I always get excited at beginning of each new year, because a new year means new TFSA contribution room for eligible Canadians. Although TFSA is inflation indexed, we won’t see an increase in 2017. The 2017 TFSA contribution limit will remain to be $5,500. Therefore, between Mrs. T and I, we can contribute up to $11,000 in our TFSA. Since we are utilizing dividend growth investing as our core investing strategy, we plan to use all $11,000 to buy Canadian dividend paying stocks. What to invest in TFSA? Here are some Canadian dividend stocks that I am considering.

What to invest in TFSA?

Why are we only considering Canadian dividend stocks and not US dividend stocks? Because if we invest US dividend stocks in TFSA we will need to pay 15% withholding tax on dividends. To be as tax efficient as possible, we only invest Canadian dividend stocks inside our TFSAs.

Since we are a bit overweight on financial sector in our dividend portfolio, I would like to re-balance our portfolio by adding dividend paying stocks in other sectors. Below are stocks we are considering for our TFSA.

BCE Inc (BCE.TO)

BCE provides a range of wireless, wire-line, Internet, television services, and content services to consumer, residential, business and government customers in Canada. The company is divided into different business segments – wireless, media, and wirelines. Bell and Bell Aliant brands offer wireless, high-speed Internet services, and home phone and business network communication services. Bell Media is the television and radio content provider in Canada. Lastly, Bell Wirelines provides data, local telephone and long distance, and other communications services and products.

A few years ago BCE expanded its empire by investing in the Montreal Canadiens and Maple Leaf Sports and Entertainment. BCE is also the owner behind The Source, one of Canada’s largest consumer electronics retailers.

Why purchase BCE Inc.

BCE stock price has retrieved slightly the last few months. BCE has managed to grow its dividend payout for 7 straight years with a respectable 5 year dividend annual growth rate of 7.8%. At a PE ratio of 18.5, it is not the cheapest stock but cheaper compared to its competitors Rogers Communication and Telus. I like BCE because it has vast empire and the stable business. Canadians are hooked on data, television and radio contents. BCE is in a good spot to continue racking in the revenues from Canadians.

Potential Risks

BCE revenue growth has slowed down over the past few years. The company, however, continued to increase its dividend payout. Hence the dividend payout ratio is now at a staggering 86%. This indicates that the dividend growth will most likely to start slow down in the future. I believe the mobile industry in Canada is very mature. BCE has already captured significant amount of the business. It’s unlikely it will all of a sudden gain large amount of subscribers. In addition, there’s always risk of another competitor entering the space and disrupt the market. For example, when Verizon announced the intention to enter the Canadian market 2 years ago, that sent BCE stock price tumbling. Shaw recently acquired Wind Mobile and is planning to boost its stake in the wireless market. We have to wait and see what kind of impact this will do to BCE’s revenue.

Canadian Tire Corporation (CTC-A.TO)

If you live in Canada, I am sure you have been to a Canadian Tire store or seen one of the odd yet funny Canadian Tire commercials. Canadian Tire Corporation is a Canada-based company that operates through different segments including retail, REIT, and financial services. The Retail segment operates retail banners, including Canadian Tire, PartSource, Petroleum, Mark’s and various FGL Sports banners. The REIT segment is engaged in owning, developing and leasing income-producing commercial properties. The financial services segment markets a range of Canadian Tire-branded credit cards to Canadians.

Why purchase Canadian Tire

Canadian Tire currently trades at a PE ratio of 15.65, a dividend yield of 1.88%, and a payout ratio of 29.5%. While the dividend yield is pretty low, Canadian Tire has managed to grow its dividend payout at 20.1% over the last 5 years. Based on discounting future cash flows to present value, the current stock price of $141 appears to be undervalued. In the past 5 years, Canadian Tire has grown its earnings by 10.3%. At 12.85% return on equity, Canadian Tire should be able to continue to grow.

Potential Risks

Like all retailers, Canadian Tire is dependent on consumer making purchases at their stores or using one of their services. The company faces a lot of competitions within Canada from other physical retail stores and also other online retailers. Because Canadian Tire stores do not sell too many premium products, there isn’t much product differentiation between Canadian Tire and other competitors. In other words, there’s low consumer brand loyalty. Consumers are as likely to shop at Canadian Tire as its competitors. Price often becomes the deciding factor on where to shop. Can Canadian Tire remain price competitive while continue growing its profits?

Hydro One (H.TO)

Hydro One transmits and distributes electricity across Ontario. The company operates 97% of the high voltage transmission grid through Ontario and serves 1.3 million customers. Hydro One went public in Nov 2015.

Why Purchase Hydro One

Hydro One has a monopoly in electricity transmission and distribution in Ontario, the largest province in Canada. The 1.3 million customers represents a stable source of strong and growing cash flow. Being a utility company, the growth is predictable. The company can easily increase its revenue by increasing the electricity rate. Hydro One board plans a 70-80% dividend payout ratio moving forward. Currently yielding around 3.6% and a payout ratio of 73%, there are some rooms for future dividend growth.

