I’ll be turning 40 later this year. Since I am very much enjoying my full time job in high tech and finding it mentally challenging, I have no intention of quitting and “retiring” any time soon. However, the question of whether we have enough to retire when I’m 40 has popped up a few times in the last couple of years.

As some readers may recall, my dad and my cousin both said sayonara to the corporate world when they were 42 and 43 respectively. The competitive side of me has always wanted to beat them by a few years. It is my hope that by retiring in my early 40s it would provide some inspiration for my own kids in the not-so-distant future.

Can we “retire” in 2023 while I’m 40 years old? Let’s take a look at the numbers and find out.

Do we have enough to “retire” in 2023?

Before I dive into the numbers, I’m sure many of you have noticed the quotation around the word retire. Why am I doing that?

Since starting our FIRE journey, I have always focused on financial independence. I don’t believe in early retirement. To me, retirement means sitting on the beach sipping pina colada all day.

That may be fun for a week or so. But long term for someone that’s only in their 40s?

BORING!!!

That’s why I have stated that it’s time to retire FIRE. Becoming financially independent simply would allow someone to do things they enjoy, regardless of whether they got paid or not. The financial freedom behind financial independence is extremely powerful and empowering when you think about it.

So when I talk about retiring in 2023, I mean quitting my full-time job to enjoy life. This could mean spending more time travelling around the world (when COVID restrictions are finally lifted), volunteering at local charities, spending more time reading, or challenging myself to run a marathon. It could also mean shooting more weddings and portraits with my photography business (I’ve not paid as much attention in the last 3 years or more) or increasing my blog publication frequency from once a week to twice a week as a way to help more people.

Some people may call working on my side businesses entrepreneurship because I’d be quitting my job to focus on self-employment. I don’t see it that way though. For me, it’s about working on things that I enjoy and not having to worry about how much money I make. I have found in the past when I have this mindset, money seems to come freely.

Live off dividends only – what about taxes?

One of our goals is to live off dividends when we are financially independent. Can we simply live off dividends without the need for additional supplementary income?

For 2022, our goal is to receive a total of $36,000 in dividend income. We have worked quite hard on increasing our dividend income by having a high savings rate and investing in stocks regularly.

Based on the latest dividend income projection, assuming no new contributions, no dividend cuts, and no dividend growth for the rest of the year, we should receive a little over $40,000 in dividends*. So I will use this number as the baseline dividend income if we were to retire in 2023.

In case you’re curious, the dividend breakdown across the different accounts is as below:

| Accounts | Dividend Amount |

| Mrs. T Taxable | $5,950.82 |

| Tawcan Taxable | $10,473.20 |

| Mrs. T TFSA | $5,153.92 |

| Tawcan TFSA | $5,899.08 |

| Mrs. T RRSP | $4,329.50 |

| Tawcan RRSP | $8,208.91 |

| Total | $40,015.43* |

* The projected income is actually higher than this amount since we’ve purchased more dividend paying stocks and there has been organic dividend growth.

I’m very ecstatic with this dividend income projection. But since not everything is tax-free, what would be our net income after paying income taxes?

For this calculation, I used Wealthsimple’s Tax Calculator for 2021. It’s simple and easy to use. But it does not take common tax deductions like donations, spouse/common-law partner amount, and health expenses into consideration. For all intents and purposes, this calculator is sufficient for this exercise.

For the living off dividends scenario, let’s assume that we will take out all the dividends from our RRSP and will pay withholding taxes as a result. Since I no longer have a full time job, let’s assume I have no other working income. We will also assume that we won’t make any RRSP contributions.

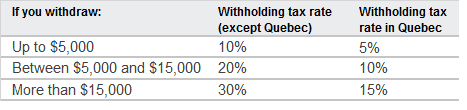

Per my millennial’s ultimate RRSP guide, one must pay withholding tax for any RRSP withdrawals that are not part of the home buyer’s plan or life learning plan. The amount of withholding tax depends on how much money you take out.

So if we take out $4,329.50 from Mrs. T’s RRSP and $8,208.91 from my RRSP, we’d have to pay $432.95 and $1,641.78 in RRSP withholding tax. The remainder, $3,896.55 and $6,567.13, respectively, would be counted as working income and be taxed at our marginal tax rate.

Please note that we do receive US dividends in our RRSP accounts. To keep the math simple, I’m ignoring the currency exchange rates.

