One of the key steps for any financial independence retire early (FIRE) seeker is to invest in assets so one day you can live off these assets. Stocks are typically the preferred investment vehicle because of their liquidity and good returns.

While stocks provide about a 7% annual return over the long term, they can be volatile in the short term. The volatility means stocks are riskier and some people simply can’t sleep at night if their portfolio value drops by 5% or more. In addition, the volatility is an issue if you are living off your assets and need a dependable monthly income.

This is why one of the age-old rules of asset allocation is to increase your fixed income exposure as you get older. As their name suggests, fixed income investments like bonds, GICs, and money market funds will provide you with a dependable, fixed amount of income each month.

Mrs. T and I are still relatively young (in our mid 30’s), therefore, stocks make up the majority of our investment portfolio. But this does not mean that we are not investing in fixed income investments. I do believe that fixed-income investments like bonds, for example, have a place in everyone’s investment portfolio. The percentage of fixed income investments you hold within your portfolio will depend on your age, risk tolerance, and retirement timeline.

When it comes to bonds, the typical options are government, municipal, and corporate bonds with different levels of risks and returns. Usually, government bonds will give you the lowest yield and lowest risk while corporate bonds will give you the highest yield but at a higher risk. Municipal bonds sit somewhere the middle.

For investors looking for higher yields on their fixed-income investments and further asset diversification, private bonds may be a good option.

Investing with CoPower Green Bonds

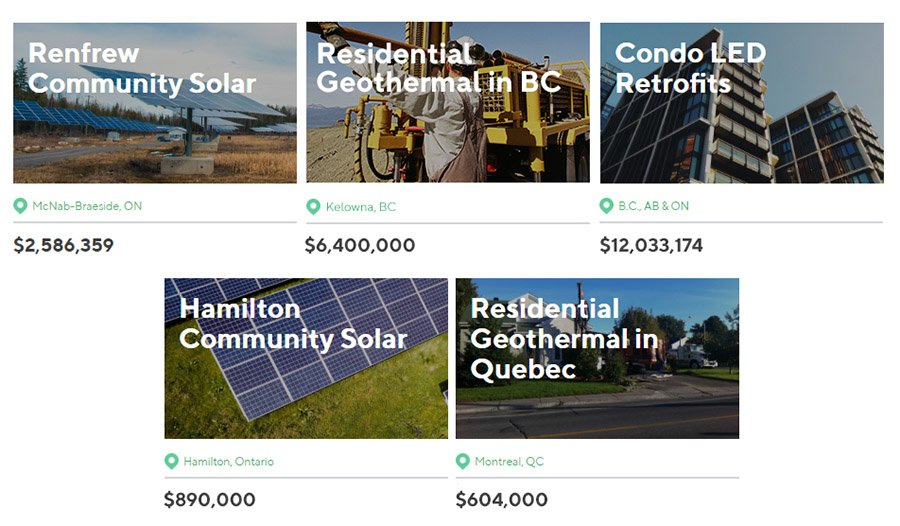

A while ago I wrote about CoPower Green Bonds which are a private fixed-income product backed by loans to clean energy & energy efficiency projects. The money raised through Green Bonds is used to lend to infrastructure projects like rooftop solar, geothermal, and LED retrofits.

As the stock market becomes more volatile and more and more indicators are hinting at a recession, in my opinion, it makes sense to diversify your investment portfolio. An investment like CoPower Green Bonds is a way I’m considering doing that.

Also, being environmentally conscious, I love how these Green Bonds are providing a positive impact on our environment by reducing CO2 emissions. The company reports that they’ve already helped avoid more than 6,000 tonnes of CO2 and investors get quarterly reports that include their positive impact.

You can invest in Green Bonds with as little as $5,000 (up to

Benefits of CoPower Green Bonds

While traditional, publicly traded bonds are liquid (CoPower Green Bonds are illiquid and must be held to maturity), I believe there are a few key benefits the Green Bonds have over these publicly traded bonds, especially today when markets are uncertain.

