As you may know, we are a single-income family where I work full-time and Mrs. T stays home with the kids. For the time being, Mrs. T is staying home with the kids to spend more time with them. Given our single income situation, I have always wondered what’s the actual financial cost of a stay-at-home parent. Therefore, I decided to reach out to Chrissy at Eat Sleep Breathe FI about writing a post and analyzing how much does a stay-at-home cost?

She has been a full-time-stay-at-home mom for 14 years. She agreed with me that this would be a very interesting exercise. Rather than a generic article, I requested Chrissy to provide as many numbers as possible (I really pushed her comfort zone with this request hehe!). I wanted to make sure that we cover as many potential scenarios as possible with a lot of calculations (because I’m a numbers nerd). Hopefully we didn’t miss out anything.

In case you’re wondering, this LONG article took a lot of back and forth between the two of us before it became ready. I have to thank Chrissy for putting up with all my demanding suggestions, ha!

Take it away Chrissy!

Thank you Tawcan. As mentioned, I’ve been a full-time stay-at-home mom since my first son was born 14 years ago. Interestingly, I’ve never taken the time to calculate the cost of that decision… until now!

With this article, I go in-depth to calculate the costs and benefits of a stay-at-home parent by:

- Outlining the financial and lifestyle benefits.

- Analyzing the opportunity costs.

- Revealing the real cost of a stay-at-home parent.

At the end of it, you’ll have all the numbers—and a clearer idea of whether this is the right choice for your family.

Disclaimers

I realize that the choice to stay home (or not) is a sensitive, emotionally-charged topic. As I wrote this article, I tried to be cognizant of this. Additionally:

- Stay-at-home parenting isn’t right for everyone. It’s a personal decision that every family needs to make for themselves.

- Not everyone has the choice for one parent to stay home. I acknowledge that I’m fortunate to have this privilege.

- This article is in no way meant to judge other parents. I equally support and cheer on working and at-home parents; single and dual-income households.

- I made every attempt to be thorough and accurate with the numbers. (I used a combination of my actual numbers and numbers from reliable online sources.)

- Where possible, I used average/typical scenarios for my analyses. If this information wasn’t available, I used scenarios based on my personal experience.

- In my experience, dual-income households have little time to optimize their finances. However, some do manage to do this! If that’s the case, the numbers shown here may not apply.

With that, let’s get into the numbers!

Part 1: Financial benefits

Based on my experience, here are some of the ways that having a stay-at-home parent can save money:

1. Childcare costs

Families with a stay-at-home parent realize the greatest amount of savings in childcare costs. Let’s take a look at average childcare costs for children from 1 to 12 years old.

Assumptions:

- Childcare costs based on Vancouver, BC, or Canadian rates from:

- Canadian Centre for Policy Alternatives (daycare costs)

- Canadian Nanny (nanny costs)

- City of Vancouver Recreation (day camp costs)

- Both parents work 40 hours per week, Monday–Friday.

- No childcare help from grandparents or other family.

- Parents opt for one year of parental leave, so childcare isn’t needed until 12 months of age.

- Daycare is the same monthly rate—regardless of holidays, sick days or vacations.

- Due to decreasing need for adult supervision, daycare rates decrease as a child ages. (Strangely, Vancouver’s average toddler rate is slightly higher than the infant rate.)

- These are the typical daycare age groupings:

- Infants: 0-18 months

- Toddlers: 19-36 months

- Preschoolers: 3-5 years

- Before and after-school care is covered by parents staggering their work hours.

- For day camps:

- In dual-income households, 8 weeks per year of day camps are needed to cover spring and summer breaks. (Based on 8 weeks of summer camp plus 2 weeks of spring break camp minus 2 weeks of family vacation during one of the breaks.)

- In households with a stay-at-home parent, most still put their kids in a few weeks of day camps. Typically, they’ll book 1 week of all-day camp over spring break and 2 weeks over summer break.

- For full-time live-in nanny costs, my research shows the average pay increase per child is $1/hour, from average base pay of $13/hour.