Dividends from our taxable accounts would be taxed as well. But since we only hold Canadian dividend stocks that pay eligible dividends in our taxable accounts and these eligible dividends are very tax efficient, we should be able to minimize the amount of taxes paid.

Putting all the numbers into the Wealthsimple Tax Calculator we end up with these numbers:

| Mrs. T | Tawcan | |

| Employment Income | $4,329.50 | $8,208.91 |

| Self-employment income | $0 | $0 |

| Eligible dividends | $5,950.82 | $10,473.20 |

| Income Taxes Paid | $432.95 | $1,641.78 |

| Estimated refund/tax owed | ($432.95) | ($1,641.78) |

| Average tax rate | 1.13% | 2.13% |

| Marginal tax rate | 20.06% | 20.06% |

| After tax income | $10,280 | $18,682 |

| TFSA | $5,153.92 | $5,899.08 |

| Total Net Income | $40,015.43 |

Essentially if we rely on dividend income only and have no other income, we don’t have to pay any income tax. How nice is that?

How much do we need?

But is $40,000 in dividend income enough money for us?

Based on our spending history over the last 9 years, we have been spending under $40,000 in core spending with total annual spending between $45,000 to $60,000 (last year was higher than usual due to a few unexpected expenses). These numbers exclude any side business related expenses and contributions to TFSA, RRSP, and RESP.

| Total core spending | Total Annual Spending | |

| 2012 | $26,210.52 | $44,603.76 |

| 2013 | $26,343.00 | $45,260.88 |

| 2014 | $29,058.96 | $47,391.96 |

| 2015 | $31,256.88 | $47,270.16 |

| 2016 | $29,831.40 | $47,566.96 |

| 2017 | $33,887.68 | $51,144.77 |

| 2018 | $31,840.75 | $57,231.99 |

| 2019 | $33,199.98 | $54,906.02 |

| 2020 | $35,511.60 | $48,908.74 |

| 2021 | $38,950.66 | $71,852.02 |

Core spending does not include expenses like travel, donations, gifts, eating out, summer camps, etc. So, to cover these non-core expenses, I believe we need a total $60,000 net income to sustain our current lifestyle while giving us some spending buffer.

When I’m “retired”, we don’t have plans to continue contributing to our RRSPs. We do plan to continue to contribute to our TFSA and RESP’s. To be as tax-efficient as possible, we probably will look into transferring shares from taxable accounts to our TFSAs rather than contributing new cash (we’d contribute if there is free cash available). We’d contribute $5,000 total in the RESP’s for both kids. This would result in a need for $65,00 in net income each year.

We usually incur around $5,000 in business expenses between Mrs. T and me. This would mean we need a total net income of $70,000.

As mentioned, there are some buffers in this $70,000 per year income needed to give us some flexibility. Most likely, we can reduce this amount by slightly optimizing our annual expenses.

In other words, while our $40,000 in dividend income can cover our core expenses, it doesn’t provide us with much buffer at all. We need to find additional income to supplement our dividend income.

Self-employment income

Mrs. T enjoys her doula work and I enjoy shooting pictures and writing on this blog. What if we supplement our dividend income with self-employment income? Do we have enough for me to retire in 2023?

For this scenario, let’s assume that Mrs. T makes $10,000 in self-employment income and I make $25,000 in self-employment income. I’m using relatively small numbers so we aren’t forced to have to side hustle all the time and not enjoy life.

The dividend income and business income add up to about $75,000 per year in this case. How much taxes do we need to pay?

| Mrs. T | Tawcan | |

| Employment Income | $4,329.5 | $8,208.91 |

| Self-employment income | $10,000 | $25,000 |

| Eligible dividends | $5,950.82 | $10,473.20 |

| Income Taxes Paid | $432.95 | $1,641.78 |

| Estimated refund/tax owed | $823.05 | $3,765.22 |

| Average tax rate | 6.19% | 12.38% |

| Marginal tax rate | 20.06% | 22.70% |

| After tax income | $19,025 | $38,275 |

| TFSA | $5,153.92 | $5,899.08 |

| Total Net Income | $68,353 |

Between the two of us, we’d be paying a total of $6,663 in taxes which includes CPP/EI premiums, bringing out total net income to $68,353. This means we’re roughly short by about $2,000 to our target of $70,000 net income.

The conservative or pessimistic side of me would conclude that’s not enough and I need to continue to work and build up our dividend income and side business income.

