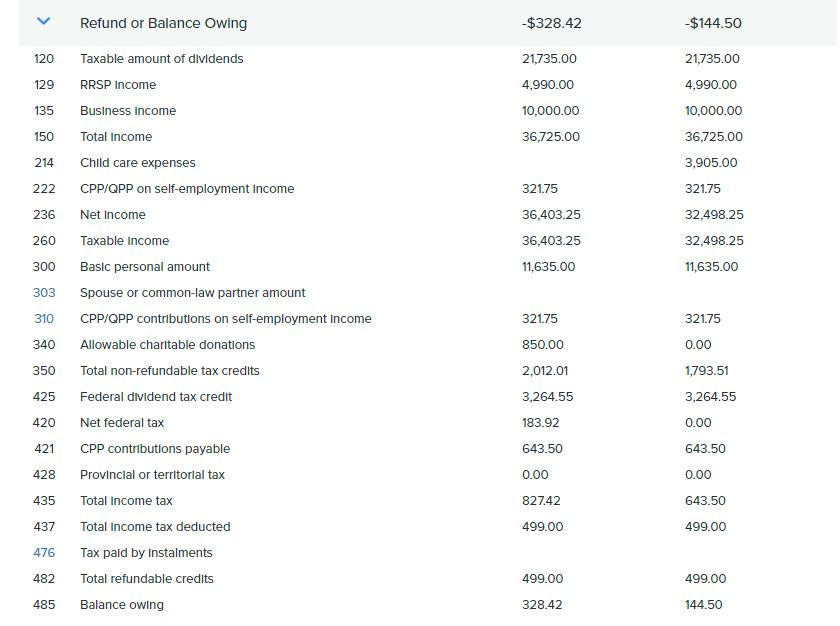

Interestingly, this would result in a different balance owing for the two of us.

Mrs. T would have to pay $328.42 in taxes. I would have to pay $144.50 in taxes. This is because I would claim the child care expenses.

Scenario 2 Total Income Summary: $74,002

- $13,520 in dividend income from TFSA’s

- $31,500 in dividend income from taxable accounts

- $20,000 in business income

- $8,982 from RRSP withdrawal

Scenario 2 Total Taxes Paid: $1,470.92

- $998 in RRSP withhold taxes

- $472.92 owed

That would be a 2.43% tax rate (exclude $13,520 from TFSA’s in this calculation). Plus we would qualify for about $669.11 of Canada child benefit each month. A really low taxrate considering our combined taxable income was $60,482.

2017 Taxes – Scenario 3

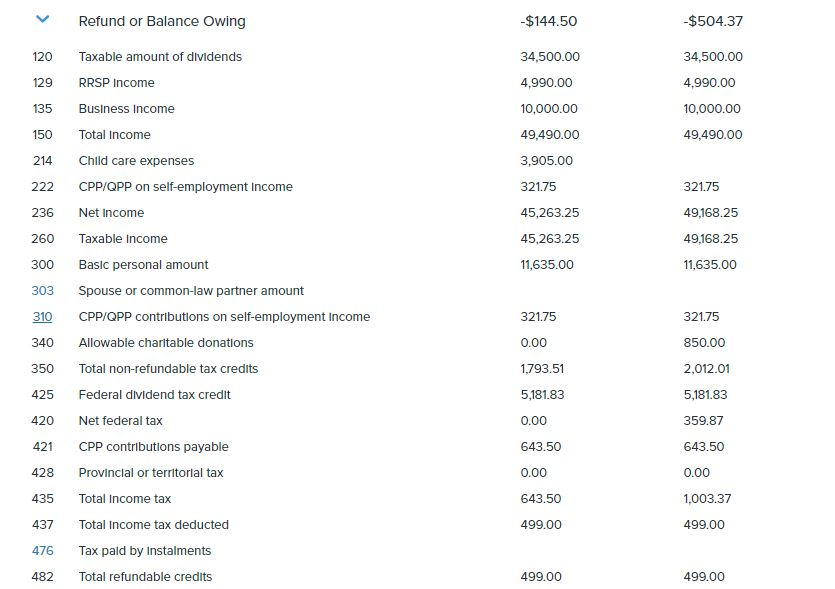

What if we were to make $25,000 in dividend income and make $10,000 in business income each while keeping the same income from TFSA’s and RRSP’s?

