If you look at our dividend portfolio, you’ll see that we own over 50 individual dividend stocks and one index ETF. I will be the first one to admit that we probably own a few too many individual dividend stocks. Therefore, I plan to reduce that number to something around 40 to 45 over the next few years.

Since we add new cash each year to purchase more dividend paying stocks and index ETFs, my current plan is to add more shares to our existing holdings, rather than initiate new positions (unless there are extremely attractive names with good stock prices I can’t ignore).

With that in mind, here are 6 stocks I plan to buy more of in 2022 and my reasons.

6 stocks I plan to buy more of in 2022

Please note, I’m not a financial professional so whatever I write on this blog is purely my opinions and not advice/recommendation. Please always do your own research and buying and selling decisions. Thank you.

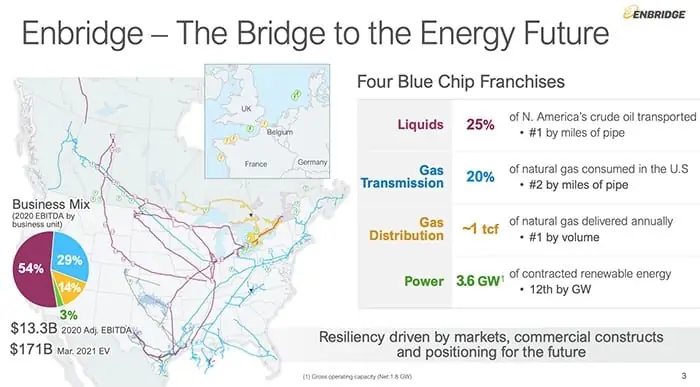

1. Enbridge (ENB.TO)

I have been building our Enbridge position over the last number of years. A few years ago, we purchased a lot of Enbridge shares when the stock price was below $40 thinking the stock price would move up over time.

So far these purchases have paid off for us, resulting in a nice paper gain.

Why am I considering buying more Enbridge shares now that the stock price is over $50 and seemingly expensive to some investors?

First, due to environmental concerns, it is getting harder and harder to build new pipelines. For example, the Keystone XL pipeline project was cancelled as a result of environmental concerns. Since it is nearly impossible to build new pipelines, existing pipeline infrastructure has become more valuable than ever. It shouldn’t surprise anyone that Enbridge’s existing 5,000 km pipeline system is now worth more than it was five years ago.

Second, we North Americans rely heavily on natural gas and oil in our everyday lives. Cleaner, non-fossil fuels are slowly shifting our reliance on natural gas and oil but I don’t see us going away completely from natural gas and oil in the next 10 to 15 years.

Some of the inability to shift away completely from fossil fuels is because of technical reasons. Here in Canada, more houses are using heat pumps as the prime heating source. Since heat pumps are most efficient at above 4 degrees Celsius, many of these houses use natural gas furnaces for backup. Furthermore, in most parts of Canada when the average temperature in the fall and winter is consistently below 4 degrees Celsius, heat pumps aren’t the best tool for heating, so Canadians will continue to rely on natural gas-powered furnaces.

Finally, Enbridge pays a healthy 6% yield. Based on my research using free cash flow, Enbridge should be able to continue to pay its juicy dividends. Even if Enbridge only raises dividend payout between 1% to 5% each year, the dividend income should continue to outpace lower yield high growth dividend stocks for many years.

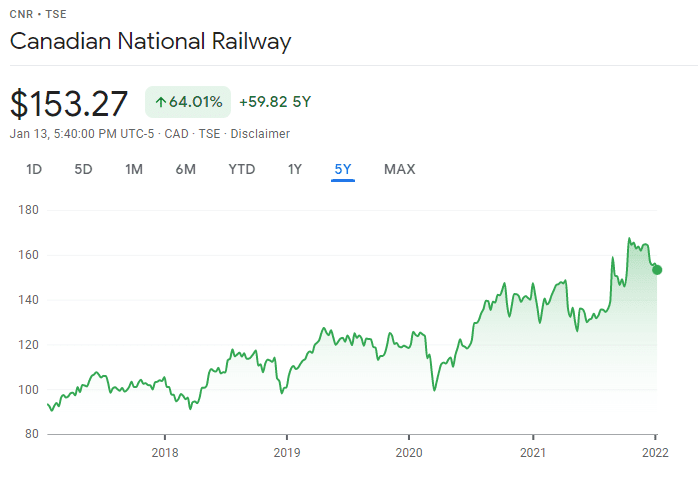

2. Canadian National Railway (CNR.TO)

Like Enbridge, we have been slowly building up our position in Canadian National Railway over the years. What was one of the key topics that people keep talking about during this global pandemic?