Scenario 1: Full-time stay-at-home parent

- 0-4 years old: $0

- 5-12 years old: $300/week for 3 weeks of all-day camp per year for 8 years = $4,800

- TOTAL: $4,800 for 12 years = average of $400/year/child

Scenario 2: Daycare and camps

- 12-18 months: $1,400/month for seven months = $9,800

- 19-36 months: $1,407/month for 17 months = $23,919

- 3-5 years: $1,000/month for 24 months = $24,000

- 5-12 years: $300/week for 8 weeks/year for 8 years = $19,200

- TOTAL: $76,919 for 12 years = average of $6,409/year/child

Scenario 3: Full-time live-in nanny

- Base pay (includes room and board):

- One child: $13/hour x 40 hours/week = $520/week

- Two children: $14/hour = $560/week

- Three children: $15/hour = $600/week

- PLUS Employer contributions to CPP and EI

- One child: $70/week

- Two children: $76/week

- Three children: $82/week

- TOTALS:

- One child: $520 + $70 = $590/week x 52 weeks = $30,680/year

- Two children: $560 + $76 = $636/week x 52 weeks = $33,072/year

- Three children: $600 + $82 = $682/week x 52 weeks = $35,464/year

Comparison

Let’s put the numbers together and compare the annual costs for one, two, or three kids:

| Scenario 1 | Scenario 2 | Scenario 3 | |

| One child from 1-12 years old | $400 | $6,409(+$6,009 vs Scenario 1) | $30,680(+$30,280 vs Scenario 1) |

| Two children from 1-12 years old | $800 | $12,818(+$12,018 vs Scenario 1) | $33,072 (+$32,272 vs Scenario 1) |

| Three children from 1-12 years old | $1,200 | $19,227(+$18,027 vs Scenario 1) | $35,464 (+$34,264 vs Scenario 1) |

Average savings: $12,818/year

Based on the cost of daycare and camps for two children, families with a stay-at-home-parent save an average of $12,818 per year in daycare costs or $32,272 in nanny wages.

Families with three children stand to save a whopping $18,027 per year in daycare costs or $34,264 in nanny wages.

2. Food costs

When both parents work full time, it can be challenging to do all the things needed to cook at home (meal planning, grocery shopping, meal prep, etc.) Throw in kids’ activities in the evening, and it’s all but impossible to prepare home-cooked meals some days!

With one parent at home full time, it’s far more feasible to homecook most meals. Let’s see how much can be saved by eating out less often:

Assumptions:

- Assume each home-cooked meal costs $10 for a family of four, or $2.50 per person per meal. (Results in a $900 grocery bill per month)

- $100 for a restaurant dinner for a family of four.

- $12.50 for an average workday lunch.

- 90 total meals per month (3 meals per day * 30 days)

Scenario 1: One meal out per month

This scenario assumes one parent is at home full time and can cook most meals at home. The working parent would bring lunch to work every day.

- 1 restaurant dinner per month

- 89 home-cooked family meals per month

Total: [ $100 + 89*10 ] * 12 = $11,880 per year

Scenario 2: Two meals out per week + Two lunches out every workday

In this scenario, since both parents work full time, the family eats out twice per week. Additionally, both parents buy lunch every workday.

- 2 restaurant dinners per week (8 per month)

- 2 lunches out every workday (20 per month x 2 parents)

- Home-cooked meals per month: 61 for the parents, 82 for the kids

Total: [ $100*8 + $12.50*20*2 + 62*2.50*2 + 82*2.50*2 ] * 12 = $24,240

Comparison

Let’s put the numbers together and compare the costs:

| Scenario 1 | Scenario 2 |

| $11,880/yr | $24,240/yr |

Average savings: $12,360/year

Families with a full-time stay-at-home-parent save an average of $12,360 per year in food costs compared to families with two full-time working parents.

3. Vehicle expenses

When both parents work outside the home, chances are each will need a car to commute to and from work. This creates increased car expenses due to:

- Higher insurance costs.

- Higher gas costs.