My Taxable Income:

- $25,000 in dividend income

- $10,000 in business income

- $4,491 from RRSP withdrawal

Taxes I Paid:

- $499 from 10% RRSP withholding tax

Mrs. T’s Taxable Income:

- $25,000 in dividend income

- $10,000 in business income

- $4,491 from RRSP withdrawal

Taxes Mrs. T Paid:

- $499 from 10% RRSP withholding tax

Our Deductions:

- $1,104.08 in Fitness for Baby 1.0

- $3,905 in Childcare (preschool) for Baby T1.0

- $1,492.20 in Fitness for Baby T2.0

- $850 donation to charities

The gross-up amount would be $34,500 and $5,182.5 for the dividend tax credit.

As you can see, I would owe $144.50 in taxes and Mrs. T would owe $504.37 in taxes.

Scenario 3 Total Income Summary: $92,502

- $13,520 in dividend income from TFSA’s

- $50,000 in dividend income from taxable accounts

- $20,000 in business income

- $8,982 from RRSP withdrawal

Scenario 3 Total Taxes Paid: $1,646.87

- $998 in RRSP withhold taxes

- $648.87 income taxes

Or a 2.14% tax rate. It’s a bit odd that we would pay a lower tax rate in scenario 3 than scenario 2.

For TFSA’s to produce $13,520 in dividend income and taxable accounts to produce $50,000 in dividend income, at 4% yield rate, we would need our TFSA portfolio to worth $338,000 and taxable portfolio to worth $1,250,000. Or $1,588,000 in total.

2017 Taxes – Scenario 4

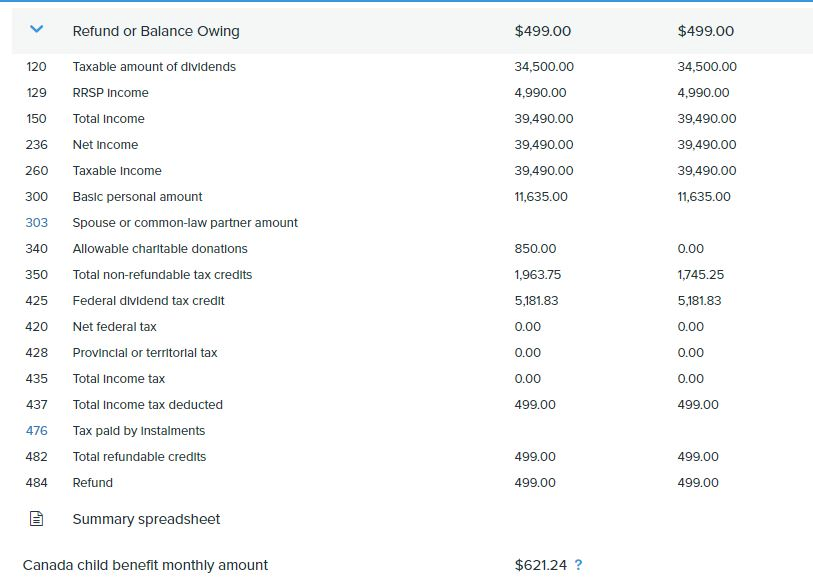

What if we had no business income at all and received $25,000 in dividend income each from our taxable accounts?

My Taxable Income:

- $25,000 in dividend income

- $4,491 from RRSP withdrawal

Taxes I Paid:

- $499 from 10% RRSP withholding tax

Mrs. T’s Taxable Income:

- $25,000 in dividend income

- $4,491 from RRSP withdrawal

Taxes Mrs. T Paid:

- $499 from 10% RRSP withholding tax

Our Deductions:

- $1,104.08 in Fitness for Baby 1.0

- $3,905 in Childcare (preschool) for Baby T1.0

- $1,492.20 in Fitness for Baby T2.0

- $850 donation to charities

And the tax filing would look like

Pretty neat to see that we would get 100% of our RRSP withholding taxes back.

Scenario 4 Total Income Summary: $73,500

- $13,520 in dividend income from TFSA’s

- $50,000 in dividend income from taxable accounts

- $8,982 from RRSP withdrawal

- $998 in tax refund

And we paid $0 in taxes once again!