Potential Risks

Being an utility company, Hydro One faces a lot of regulations. To increase its electricity rate requires multi-stages of approvals. Since Hydro One just went public in 2015, there has been no dividend growth history. As a dividend growth investor, there’s no guarantee that the dividend payout will continue to grow at a reasonable rate.

Fortis (FTS.TO)

Fortis is a Canadian based electric and gas utility company and a leader in the North America utility industry with assets of $47 billion and 2015 revenue of $6.7 billion. The company serves customers in five Canadian provinces, nine US states, and three Caribbean countries.

Why Purchase Fortis

Fortis has a large customer base of over 3 million customers in Canada, the US, and the Caribbean. It has an impressive 42 years of dividend increase streak, the second longest among all Canadian dividend paying stock. The stock currently trades at a PE ratio of 22, a dividend yield of 3.88%, and a payout ratio of 86.5%. The PE ratio is a bit higher than my liking but utility stocks seem to be trading at a slight premium nowadays. A stable business and a stable dividend payer, I feel that I can almost treat Fortis like a bond. The stock price has come down slightly over the last few months. Adding some Fortis shares while the price is slightly lower may serve well in the long term.

Potential Risks

Fortis’ future growth is limited, unless the company continues to acquire other utility companies. At a PE ratio of 22, it is not the cheapest stock in the market. Although Fortis has a 1 year dividend growth rate of 9%, the 5 year dividend growth rate is a low 4.5%. At a payout ratio of 86.5%, high dividend growth probably shouldn’t be expected.

H&R REIT (HR.UN)

H&R REIT is the largest diversified REIT in Canada with a market cap of $6.7 billion. H&R REIT’s portfolio consists of 38 office properties, 156 retail properties, 102 industrial properties, 10 residential properties and 4 development projects with a total value of approximately $14.5 billion, comprising over 44 million square feet of lease space.

Why Purchase H&R REIT

H&R REIT has managed to increase their distributions semi-regularly, which is something we do not see often in the Canadian REIT space. The company is fairly diversified geographically with 31% of its properties in Ontario, 27% in Alberta, 11% in other Canadian Provinces, and 31% in the US.

The top 15 tenants are all large corporations, including Encana, Bell, Hess Corporation, New York City Department of Health, Canadian Tire, and Telus. All these corporations have long term lease and compose ~51% of H&R REIT’s rental income. Last time I checked, big corporations are very unlikely to move their offices, which is a good news for H&R REIT.

Financially H&R REIT is doing quite well. It has a solid occupancy rate of ~96%, a FFO per unit of $1.48, and a 68.2% payout ratio as percentage of FFO in Q3 2016. The 68.2% payout ratio is a great sign that H&R REIT will be able to continue raising its dividend payout in the future. In fact, H&R REIT has increased distributions by $0.03 per unit from $1.35 to $1.38 per year.

Potential Risks

Like all REITs, H&R REIT is sensitive to interest rate changes. With US Fed planning to increase interest rates 3 times in 2017 and Bank of Canada may follow suit, this will have a negative impact to H&R REIT.

Smart REIT (SRU.UN)

Smart REIT, formerly known as Calloway REIT, focuses on retail and mixed-use asset classes. With $8.6 billion total asset value, 141 shopping centres and 1 office tower across Canada, and a total gross leasable area of over 31.3 million square feet, Smart REIT is the 3rd largest REIT in Canada by market capitalization.

Why purchase Smart REIT

As of Q3 2016, Smart REIT enjoys an occupancy rate of 98.5% with 72% of the properties anchored by Walmart. Smart REIT has also managed to increase its payout for the past 3 years while growing its assets and revenues. The company has enjoyed a compounded annual growth rate of 8.8% in rental revenue since 2011 and a CAGR of 4.9% in AFFO since 2011. Most impressively, the company has a CAGR of 38.2% in total assets since 2002. At a dividend yield of 5.22% and a payout ratio of 81% to AFFO, Smart REIT appears to be a solid pick for dividend income.

Potential Risks

Similar to H&R REIT, Smart REIT is also sensitive to interest rate changes.

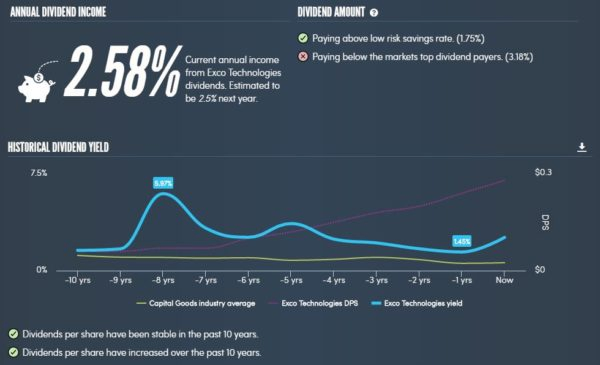

Exco Technologies (XTC.TO)

Exco Technologies is a designer, developer and manufacturer of dies, molds, components and assemblies, and consumable equipment for the die-cast-extrusion and automotive industries. Operating in 18 locations including Canada, US, Mexico, Colombia, Brazil, Thailand, Germany, and South Africa, the company has a diverse and broad customer based through three business groups: Automotive Solutions, Extrusion Tooling Solutions and Die Cast Solutions.