- Higher maintenance costs.

Let’s take a look at how these increased expenses add up.

Assumptions:

- The cost of the car purchases is not considered in this calculation.

- Mileage:

- Each working parent’s commute is 20 km each way, resulting in 10,000 km per year.

- For errands/kids’ activities/events/weekend getaways: 7,500 km per year (based on my personal experience).

- For vehicles used for daily commute and errands: 15,000 km per year (10,000 for commuting plus 5,000 for errands.) This errand mileage is lower than a vehicle solely for this purpose since some errands are on the way to/from work.

- Insurance, gas, and maintenance costs are based on a 2014 Honda Civic.

- Gas is $1.50/litre and gas mileage is 9 litres/100 km.

- Oil changes are $125 each (tax included).

- Major servicing and repair costs average out to $400/year, based on my personal experience.

- Insurance costs based on:

- $2,000,000 in liability coverage.

- $2,500 deductibles for collision and comprehensive.

- Vehicle use:

- To/from work over 15 km (for daily commute vehicle): $2,100/year

- Pleasure use only (for errand vehicle): $1,985/year

Scenario 1: One car for the family

- Mileage:

- Commuting: 10,000 km/year

- Pleasure use: 5,000 km/year

- TOTAL: 15,000 km/year

- Insurance cost: $2,100/year

- Gas cost: $2,025/year

- Oil changes: $125 x 2/year = $250/year

- Major servicing, repairs, other maintenance: $600/year

- TOTAL: $2,100 + $2,025 + $250 + $600 = $4,975

Scenario 2: One car for daily commute + One car for errands, kids’ activities

One vehicle will be used for daily commuting only. The other will be used for errands/kids’ activities/weekend events and getaways.

- Mileage:

- Vehicle 1: 10,000 km/year

- Vehicle 2: 7,500 km/year

- Insurance cost:

- Vehicle 1: $2,100/year

- Vehicle 2: $1,985/year (lower cost because no work commute counts as pleasure use)

- Gas cost:

- Vehicle 1: $1,350/year

- Vehicle 2: $1,013/year

- Oil changes:

- Vehicle 1: $125 x 1/year = $125/year

- Vehicle 2: $125 x 1/year = $125/year

- Major servicing, repairs, other maintenance:

- Vehicle 1: $400/year

- Vehicle 2: $300/year

- Sub-totals:

- Vehicle 1: $2,100 + $1,350 + $125 + $400 = $3,975

- Vehicle 2: $1,985 + $1,013 + $125 + $300 = $3,423

- TOTAL: $3,975 + $3,423 = $7,398

Scenario 3: Two cars for daily commutes, errands, and kids’ activities

One vehicle will be used for daily commuting only. The other will be used for daily commuting PLUS errands, kids’ activities, weekend events, and getaways.

- Mileage:

- Vehicle 1: 10,000 km/year

- Vehicle 2: 15,000 km/year

- Insurance cost:

- Vehicle 1: $2,100/year

- Vehicle 2: $2,100/year

- Gas cost:

- Vehicle 1: $1,350/year

- Vehicle 2: $2,025/year

- Oil changes:

- Vehicle 1: $125 x 1/year = $125/year

- Vehicle 2: $125 x 2/year = $250/year

- Major servicing, repairs, other maintenance:

- Vehicle 1: $400/year

- Vehicle 2: $600/year

- Sub-totals:

- Vehicle 1: $2,100 + $1,350 + $125 + $400 = $3,975

- Vehicle 2: $2,100 + $2,025 + $250 + $600 = $4,975

- TOTAL: $3,975 + $4,975 = $8,950

Comparison

Let’s put the numbers together and compare the costs:

| Scenario 1 | Scenario 2 | Scenario 3 |

| $4,975 | $7,398 | $8,950 |

Average savings: $1,552/year

One-car families save an average of $3,975 per year in vehicle costs compared to families with two cars and two working parents. (They’d also be able to save and invest the amount they would’ve used to purchase the second car. This could be a significant amount.)