Supply chain issues.

Remember people hoarding toilet paper at the beginning of the pandemic then recently hoarding eggs, beef, and poultry during the BC floods?

People tend to get a bit crazy when there’s a supply chain issue on products they rely on a daily basis…

Although airplanes are readily available to move people, many goods are still being transported via rail in North America. Why? Because rail remains to be one of the best, most cost-efficient ways to move goods around North America. This trend is not going away soon and Canadian National Railway will benefit from it.

Despite CNR’s low yield of around 1.5%, it has a ten-year dividend growth rate of 14.2% and a five-year dividend growth rate of 10.4%. Most importantly, the stock price has appreciated over 60% in the last five years.

A boring yet highly profitable company that pays stable and growing dividends? Sign me up!

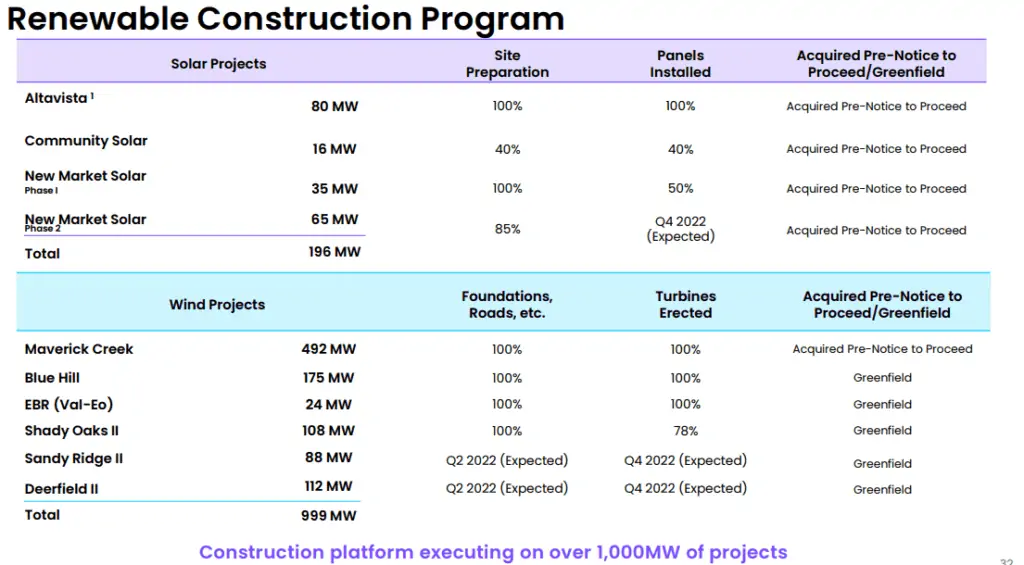

3. Algonquin Power & Utilities (AQN)

Although I just wrote about our dependence on fossil fuels when it comes to Enbridge, Mrs. T and I continue to like renewable energy as we think renewable energy is the future. For the sake of our kids, their kids, and all future generations, we need to change our energy strategy and shift our reliance on fossil fuels to renewable energy. I truly believe this is absolutely vital for the continuation of humankind and Earth.

As of December 2021, Algonquin owns and operates ~4.1 GW renewable assets and has many different renewable projects in the pipeline to increase its renewable capacities. For example, the Altavista and other solar projects will add 196 MW and the Maverick Creek, Blue Hill, Deerfield II and other wind generation projects will add another 999 MW to Algonquin’s portfolio.