Based on our 2017 expenses, a combined income of $73,500 would give us $22,355.23 buffer or 30.4%. I think that’s a lot of buffer room to cover unexpected expenses.

Final Thoughts

By using real-life expenses from 2017 and creating four different scenarios with some realistic assumptions, once again I have confirmed that it is indeed possible to live off from dividend income when we are financially independent.

Another thing that I have confirmed is that dividend income is very tax efficient, even if you make a modest amount of active income. Having kids has also allowed us to receive some deductions.

If we were to make more “active’ income when we are financially independent via businesses and side hustles, another way to reduce our taxes is to take out more dividend income from our TFSA’s and relying less on dividend income from taxable accounts. For example, maybe a 50-50 split between TFSA and taxable, or even a 60-40 split.

As you can see, when we are financially independent, there are quite a number of parameters we can play with to allow us to effectively pay $0 in taxes while sustaining our current lifestyle. While paying $0 in taxes (legally through deductions and such) is the goal, I have no problem paying taxes to make sure we can continue to receive the excellent social benefits of being a Canadian.

From a dividend income perspective, we still have some work to do. But it is very encouraging to see we are making good progress and breaking our monthly dividend income record consistently.

Great Read, you might consider leaving some RSP for later, if you have no pension , CPP and OAS don’t qualify for pension credit but RIF does , you each can draw $2000 per year starting at 65 from RIF tax free. That is $4000 per couple of tax free income. You can convert part of your RSP to RIF at 65 let’s say $10,000 and just set the payment on RIF to $2000 annually

That’s a good point, thanks.

Check out Andrew Hallems book on expatriate investing

Will take a look thank you!

Love this blog! Re: RRSP withdraws according to an RBC wealth Management document I just read: “if you make separate requests for RRSP withdrawals, the withholding tax rate applicable to each payment

only should apply.” I am looking at drawing 12 – 15 K total per year from RRSP and wind it down by 71 (current age is 56) If I make 3-4 separate requests, each should only have the withholding tax of 10% and not the 20%. Of course there may be some adjustments come tax time but I hate the thought of giving Government any money and getting a tax refund. Currently have it planned to make 60 000 net without working. Semi retiring from a 28 year public school teaching career in 3 months.

That’s true, the withholding tax is based on the amount that you withdraw so using multiple withdrawals might be a good idea to limit the withholding tax.

As an oversea non resident.. Status Canadian… We do not pay taxes…. If we invested in Canadian Vanguard or stocks then we would have to pay taxes… I wonder if it is possible for Canadians to go online and invest in American Vanguard ….. For perhaps Hong-Kong Vanguard…?. Do your readers know much about this? What are the advantages and disadvantages?

I was under the impression that as Canadians we need to declare all income made (within and outside of Canada). So when it comes to investment income, I would think you need to declare too. But I am not a tax accountant so I am not 100% sure.

SimpleTax.ca is the best tax software ever! It’s tax software for people who dont file taxes for a living. At the end of the process, felt very confident I had done a good job as opposed to feeling like an idiot bumbling my way through, hoping for the best with other programmes used the past. Funny, this article came out the day I first checked them out. Their platform is super user friendly but to see you endorse their product sold me. Hope that’s an affiliate link above, you both deserve the business!…sidenote, keep up the awesome work here on the blog, always look forward to your new posts.

Haha, it’s not an affiliate link. I just love SimpleTax and happy to send new customers to them. 🙂

I am reading a book called Invested by Danielle Town who is investor Phil Town’s daughter. She started investing in her thirties and in 2016 when the market was at its peak. The writing style is a conversation between the father and the reluctant daughter who is scared of investing.

The teacher-student narration in layman terms about Buffet and Charlie Munger style investing is intriguing. Thought to mention it for those who find the investing books dry and boring.

Sounds like a very interesting book, will have to check out Invested. Thanks for mentioning it.

Another thing to consider is that the expense will be increased after retirement due to there is no extended health care insurance any more. Now you have to pay dental care, vision care, and drugs yourself. These are core expense I think.

That’s very true, something to think about for sure.

… for long term non resident Canadians overseas there are no Canadian taxes, nor usually rssps , or Canadian pensions etc, only our overseas investments … up to almost 3 mill now via foreign stocks and real estate …

Right, I guess you have no RRSP and taxable accounts in Canada?