As you may know, there’s an inverse relationship between interest rates and bond prices. So when the Bank of Canada starts to raise interest rates to reduce inflation, public bond prices decrease. Because CoPower Green Bonds are private investments, they aren’t exposed to this interest rate-tied price fluctuations. The 5% return on their 6-year bond doesn’t change. For a $5,000 investment in a simple interest bond series, that means you could expect to receive $250 each year — that’s $1,500 in interest at the end of the 6 year investment period plus your $5,000 principal. Having the peace of mind of not having to worry about bond price fluctuations can be quite attractive for some investors.

In general, adding a private investment into your portfolio and one backed by infrastructure assets can help reduce volatility in your portfolio and protect your returns. The projects CoPower lends to will continue to save energy or generate solar power supporting loan repayments, whatever of what the stock market does.

Another benefit of CoPower Green Bonds, unlike most private investments, is that you can hold them inside your TFSA or RRSP. This means you can re-invest your interest & principal while being tax efficient.

For me personally, the key benefit of Green Bonds is the attractive returns. Canada 10 year bond yield rate is 1.99%, Canada 5 year bond yield rate is 1.92% as of Dec 20, 2018, Vanguard Aggregate Bond index ETF (VAB) has a 2.94% yield, and Vanguard Canadian Long-Term bond index ETF (VLB) is 3.62%. In comparison, the 6-year Green Bonds have a 5% yield and the 4-year Green Bonds have a 4% yield. So if you are looking for a higher fixed income, Green Bonds may be a suitable investment option for you.

That said, CoPower Green Bonds have more risk associated than government bonds which are considered low risk. For example, a wide-spread technical problem in one of the clean energy project portfolios could lead to a late payment or a loan default in an extreme circumstance. To reduce that risk CoPower often requires project owners to establish debt-service reserve funds and they ensure that warranties and insurance are in place when relevant. It’s nice to see that they report that to-date no loans have defaulted and all interest payments have been made on time, from borrowers to CoPower and from CoPower to investors. CoPower provides lots of information on their site and in their offering memorandum about other risks and how they work to mitigate them for investors.

A few more things to note

If you decide to invest with CoPower, you can purchase Green Bonds through their online platform with a very straightforward process. You don’t need to open up a brokerage account and pay trading fees. Although if you want to hold them in an RRSP or TFSA you need to do that through a financial institution and they may charge fees. CoPower’s site says that Questrade is the easiest and cheapest option.

The bonds invest in a diversified portfolio of many projects, so you don’t have to pick and choose which green projects to invest in making the investing process even more complicated. CoPower has already done the work for you. Right now the Green Bond portfolio includes loans supporting more than 1,100 individual projects.

Also, since Green Bonds are private investments, they must be held until maturity. In other words, Green Bonds can’t be sold on a secondary market or redeemed before the end of the term. This is very different than the Canadian government bonds or Vanguard bond index ETFs. So before you invest in Green Bonds, make sure you are OK with the 4 or 6-year terms, as you won’t be able to get your principal back until the end of the bond maturity. You’ll also have less reporting information to base decisions on than you do with public investments.

Final Thoughts

Being environmentally conscious, both Mrs. T and I have always liked the idea of green investing. For the right investor, Green Bonds not only offer the ability to invest green, they also provide further asset diversification with good yields.

If you are looking for something other than the standard investment options, I highly recommend taking a look at Green Bonds. You can learn more about CoPower and Green Bonds here.

This post was sponsored and solicited by CoPower. All thoughts and opinions are my own and may not be representative of the views of other investors or potential investors in CoPower Green Bonds.

Interesting sponsored post Bob. I’ve never heard of green bonds before. I always though if municipalities or corporations could offer bonds for a project (green or otherwise) and investors could select the projects they wanted to invest in.

Why would an investor want to invest in Copower’s green bonds vs. just buying the green project bonds directly? Is it just the number of green deals available?

Hi Mr. Tako,

The green bonds are pretty new and I wouldn’t have known it unless I met the CoPower team at CPFC a few years ago. This is the 2nd sponsored post I’ve done in the history of the blog and both posts were both with CoPower. I get approached A LOT by brands on sponsored post (I’m sure you too), and I’ve turned them all down (I’ve been extremely selective regarding sponsored posts). The only reason I’ve written about CoPower is because I believe the product.

Why would an investor invest in CoPower’s green bonds vs just buying the green project bonds directly? Mostly because the number of green projects associated to CoPower’s green bonds. But also it’s not so easy to find green project bonds here in Canada. 🙂