Families with two cars but only one commute would still save a significant amount: $1,552 per year.

4. Income taxes

The spouse or common-law partner amount is a non-refundable tax credit available to Canadians. If the stay-at-home spouse doesn’t earn income, the working spouse can claim the entire credit. However, any income the stay-at-home spouse earns lowers the credit by the same amount.

For example, the full federal spouse or common-law partner amount is $11,809 for 2019. If the stay-at-home spouse earns $1,000, the credit is lowered to $10,809. (Note that there’s also a provincial spouse or common-law partner amount.)

That means: the less the lower-income spouse earns, the more credit the higher-income spouse can claim. Let’s take a look at how income earned by a stay-at-home spouse can affect a higher-income spouse’s taxes:

Assumptions:

- One spouse earns $80,000/year. Second spouse earns $60,000/year.

- To keep things clear, we’ll only look at the tax savings in this section. The $60,000 earned by the stay-at-home spouse is not included. (Earned income from the stay-at-home spouse will be accounted for in Part 3 below.)

- All values below calculated for BC tax rates using the Tax Tips Canadian Income Tax Calculator.

Scenario 1: One spouse earns $80,000; second spouse earns no income

- $80,000 in taxable income.

- Full $11,809 spouse or common-law partner amount available to claim.

- $16,938 (16.68%) in taxes owing.

Scenario 2: One spouse earns $80,000; second spouse earns $60,000 in income

- $80,000 + $60,000 in taxable income.

- None of the $11,809 spouse or common-law partner amount available to claim.

- $19,211 (19.52%) in taxes owing for spouse who earns $80,000 in income.

| Scenario 1 | Scenario 2 | |

| Total taxes paid by spouse who earns $80,000 in income | $16,938 | $19,211 (+$2,273 vs SAHS earning no income) |

Average savings: $2,273/year

By earning no income, the second spouse lowers the working spouse’s tax bill by $2,273/year.

5. Investment fees

When both parents work, there’s little time to think about investments. (This was the case when my husband and I both worked full time.) A full-time stay-at-home parent could take on management of the household investments, or free up time for the working spouse to do so.

By DIY investing in low-cost index ETFs, this family could save 1%+ in financial advisor fees and another 1%+ in MERs. Plus, as the nest egg grows, the savings continue to increase:

| Nest egg size | Investment fee savings |

| $300,000 | $6,000 |

| $500,000 | $10,000 |

| $1,000,000 | $20,000 |

There’s also another component to factor in—the growth from keeping that 2% invested instead of going to fees. Just in the first year, this is the growth that could be generated (based on an average 7% return from index investing):

| Nest egg size | Investment fee savings | Annual growth of fee savings | Total |

| $300,000 | $6,000 | $420 | $6,240 |

| $500,000 | $10,000 | $700 | $10,700 |

| $1,000,000 | $20,000 | $1,400 | $21,400 |

Average savings: $6,240/year

Based on a $300,000 portfolio, $6,240 per year could be saved if the stay-at-home spouse manages the family’s investments.

6. Recurring expenses

Optimizing recurring expenses is one of the easiest ways to save a lot of money. When both parents work, it can be challenging to find the time, energy, and motivation to take on this task.

Fortunately, the ‘work’ of optimizing expenses can be broken up into short segments of time. This makes it possible for the stay-at-home parent to squeeze the following tasks into nap times or other quiet times during the day:

- Calling around for quotes.

- Switching providers.

- Negotiating better rates with existing providers.

- Researching better, cheaper options.

- Taking time to consider which expenses could be cut out.