The idea behind RRIF is lower tax rate at age 71, as most people are in the lower tax bracket at the age.

As it stands, the dividends are almost tax-free up to a certain point if the dividends are the only source of income (this may change with the new tax budget thanks to Trudeau being out of money). I won’t give the number as I find people become greedy about the dividends. It is simply an integration rule.

The tax just kicks in due to the business income and other income.

Further, don’t forget to claim the monthly bus pass for the first six months of 2017 as Trudeau is eliminating these, too.

Further, I find people don’t know this. If people miss something, the returns can be amended online (after they are filed) and if anyone doesn’t know how to do it. Call the CRA agent and ask them to for help.

Scam Alert! If anyone receives a phone call saying that they owe money to the CRA or their property will be seized etc. etc. , ask for the agent ID number. Call the general line 1-800-959-8182 and track that agent down. The CRA never calls people at home asking for money; they always issue a notice of assessment. So, people need to be aware of scams!

Yes your tax rate should be lower once you turn 71 so you can withdraw from RRIF without paying too much taxes. And you should qualify for CPP and OAS without the crawl back penalties. However, I simply don’t like the fact that with RRIF you are required to withdraw a certain % each year and that % increases as you age. I don’t like to be told to do something. 🙂

Good call on the scam alert. People need to be aware of such scams.

Thanks Tawcan for the very interesting calculation. You are assuming an early retirement, I think the age of retirement makes big difference with withdraw strategy.

We will retire not so young so it’s important for us to keep in mind that RRSP has to be converted into RRIF and we will be forced to withdraw a certain percentage of our portfolio. So I think when calculating how much to withdraw from RRSP, not only tax on current year needs to be considered, how much will be left in your RRSP at 71 is another big factor. Withdraw only $5000 basically won’t be an option for us.

Hi May,

Yes, that’s very true that you need to consider how much will be left in your RRSP at 71. This calculation is based on if we are living off dividend income in 2017, and since we were in our early-mid 30’s last year, I didn’t want to take out too much from our RRSPs.

I do wonder if it makes sense to eventually convert RRSP into RRIF or if it makes more sense to collapse before age 71 and just live off TFSA & taxable accounts. I just don’t like that RRIF has a mandatory minimum withdrawal rate.

I definitely would like to collapse RRSP before age 71. The feasibility however will depend on the age of retirement and the size of RRSP. Also, how much income generated already from taxable accounts. We definitely don’t want to pay too much tax during retirement years. My current plan is deferring CPP and OAS to 70, and live off RRSP and taxable accounts before that while keep transferring funds to TFSA.

I think that’s a good strategy, esp when you can transfer investments in-kind to TFSA and taxable.

Maybe you can have a new blog to discuss RRSP collapse strategy? It would be definitely nice if there is no RRSP but only taxable account and TFSA at age of 71. Regardless what the tax rate is, you have more control over your finance. So how to get there if you have RRSP of size, let’s say, $1M for two, and you retire at 60?

I have read an article regarding to borrowing to invest as strategy for collapsing RRSP. But borrowing to invest is very high risk and it’s conflicting with people want to reduce risk in retirement, not increase it.

Where does this fit into all of this? https://www.google.ca/amp/s/www.theglobeandmail.com/amp/globe-investor/investment-ideas/strategy-lab/dividend-investing/you-do-the-math-almost-50000-in-earned-dividends-0-in-tax/article4599950/

Similar idea I guess. Getting $50k in dividend income (from taxable) would mean a portfolio worth $1.25M at 4% yield. That’s a sizable portfolio. 🙂

Hmmm…. this has made me realize that I need to stop relying so much on RRSP because the money is really inaccessible in early retirement. Do you prefer investing in TSFAs over taxable accounts?

We always max TFSA and RRSP first before investing in taxable accounts. I really like TFSA, wish the Canadian government would increase the yearly contribution limit. 🙂

Not sure what you mean by inaccessible. You can withdraw whatever amount you want at any time. Sure you’ll pay withholding tax, but any excess tax paid will eventually get refunded. It seems like a good tool for early retirement–you reduce your taxes during your working years and you can withdraw during early retirement when you’ll have little or no employment income, paying almost no tax.