The more optimistic side of me would conclude that these numbers are close enough and given that we already have built-in some buffers with the $70k target, it should be OK for me to give my 2-week notice and retire sometime in 2023! Woohoo!

Wrapping it up – additional thoughts & analyses

Based on these rough calculations and analysis, if I really wanted to, I probably can retire in 2023 while I’m in my 40’s and have more free time. While relying on self-employment income isn’t the ideal situation, here are some additional thoughts and analyses.

- As mentioned, for our dividend income, I didn’t convert USD to CAD, so the actual dividend income will be higher than $40,000 (because of the conversion of American dividends at about 1.27).

- For self-employment, since we can deduct business expenses and business home usage expenses, the actual net income most likely will be lower than $10k and $25k respectively. This should bring us much closer to the $70k target. Hypothetically, if we each have $2,500 in total business expenses, the numbers would look like below:

| Mrs. T | Tawcan | |

| Employment Income | $4,329.50 | $8,208.91 |

| Self-employment income | $7,500 | $22,500 |

| Eligible dividends | $5,950.82 | $10,473.20 |

| Income Taxes Paid | $432.95 | $1,641.78 |

| Estimated refund/tax owed | $538.05 | $3,1627.22 |

| Average tax rate | 5.46% | 11.58% |

| Marginal tax rate | 20.06% | 22.70% |

| After tax income | $16,809 | $36,413 |

| Deducted business expenses income | $2,500 | $2,500 |

| TFSA income | $5,153.92 | $5,899.08 |

| Total Net Income | $69,275 |

This results in a net income of $69,275. Hey, that’s pretty darn close to our $70,000 target! Now I know you probably will say that business expenses shouldn’t be added back as income… I suppose you’re right.

- I have ignored the idea of selling some stocks to supplement our dividend income. Since stock profits are taxed at 50% of our marginal rate, selling stocks and using the money to supplement our dividend income may be more tax efficient than supplementing with self-employment income. Per the Cashflows and Portfolio retirement projections, the most optimized withdrawal order is taxable first, RRSP second, then finally TFSA. Therefore, I suspect further tax optimization can be had if we were to sell a small amount of stocks in our taxable accounts and not withdraw any money from our RRSPs. I would need to consult with a tax specialist to understand the details.

While it is not possible for me to retire in 2023 and rely on dividend income alone, it is definitely possible if we were to supplement our dividend income with business income or sell a small portion of our dividend portfolio. It is comforting to know this possibility is available to us.

For now, I have no plan to hand in my 2-week notice. But it is comforting to know the option is there if we ever choose to. This awareness has also provided some self-empowerment for me when it comes to how I view my full-time work.

We plan to continue our financial independence plan and re-evaluate our plans sometime in 2025. Since situations and plans can change, we also keep reminding ourselves to remain flexible and adaptable.

Note: I’m not a tax expert so this is merely a fun analysis. There may or may not be some mistakes in my calculations.

Congrats! I look forward to you taking the leap of faith. Enjoying your same career at age 40 is pretty incredible. I burned out after 11 years of doing the same thing.

Just make sure you’re not suffering from the “one more year syndrome.” It can sneak up on you year after year.

As one commenter above pointed out, a year now is worth way more than a year in the future. Personally, with two young children, there is no way I would spend more than three hours a day working for money. The kids are growing up too fast.

I’d rather spend time making money after they leave the house.

Sam

Thanks Sam. Appreciate you sharing your insights.

Well done Bob! So inspiring to see how you’ve amassed a sizable portfolio that brings in an impressive 40K in dividend income. P.S. It was also so nice to watch you on the Canadian Financial Summit. Way to go man!

Thanks Moe.

Hi

I’m a 45 yo accountant who semi retired 3 years ago. I still work about 25 hours a week during the 2 months of the tax season (I own the practice but it is entirely run by someone else).

I accumulated my “pension fund” in a holding company and invested in canadian dividend paying stocks . Currently at around 45 k/ year in dividends. Plus 7K of dividends in TFSA/RRSP from ETFs in US and world markets, not dividend driven. Pretty much 100% equity portfolio allocation.

At the level of income you need (and myself, which is 70K combined with my girlfriend and our 12 yo kid) canadian dividends make sense for tax purposes. They are even more efficient than capital gains (I can get around 45K in eligible dividends before paying tax, but a 45K capital gain (22.5K taxable) will trigger tax).