There are a lot of potential future growths with Algonquin. Given the stock price has taken a beating in the last year, we plan to take advantage of the discounted price and build up a holding with sizable AQN shares.

Given the juicy +4.5% yield, we can collect dividends from Algonquin and wait for the stock price to appreciate. This certainly beats holding a stock that doesn’t pay any dividends.

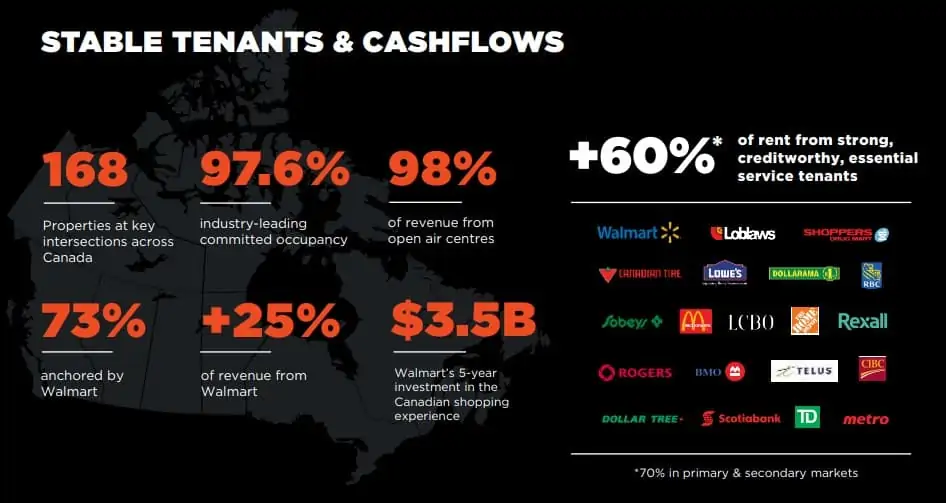

4. SmartCentres REIT (SRU.UN)

For many years, people believed online retailers would take over and brick-and-mortar stores would cease to exist. Sure, consumers have been ordering products through online retailers like Amazon regularly. However, brick-and-mortar retailers like Walmart, Target, Costco, and Home Depot have learned to adapt and change their business model and strategy in the fast changing market.

Throughout this global pandemic, people have again doubted these brick-and-mortar stores. Lockdowns and restrictions have prevented people from accessing shopping malls and brick-and-mortar retailers.

For real estate investment trusts like SmartCentres REIT, rent collection level became a big topic. Most investors were concerned whether these retail REITs can continue collecting rents from their tenants. These concerns sent the retail REIT sector into a downward spiral. Some retail REITs had to cut dividends. Fortunately, SmartCentres REIT continued paying dividends despite all the turmoil and uncertainties.

Mrs. T and I don’t frequent shopping malls but whenever we visited shopping malls throughout the pandemic, we found lots of people in them. This gave me a key realization – for many people, shopping malls are the place for their social interaction. They meet up with friends for coffee or food in shopping malls. Some people like to be surrounded by people so they head to shopping malls regularly to meet that need.

There are a few things I particularly like about SmartCentres REIT. One, SRU.UN has 168 properties across Canada and 73% of these properties are anchored by Walmart. Walmart typically does not close stores once they are opened; Walmart also spends a lot of money each year to improve the look and feel of their retail stores. In other words, Walmart is a great tenant to have.