Right, inaccessible isn’t the right word, you’ll just get hit by withholding tax, depending on the amount you take out.

I just did a quick calculation with SimpleTax. If we were each to take out $17,000 from our RRSP’s (pay $5,100 in withholding tax) and still get $15,750 dividend income from taxable accounts, we would get $8,818 back all together.

This means we’d pay $1,382 of taxes on a total of $55,390. About 2.5% taxes altogether, still really really low.

Hi Bob!

Great post; love the simplicity behind it.

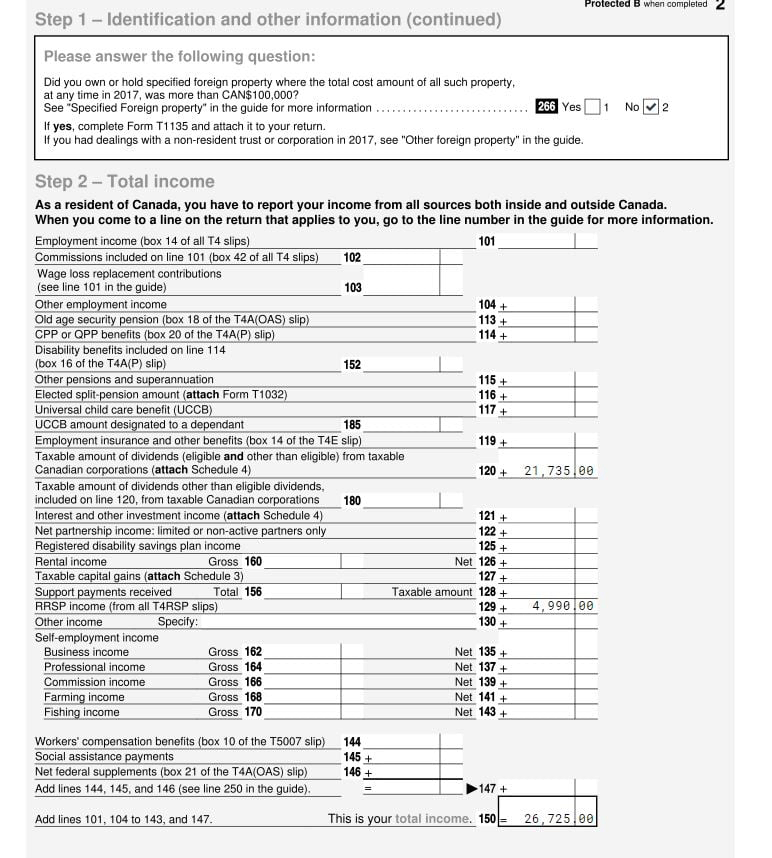

Quick question: under Scenario 1, your taxable income (line 260) says $48,460.

But under Schedule 1, Step 2, it says $26,725. Can you explain what happened to the difference, or roughly $21,735?

Ahh good catch! I posted the wrong T1 images. I have corrected the images. Thanks for catching this.

This is a really interesting read because Canada’s taxes are so different than the United States. I was under the assumption that yours were higher so there was no way you could effectively pay no tax, but apparently I was wrong.

I like how you split out “necessities” from the rest of your spending to get to your base income need. I think I’m going to do that in the future, because quite a bit of our spending these days is still discretionary.

I think taxes in Canada and US are pretty. There are a few key differences though, like couples have to file separately here in Canada and mortgage interest isn’ tax deductible.

Total media spin and political mis-information out there making people think we are so heavily taxed. It should also be noted that your health care would be free and on top of that you would be get that $9900 in cash deposited into your account for the kids from the government.

A little late, but….the type of income makes a huge difference. True, dividend income has extremely low tax rates. However, $50,000 of regular income from a job would be taxed at a MUCH higher rate, it varies by province and territory, but in the neighbourhood of 30%. Plus, we pay anywhere between 5% and 13% on almost all goods and services, with only a few exceptions like basic groceries (again, the rate depends on which province or territory). I’m not an expert on U.S. taxes but I believe we do pay a lot more tax, but we receive more for that tax money (healthcare, social programs, etc.).

Just to clarify before I called out, since taxes are scaled, your first $10k or so would be 0% tax, then it increases in increments up to 30% by the time you’re getting close to $50k. So you would not be paying 30% on the entire $50k.