Exco Technologies acquired AFX Industries in early 2016. The completed acquisition nearly doubles company’s interior trim business sales. The auto interior trim industry is currently composed of primarily highly fragmented small companies. Doubling the interior trim business allows Exco Technologies to emerge as one of the leaders in this industry.

Why Purchase Exco Technologies

Exco Technologies jumped out when I was going through the Canadian Dividend All Star List. I was very impressed that the company has managed to grow its dividend payout for 10 straight years at a 10 year growth rate of 17% and a 5 year growth rate of 23.1. This means that XTC has manage to grow its dividend payout more in recent years. At a low payout ratio of 25%, Exco Technologies should be able to continue its impressive dividend growth for many years to come. At a PE ratio of 10, a dividend yield of 2.5%, a PEG ratio of 1, and a future cashflow of $20.02, the stock price appears to be undervalued.

Upon further research, I found that Exco Technologies focuses on the luxury auto manufacturers so the sales is less volatile than consumer brands. It has facilities in Mexico, Morocco, and Bulgaria which allows Exco Technologies to keep its operation cost down. Exco Technologies has a strong balance sheet with very little debt compared to its peers Martinrea and American Axle. All these factors mentioned already makes Exco Technologies even more attractive to invest in.

Potential Risks

Exco Technologies, having facilities in many countries, faces currency exposures. Changes in currency value may have a negative affect to company’s profitability. In addition, auto industry is cyclical so Exco Technologies may face headwinds during an economic downturn.

Conclusion

These are the stocks I am considering adding to our TFSA using the 2017 contribution room. As you can see, I’m monitoring a mix of high yield lower growth and low yield higher growth stocks. I believe it’s important to have a healthy mix of high yield lower growth and low yield higher growth dividend paying stocks.

Dear readers, what are some stocks that you are monitoring?

Great advice! I am a new investor and wondering how much of each stock you normally purchase? For example, is $1,000 sufficient to invest in any of the mentioned companies? Or should you buy in larger chunks?

I always suggest making sure the commission is less than 1% of your overall transaction. So $1,000 is roughly sufficient amount of invest if the trading commission is less than $10. If you can, I would suggest buying 100 shares each time.

Just crossing by your web site and like it. The following CUF-UN.TO, STB.TO, EXE.TO and RY.TO can be considered in TFSA. I got them in my porfolio and quite happy so far. Thank you for the Dividend Spreadsheet Tutorial, very helpful. Good job TAWCAN!

Ricky.

Great picks, technology and REITs are 2 great sectors to be in. If you don’t want to do rental property, REITs is a great way to go as the dividend are much higher and headache free.

Thanks for sharing your watchlist, bro!

Ah, I see the change on your website, finally see how one of the Tawcan look LOL 🙂

Cheers!

Thanks Vivianne. We like REITs so we don’t have to deal with rental properties.

I’ve got my eye on Algonquin Power and Utilities (AQN). Canadian company servicing the American market with renewable energy sources. Nice dividend track record and Canadian eligible dividends paid in USD. Just raised the dividend 10% and has a current yield north of 5%! YMMV

AQN is looking interesting for sure. Don’t like the fact they cut dividends 5 or so years ago now they’re back to aggressive dividend increases.

new reader here … always looking for good stocks at good prices … as a mechanical engineer just to assure you that die and mould is really big part of plastic production die can never be obsolete until ppl use plastic products.

my investing style is that i am always looking for bargain as i will never invest when stock price is 52 week high as most of the stocks are at that stage now .. whats your opinion on that … just curious ..

TIA

I thought die and mould are still big part of plastic production as well. But Mr. Tako brought up a good point that Chinese companies may be able to do it for cheaper.

In terms of investing when stock price is 52 week high… I try not to invest at that point either. But the thing is, you can’t just look at the price alone, you need to look at the stock evaluation and future growth. Because the stock price can just keep going up and you’d miss a great opportunity.

I don’t know if you invest in closed end funds but I am watching FAP on the tsx Aberdeen asia-pacific income fund. I will likely add this one to my TFSA soon. I use the closed end funds for higher returns as long as they are below NAV

Hi Ken,

I have not looked at FAP before, will take a closer look.

Some interesting picks there Tawcan, several of which I’ve never heard of…which is no surprise as these are Canadian companies.

Exco Technology stands out to me as an interesting pick, but I’ve heard from friends that work in manufacturing that die/mold production of parts is dying out. (at least metal parts) It’s now getting cheaper to CNC many parts with higher precision. I’m not certain if Exco would be affected by this trend.

Hopefully these are good picks lol. Good point about Exco Technology. From my research looks like they are branching out with interior trim business which take quite a bit of expertise. True that CNC will do die/mold production of parts for cheaper so we definitely need to keep an eye on Exco if we were to purchase this stock. It’s a shame that Canadian dividend stocks are so focused on financial and energy. It’s tough to diversify with such restriction. 🙂