If you like your job, and I assume it is well paid, then yes stay there. But once you taste the freedom of doing what you want every day, you don,t want to go back. And stopping work opens a whole lot of opportunities (both paid and volunteer) that you would never consider while working. I coach my son’s basketball team and also became a basketball referee.

Don’t delay too much that free time. In finance, a dollar today is worth more than a year from now. But it also applies to time. A free year today (while healthy and young) is worth more than a free year in 10 years, because nothing is guaranteed. Check this article out, I really like it :

https://www.dividendmantra.com/a-year-isnt-a-year/

Thanks William for offering your thoughts on this topic. Having time freedom is pretty powerful. 🙂

Congrats on your progress. Careful with self-employment and CPP contributions : on self-employed earnings you pay both the employer and employee portion (totals 11.4%) on earnings higher than $3500. I expect your CPP contribution on $22500 should be a lot more than your stated amount of $271.

That’s a good point about CPP contribution, may be worthwhile to consider incorporating the self-employement business if it makes sense. 🙂

Incoporating does not make sense with those levels of income. The expenses related to incorporating and annual fees would erase any benefits. Plus, CPP contributions as you know are not tax, they mean you’ll get a higher monthly sum when you withdraw.

Yup I agree that incorporating doesn’t make sense at these income levels, already ran the numbers.

Hi Bob. I enjoy your blogs. Keep up the great work.

I retired at 52 due to health issues. I deferred my pension start to 58 to reduce the haircut and lived on savings for those 6 years. One year I did transfer some stocks in kind to cover my TFSA contribution. Of course it triggers capital gains and when I did the payback calculation, it was something like 18 years to recover the capital gains tax (not counting dividend increases). In your case, you mentioned you might do that, but you are reluctant to sell stocks to supplement your dividend income. I feel transferring stock in kind to your TFSA is similar to selling and depositing cash.

Best wishes

Stephen

Hi Stephen,

Don’t have a pension so we need to self-fund our retirement. Trasnferring stocks in kind to our TFSA is definitely a potential option to offset amount of taxable income. Will have to calculate the tax implication when the time comes.

Great analysis Bob!

If it’s not prying into your personal finance too much, I would be interested to know how your mortgage fits into your over-all financial planning. Assuming you still have one, how much do you try to pay it down. Or do you look at your mortgage as a necessary expense that you pay the minimum on, while funneling most of your money to your portfolio? So far, I have followed the latter plan. If I am only paying below 3% interest on the mortgage (only until 2025 unfortunately!) but I can make over 5% in my portfolio, I have found it difficult to justify allocating funds towards paying off what I consider to be the “eggs in one basket” nature of a house. I would appreciate your insights here.

By the way, that was a great interview on the Canadian Financial Summit!

Thanks Kyle. Looking at the mortgage as a necessary expense.

Glad to hear you won’t be quitting your full-time job.

Since you enjoy your work + have 2 very young children + obviously are the family’s main breadwinner, I’d be cautious in my approach to ‘retirement’. Especially at this point in time, with a recession looming (dividend cuts???) that could last years.

Right, continuing working will provide a bit more flexibility and options. The looming recession is definitely a concern.

How does the increase an CCB with a lower reported income play into your calcs?

Good question Court. We didn’t consider CCB in any of the calculations. Sine CCB is tax free, it’d be considered as extra gravy. 🙂

Congratulations! If you still enjoy your job, then keep at it. It’s great to know you have options, though. Things always change.

IMO, most people underestimate how much money they will make after leaving their career. You’re still young and have a lot of energy. You probably would hustle more and make more income from your side gigs when you don’t have to work full-time.

Great job building your dividend income up over the years.

Yup, continuing working will give us a lot of options. 🙂

Incredible! I always look forward to reading your articles. You and your family must be so proud of your growth- amazing! I am 31 and invest every month in ETFs to build my portfolio. I hold a few blue chip stocks but don’t feel confident enough (even though I do lots of research and reading) to go “all-in” on stocks. Do you have any advise for someone in their early 30s?! Thanks!

Thank you Carly, appreciate your suport.

For younger investors I believe you’re better off focusing investing in one of the all-equity ETFs like XEQT or VEQT. https://tawcan.com/all-equity-etfs-veqt-xeqt-hgro/

Once you have a sizable all-in-one ETF you can consider investing in individual dividend stocks if you wish.