Income tax is one of those unavoidable things in life. If you have a working income, you most likely will need to pay income tax to the Canadian Revenue Agency (CRA).

Typically your employer will deduct taxes on your bi-weekly pay so you don’t end up with an amount owing when you file your income tax. However, if you have additional income from other sources like part-time work, side hustles, or investments, you may end up owing taxes to the CRA.

Since I like to plan (surprise!), I have been using online tax tools like Wealthsimple Tax and TaxTips since late 2023 to estimate if I would get a refund or if I would have to pay additional taxes. As we received various tax forms like T4 and T5 so far this year, I have been entering them into Wealthsimple Tax to understand where Mrs. T and I stand..

Thanks to my company equities, bonuses from the acquisition, and other side hustle incomes, it looks like I will owe some money to the CRA for the 2023 income tax.

Owing money to the CRA sucks but I guess that’s better than getting a tax refund – because getting a tax refund essentially means you’re loaning money to the CRA at zero interest.

Since one of my annual goals is to travel hack to earn $2,000 equivalent of points, it makes me wonder, is it possible to pay income tax with a credit card? If so, does it make sense?

How to pay the CRA

First of all, how can individuals make a payment to the CRA when they owe taxes?

Since the good old paper filing of income taxes is mostly gone (thank god!), replaced by digital filing via NETFILE, the CRA has made paying tax owing much simpler.

Per the CRA, you can make a payment with the following methods:

- Online banking – pay a payment or schedule future payments to the CRA through Canadian bank or credit union mobile banking app or website.

- Pre-authorized debit (PAD) payments – you can set up a payment schedule or single payment directly in CRA’s My Account to authorize the CRA to withdraw set amount(s) from your Canadian chequing account.

- Debit card payments – Use CRA My Payment service to make payments directly using your bank access card

- Wire transfer and internationally issued credit card payment (for non-residents) – this is only possible for non-residents who don’t have a Canadian bank account

- At bank or credit union – physically pay taxes at your bank or credit union by cheque or debit

- Post office – pay at a Canadian Post location by debit or cash. Canada Post charges a fee for this service

- Pay by mail – send a cheque or money order with your remittance voucher

- Credit Card, Paypal, Interact e-Transfer payments – this can be done via a third-party service provider. → Bingo!

How to pay income tax with a credit card

So yes, it is possible to pay income tax with a credit card but you have to do it with a third-party service provider.

The CRA has listed PaySimply as the only third-party service provider they will accept. PaySimply accepts a variety of payments like debit cards, credit cards, Union Pay, Paypal, and Interac e-Transfer.

You used to be able to pay the CRA using Plastiq but this is no longer supported. You can, however, still use Plastiq to pay all of your other business expenses.

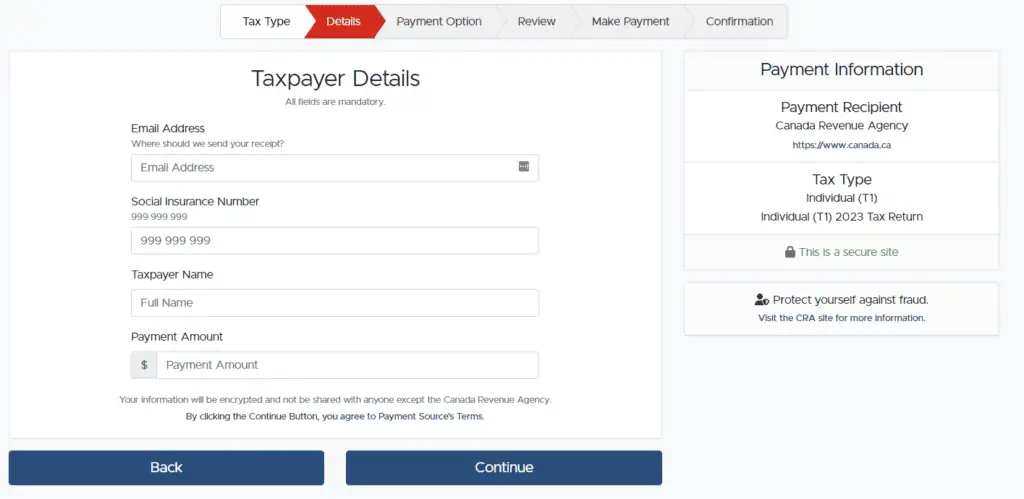

Paying income tax with PaySimply

PaySimply is a very user-friendly platform to pay the CRA. There’s no need to set up an account. You simply follow the prompts, provide your email address for your receipt, social insurance number, name, payment amount, and then your payment option.

Since PaySimply has been vetted by the CRA, the transaction is valid and secure.

How much does PaySimply cost?