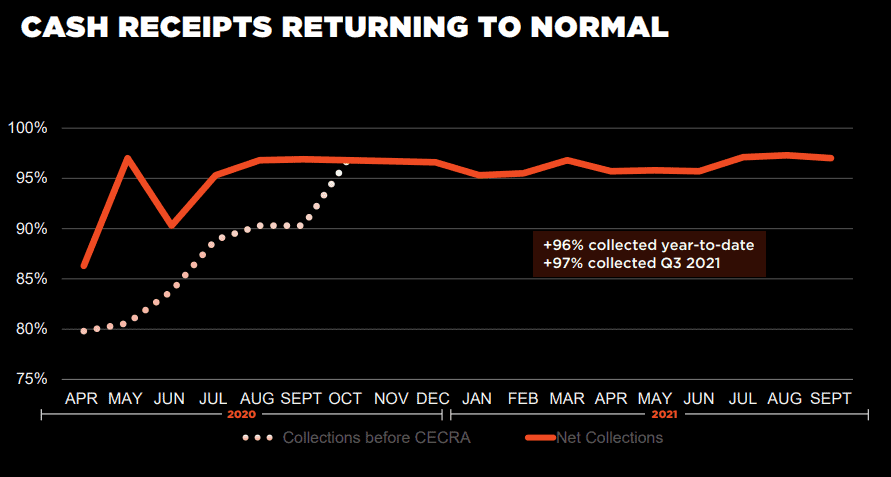

Another thing to like about SmartCentres REIT is that the cash receipts have returned to the historically normal level. Early on in the pandemic, the cash collection dipped to as low as 86% but it has since returned to around its normal range of around 97%.

SRU.UN also has 54 projects completed, 84 active projects, and 153 future projects which should unlock $3.7 billion of potential value to shareholders.

We plan to continue to add SRU.UN in our TFSAs for tax efficiency reasons.

5. Apple (AAPL)

Recently, Apple became the first US company to cross the 3 trillion dollar market cap and I believe the company will continue to grow.

Apple has become a profit-generating empire by creating a tightly integrated ecosystem. Once you buy into the Apple ecosystem, it becomes increasingly more and more difficult to leave this ecosystem the more Apple products you own.

It is expected that Apple will announce new products this year – a high-end 27 inch iMac, a new Mac Pro desktop, a revamped MacBook Air, an updated Mac mini, new Apple Watches, new iPhones, new AirPods Pro, and possibly other new products like a new external display and an augmented reality headset. All these new products will trigger existing customers to either upgrade their Apple products or entice new customers to switch from Apple’s competitors, generating more venues for Apple.

Apple has never been the “first” to create a new product but it has a long history of innovating and improving existing products and making them better. Just take a look at iPhone and iPad. It’s hard to believe that it has been 15 years since Steve Jobs announced the iPhone. Who knows, maybe Apple will enter the electric car space in a few years, announce its “next” revolutionary product series and start the next chapter of the company.

I’m convinced that Apple will continue to thrive and so I plan to add more Apple shares in 2022.

Ok, XAW technically isn’t stock but I’ve decided to include it on this list.

Since XAW holds more than 9,000 international stocks with more than 60% exposure in the US, 6% exposure in Japan, 4% exposure in the UK, and 3% exposure in China, it is an excellent ETF to hold for international exposure and sector diversification.

We plan to add more XAW in 2022 in our RRSPs and non-registered accounts and take advantage of the commission-free ETF purchase that Questrade offers.

Summary – 6 stocks I plan to buy more of in 2022

There you have it, six stocks (five stocks, one ETF) that I plan to buy more of in 2022. We plan to buy these stocks across all three of our accounts – TFSA, RRSP, and non-registered.

However, with tax efficiency in mind, we will only purchase REITs in either our TFSAs or RRSPs; we will only purchase US stocks like Apple in our RRSPs to avoid the 15% withholding tax on dividends.

What will happen in 2022? Will 2022 give us yet another great year of return? Will the market finally crash from its all-time highs this year?

Well, I have no idea. Your guess is as good as mine. But I know one thing for sure – time in the market is far more important than timing the market.

So keep increasing your savings gap and invest the difference.

Happy investing!

Would like to know more on which etf’s are best in a rrsp. Thank you.

Really not much difference if you’re holding them in an RRSP.

April 29, 2022

I’m new to this. I’m retiring. I’d like to buy more dividend stocks, but don’t want to overpay. Do any of these make sense right now as entry points?

Thanks for all the info

I have been buying them so far this year but please do educate yourself and always make your own buying and selling decisions on your own. 🙂

From a New Zealand view of Canada..why not any of the Canadian Banking Stocks..??

We added a lot of Canadian Banks throughout 2020 so there’s currently no plan to add more.