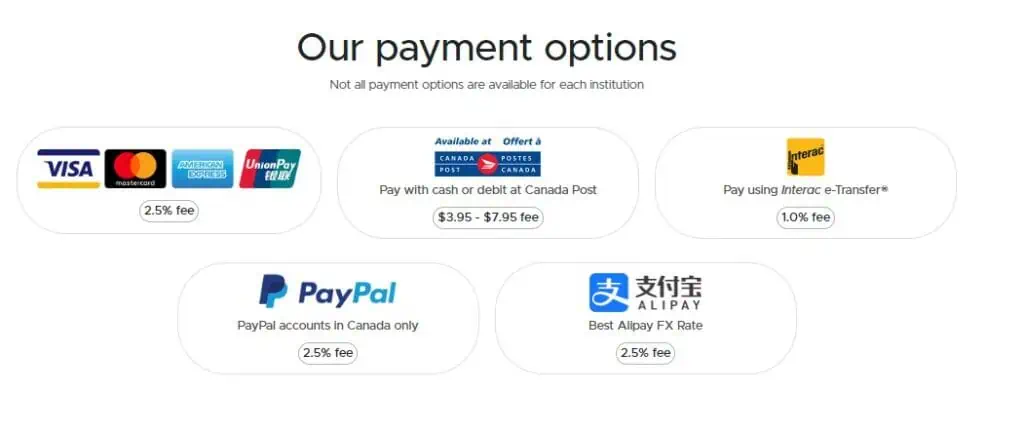

While it’s convenient to pay taxes using a credit card through PaySimply, the service isn’t free. PaySimply charges the following fees:

- Visa, Mastercard, American Express, Union Pay: 2.5% fee

- Pay with cash or debit at Canada Post: $3.95 – $7.95 fee

- Pay using Interact e-Transfer: 1% fee

- PayPal: 2.5% fee

- AliPay FX: 2.5% fee

So, if we pay the tax owing using a credit card through PaySimply, we’d have to add a 2.5% fee on top. For example, if we owe $1,000 in taxes, we’d have to pay another $25, or $1,025 in total.

Interestingly, PaySimply allows you to pay property taxes, utility, tuition, rent, and even business invoices through them. The same fees apply to these payees.

Does it make sense to pay the CRA with a credit card?

Does it make sense to pay the CRA with a credit card given the 2.5% fee that PaySimply charges?

That would depend on which credit card you have. Since no credit card has an earn rate of more than 2.5%, you wouldn’t get more money back in credit card rewards. So it’s not worth it at all.

Note: If you have at least one Rogers/Fido/Shaw service, then the Rogers Mastercard and Rogers World Elite Mastercard you potentially give you 3% cash back if you redeem the points on a Rogers/Fido/Shaw purchase charged to the card.

Since many credit cards have a spending requirement to get the welcome bonus points, I believe this is the only occasion where it’d make sense to pay the CRA with a credit card. The large tax owed may help you to meet the spending requirements and qualify for the welcome bonus points.

Welcome Bonus Points – some scenarios

I decided to run a few different scenarios, do some calculations, and see whether it makes sense to pay taxes using a credit card via PaySimply.

For the calculations, I will assume that we owe $5,000 in taxes. Using PaySimply means we’d have to pay an extra $125 in fees.

Scenario 1 – Marriott Bonvoy American Express Card

Right now you can apply for the Marriott Bonvoy American Express Card (my referral link) and earn 70,000 Marriott Bonvoy points after spending $3,000 on the card in the first three months of card membership. The $5,000 tax owing will cover the $3,000 spending requirement right away.

Per Prince of Travel, one Marriott Bonvoy point is worth 0.8 cents CAD. So 70,000 Bonvoy points are equivalent to $560.

The card has an annual fee of $120 and you’d pay $125 in fees for using PaySimply.

Therefore, in this scenario you’d end up with a net of $315, making it worthwhile to pay the $5,000 in tax owing with a credit card via PaySimply.

Scenario 2 – American Express Platinum Card

You can get 70,000 Amex MR bonus points after you spend $10,000 in net purchases in the first three months of card membership. $10,000 is a pretty significant amount of money in three months so it’s a good idea to only apply this card when you know you have upcoming big expenses.

The $5,125 in tax spending will cover slightly over the spending requirement. Assuming you can hit the $10k spending limit, at 2.2 cents CAD per Amex MR point, the 70,000 Amex MR points are worth $1,540. If you were to transfer these MR points to Aeroplan at a 1:1 rate, you’d end up with the equivalent of $1,470 (2.1 cents CAD per Aeroplan point).

American Express Platinum Card has an annual fee of $799 but you get a $200 annual travel credit and $200 annual dining credit, reducing the annual fee down to effectively $399. For this calculation, I will ignore the money equivalent of unlimited airport lounge access.

Therefore, in this scenario, you’d end up with a net of $1,016 ($1,540 – $399 – $125) if you redeem via Amex Fixed Points Travel. If you redeem via Aeroplan, you’d end up with a net of $946 ($1,470 – $399 – $125).

Scenario 3 – Scotiabank Passport Visa Infinite

With Scotiabank Passport Visa Infinite, you’d get 30,000 Scene+ points by making at least $1,000 in everyday eligible purchases in your first 3 months. The $5,000 tax owing will easily cover the spending requirement.