See here – https://tawcan.com/dividend-stock-transactions-2020/

Nice list, Tawcan! I own most of these. I hold $ENB, $AAPL, $AQN, and $SRU.UN. I am just letting $ENB and $AQN DRIP at this point. I’d add to Apple and $SRU.UN on pullbacks. I would like to own $CNR at some point as well. Thanks for sharing.

Thanks Graham. Good to hear that you also hold the same stocks as us.

Hi Bob,

Compelling article backed up with well-articulated argumentation (as usual)!

CNR is definitely on my list for a growth investment vehicle (and I have worked for them for 16 years).

I agree fully with SRU.UN and AQN but more as perfect dividend generators with limited growth potential short-term. The way I see it, those stable dividend generators create the means (through their dividend generation) to invest into the other growth stocks in my portfolio in order to get the best of both worlds.

My personal top 2 would be MFC and NWC Both companies seem to have solid leadership and a clear business vision to continue to position well into the future with proven year-to-year growth and high dividends. Also an undervalued asset of both of those companies is that they are rather discreet on the market place and in their public relations so less likely to swing wildly on a whim.

Thanks Olivier. We already own quite a bit of MFC so there’s no plan to buy more. It was one of the first stocks that I purchased before the financial crisis. Haven’t looked at NWC too closely but I like the niche market.

I’m a fan of SRU.UN and bought it during the initial phase of the pandemic around $25. I’ve enjoyed receiving the generous dividend for almost a year, as well as some healthy capital appreciation. Now though, I’m looking backwards and seeing extremely limited dividend increases, and a few dividend reductions. Today their dividend is at $0.1542, while in 2016 in started the year off at $0.1375. That’s only a 12% appreciation over 6 years (compare with our bank’s recent increases). In January of 2016 the SP of SRU was $30.16. That’s only a price appreciation of 2.3% over the six years.

Using Portfolio Visualizer I compared AQN (since I commented on that one elsewhere) vs SRU.UN from 2016. AQN significantly outperformed.

I will say that I think SRU.UN is in a transformative point as they add to their portfolio with a new focus on mixed use development. I think it is very exciting and potentially quite lucrative, but my fear is that the market will be slow to acknowledge these changes. I also think they will be slow to raise the dividend as the transformations they are making are capital intensive. I have chosen to exit my SRU position in favour of other dividend payers on the BTSX list that I do not currently own, but it has certainly been a good ride and I might regret my decision down the road!

Fair point James, dividend growth isn’t typically very high for these REITs.

FWIW, I think this is a strong candidate to return to for my decumulation phase in order to supercharge my dividends in the “go-go” phase of retirement.

Hi Bob. Great Blog / Website and I have used many of your ideas and suggestions. I’m approaching retirement so I am focused on high yield stocks with some growth stocks added. I have 4 out of your 6 on the list, partly due to my resistance / reluctance to buy US stocks directly. Don’t want the hassle with the exchange, fees, etc.

I have noticed that you don’t buy or talk about Canadian Tech stocks (ie. OTEX), rather you focus on the US tech stocks for your purchases in your portfolio.

Is there any reason for this? Is it a matter of preference and more “bang for your buck” with US tech stocks, the US being more tech savvy, or perhaps there is nothing of value or significance in the Canadian market?

I would like to hear your thoughts….or perhaps this (Canadian Tech stocks) could be addressed in a future blog.

Regards,

John

Hi John,

A very good question. I guess I prefer US tech stocks because there are more choices in the US and these US tech companies are more profitable and have wide moats. Personally I’d rather invest in the likes of Apples than Open Text but that’s just my own opinion.

Thanks Bob. I’m a newbie to Dividend Investing and I thought I was missing something re: Canadian Tech stocks. The DGI blogger community doesn’t really mention them and if they do, only 2-3 are discussed. I would agree, US Techs more profitable and wider moats. And I want to diversify into Tech Stocks for the growth aspect…at least a small portion of my portfolio due to my limited time horizon. I guess that is why I am leaning towards QQC.F to get some exposure to US tech. Profitable, but volatile.

Thanks Again

Hi John,

Another reason is that many Canadian tech stocks do not pay dividends, so the Canadian DGI bloggers don’t talk about these non-dividend paying stocks that much. I just think that if you want to get into tech and the more growth side of things, US offers slightly better opportunities compared to Canada. This is why we also own stocks like Alphabet, Amazon, Tesla, etc.