At 1 cent per Scene+ point, 30,000 Scene+ points are worth $300. You get six complimentary airport lounge access but we’ll ignore the dollar value for this calculation.

The Passport Visa has an annual fee of $150. Therefore, you’d end up with a net of $25 ($300 – $150 – $125). While you come out positive, I’d argue it’s not worth paying taxes owing with Passport Visa Infinite just to earn the welcome bonus points.

Scenario 4 – TD Aeroplan Visa Infinite Card

The TD Aeroplan Visa Infinite Card has a 40,000 Aeroplan welcome points offer after you spend $5,000 within 180 days of account opening. Right now the first year annual fee is waived.

At 2.1 cents per Aeroplan point, 40,000 Aeroplan points are worth $840. Subtracting the $125 PaySimply fee means you’d end up with a net amount of $715.

Scenario 5 – TD First Class Travel Visa Infinite

Currently, you’d earn 135,000 TD Rewards Points after spending $5,000 within 180 days of account opening. Like the TD Aeroplan Visa Infinite Card, the first year annual fee is waived.

At 0.5 cents per TD Rewards Points, 135,000 TD Rewards Points are equivalent to 675. Subtracting the $125 PaySimply fee means you’d end up with a net amount of $550.

As you can see from the five scenarios above, by paying taxes using a credit card and earning welcome points, you can earn upward of over $500. This is worthwhile if you can pay off the balance at the end of the month and not pay any credit card interest.

If the amount taxes owing is a much smaller amount where you won’t hit the spending requirement at all, it may not be worth paying with a credit card.

Paying the CRA with a credit card – Pros & Cons

You also have to consider the pros and cons of paying taxes with a credit card.

Pros

- Welcome bonus – paying with a credit card can help you meet the spending requirement and qualify for the welcome bonus

- Payment is processed instantly – payment is processed instantly, you don’t have to wait for a day or two for the payment to go through

- Gain some time – since you don’t have to pay your credit card balance until the statement payment date, you can gain some time and may earn interests with the money sitting in your bank

Cons

- 2.5% fee – this eats into your potential “returns”

- Credit card interest – if you don’t pay the balance in full, you will end up paying a very high interest rate

- Impact on credit score – if you don’t pay the balance off, your credit score may be negatively impacted

Like what I have demonstrated in the different scenarios, you need to do your calculations to determine whether it makes sense to use a credit card to pay taxes, and you also need to understand the pros and cons.

Summary – How to pay income tax with a credit card

Can you pay income tax with a credit card? Absolutely! You can use PaySimply to pay the CRA. You can also use PaySimply for utility, property taxes, tuition, rent, and even business invoices.

For the most part, it is not worth paying your income taxes with a credit card as the 2.5% fee from PaySimply is much larger than what you get from credit card earning rates. This means you end up paying more out of pocket.

However, if you can find a credit card with worthwhile bonus points, it may make sense to pay income taxes using a credit card.

For us, we need to do a bit more homework to decide whether to pay income taxes via online banking or a credit card.

Have you paid the CRA with a credit card in the past?

One other option is using Canadian Tire Triangle MasterCard – I stopped a lot of our direct payments out of the chequing account for utility bills, property tax, university tuition, etc and started to make payments with the Canadian Tire card. It’s only 1% but it can add up because it’s treated like a regular bank account not a MasterCard. So no 2.5% fee. I’m assuming CRA is on the bill pay (I haven’t checked). It’s better than paying directly from a bank account. With your example, it would = $50 of points, which could be used for clothes, shoes, gas, gardening tools, etc. Not as much as your examples, but it’s something!

You can’t pay the CRA with Canadian Tire Triangle MasterCard though. You can on utility bills, property tax, tuition, etc like you mentioned.

Sounds like a lot of effort for little gain. We have the RBC Avion Visa. We do use it for practically everything (except Costco). We have used the points many times to save on airfare. I got my CRA refund already but my partner owes – we will wait until the last possible day (April 30th) to pay it.

The extra fees usually make this not worth it. If you have a big tax bill and you’re looking to hit the spending requirements for a credit card, this might be worthwhile to look into.

I thank you as one of the lucky few, like me , that has to pay net tax to the CRA to keep this country running . Everyone else seems to get a refund .

Pay Simple would be a good company to invest in. Gets 2.5% on every transaction for doing little. But it looks like a private company.

All I can say is thankfully I own the banks RBC, TD, CIBC instead of working for the banks and they are doing a great job like Pay Simple of collecting profits on every transaction for my rising dividends.

I had it with points on cards and never being able to redeem points due to changes in rules .

I’m happy with a no fee cash back CC.

We’re owing about $20K to CRA this year due to some capital gains and dividends but we’ll just pay them directly this year .

Well having to pay net tax to the CRA is a good thing. Getting a refund means you’re loaning the government tax free.

Wow owing $20k to the CRA… that’s a lot. 🙂

You should try the Smith Manoeuvre!