Hi Bob,

Great list and own all those holdings. I have been adding to AQN, ENB, SU this month. Also started a small position in Magna since it seems to be trading at discount right now.

For SRU the overall growth of the share price has been flat over the past 5 years and they didn’t raise dividends in 2021. Why do you prefer it over another REIT like an industrial REIT (i.e. granite) which seems to check all the boxes for dividend growth investors.

We already have a sizable amount of industrial REIT in our portfolio so looking at retail REITs instead.

Thanks for the post Bob!

You mentioned:

¨We plan to buy these stocks across all three of our accounts – TFSA, RRSP, and non-registered.¨

This is a question I had to myself if should duplicate some of my stock purchases in multiple accounts or not.

For example, I do have AQN in my RRSP, but wasn´t sure if I should also purchase in my TFSA. I was always wondering if it´s better to start a new position if I already own a stock in one of my other accounts, or just buy the stock in two or more accounts.

Your thoughts on this?

Thank you!

We do hold some stocks across different accounts. We see all these accounts as one big portfolio.

Great picks!. Own 4 of the 6 and have already added to AQN in the very low 17’s. Looking at SRU.UN but would have to sell something as I don’t want to increase my portfolio number.

Thanks. Makes sense to limit number of holdings in your portfolio.

Hi Bob

ENB is too risky now that is near to its higher value.

SRU.UN have been unstable in the last two years. There are other REITS with more upside like Granite.

AQN is not a the bottom yet. Renewables have been very complicated in the last six months.

These three stocks are only good if you buy them very low, if you made the mistake to buy high like ENB now and SRU. UN near to high, after the next deep you are going to waste time waiting for the recovery.

The dividends collected do not pay for the drop in price.

Agree on the points you’ve made but can’t just look at share price alone.

nice list Bob

Aqn and xaw are up there on my list.

cnr is currently our largest holding but if it gets cheap I’ll add =)

couchetard is growing on me, so I’ll definitely be adding to them. They just announced an even higher buyback.

keep it up

Nicely done on having CNR as one of your largest holding.

Might get into Couchetard one of these days.

Are you not conflicted by the investment in oil and gas companies vs the environment?

I’m trying to deleverage. If we let our children make laws, they would crush oil and gas. Renewable solar is 10x more advanced then predicted it would be just 10 years ago. We could switch, but we won’t until we legislate. Sad.

Hi Jon,

That’s a good point, I am conflicted but at the same time, it’s important to consider the reality. Oil and gas won’t go away any time soon so it makes sense for me to invest some portion of our portfolio in that sector. Having said that, we’re adding more and more renewables in our portfolio and slowly shifting away from oil and gas.

If our children crushed oil and gas they would give up their standard of living! Solar panels made from oil as well as many byproducts. It will be decades until fossil fuels are replaced. The infrastructure can’t support the electrical demand Electric cars would put on the grid. It will be a very slow transition.

If China and India not onboard it is futile.

Hi Dan,

I am optimistic that we’ll limit oil and gas use in the near future. We need to slowly move away from oil byproducts. It’s hard but we can get there one day. Let’s not make this into a political discussion.

Surprised to see that Fortis (FTS) is not on this list. Care to share why?

Fortis is a worthy buy for sure but thought these 6 I listed are more attractive at the time of writing.

Thanks Tawcan! I know you investigate your planned purchases carefully – what are your impressions about why Algonquin prices fell? Do you think this is temporary?

I feel the drop is across all renewable sector.

I think the market has concerns over AQN’s strategy over their latest distribution company acquisitions, particularly the one in Kentucky. Yes, AQN has built up a green energy generation portfolio but a huge amount of their revenue originates from local distribution companies providing energy and water to tens of thousands of customers. This is no different from what Fortis BC does (as an example). AQN gets a lot of credit for green energy generation,but it is only a segment of their business. I am a shareholder, but I also think there is room for another pullback. They really miss Ian Robertson as CEO.