Listed below are some of the larger expenses that I’ve been able to optimize:

| Expense | Old cost per year | New cost per year | Savings per year |

| Life insurance (took the time to better-optimize our coverage) | $2,650 | $455 | $2,195 |

| Home insurance (switched to get better coverage and a lower rate) | $1,800 | $910 | $890 |

| Car insurance (took the time to better-optimize our coverage) | $2,100 x 2 cars = $4,200 | $1,800 x 2 cars = $3,600 | $600 |

| Landline + internet (switched to VoIP calling and wholesale ISP) | $1,260 | $616 | $644 |

| Property taxes (saved up the monthly instalments in a HISA instead of letting the city hold it, and also paid for the bill using a credit card and Paytm) | $19 saved(interest paid by the city for my monthly instalments that they hold through the year) | $169 saved (interest from EQ Bank for my monthly savings towards the property tax payment + credit card cashback on payment through Paytm) | $150 |

| TOTAL: | $4,479 |

Average savings: $4,479/year

Optimizing expenses saves us $4,479 per year. That’s pretty significant, especially when you consider that I only needed to lower each expense once—then it’s done!

With no further effort, we’ll continue saving from that point on. (But I recommend you revisit your recurring expenses every 1-2 years.)

7. Credit card rewards

It doesn’t take a lot of time or effort to better-optimize your credit cards. But it does require some focused time. In a dual-income household, it’s not always easy to find the time for ‘optional’ tasks like this.

Having one stay-at-home spouse helps to free up both partners so that one is able to take on tasks like this. Doing so can earn most families over $1,000 per year in credit card rewards.

(I use a simple, low-maintenance system to manage our credit card rewards. You can read more about it here.)

Average savings: $1,000/year

8. Discretionary spending

When my husband and I both worked, we were usually too busy to deal with things like watching for deals or researching purchases. Most often, we’d have to choose convenience over savings.

Being at-home full time, I’m better-able to optimize our spending. Additionally, I have time to follow up with manufacturers when products break or perform badly. This usually results in free product replacements or generous coupons and vouchers.

Here are some recent examples of ways I’ve saved on our discretionary spending:

| Expense | Regular price | Sale price | Savings per year |

| Flights to Japan | $900/person x 4 = $3,600 | $731/person x 4 = $2,924 | $676 |

| Kids’ clothing | $450/yr (at 10% off regular price of $500/yr) | $250/yr (at 50% off regular price of $500/yr) | $200 |

| Following up with manufacturers | $150 (broken door handle) + $50 (prematurely spoiled food that had to be discarded) | $200 in free replacement products, coupons, or vouchers | $200 |

| TOTAL: | $1,076 |

Average savings: $1,076/year

9. Clothing

When I worked outside the home, I had to buy dressier and pricier clothes and more pieces of clothing than I need as a stay-at-home mom. Let’s take a look at how much can be saved when a professional wardrobe is no longer needed:

Scenario 1: Stay-at-home parent wardrobe

As a stay-at-home mom, I can get away with wearing a few items over and over. So I only need 2 new tops per year and 2 new bottoms. I also don’t need dressy or high-quality clothes, so the average cost per piece is only around $20. That totals $80/year.

Scenario 2: Working parent wardrobe

When I was working, I used to buy around 10 new tops and 4 new bottoms per year. (It’s still not socially-acceptable to wear the same outfits too often. That meant I needed to keep a larger inventory of clothing for work.) At an average cost of $60/piece, that totals $840/year.

I’d also still need to buy some non-work clothes (probably only half of what I’d need as a stay-at-home mom.) That would be $40/year in non-work clothing.

So as a working parent, I’d spend a total of $880/year in clothing.

| Stay-at-home parent wardrobe | Working parent wardrobe |

| $80/yr | $880/yr |

Average savings: $800/year

Total financial benefits

Let’s take all the savings listed above and tally them up:

| Expense | Savings realized with one stay-at-home parent |

| Childcare | $12,818 |

| Food expenses | $12,360 |

| Vehicle expenses | $3,975 |

| Income taxes | $2,273 |

| Investment fees | $6,240 |

| Recurring expenses | $4,479 |

| Credit card rewards | $1,000 |

| Discretionary spending | $1,076 |

| Work clothing | $800 |

| TOTAL: | $45,021 |

Average total savings: $45,021

Based on the average assumptions I used for each category, a family of four could save an average of $45,021/year with one parent at-home full-time.

Note: In order to earn an after-tax income of $45,021, the second parent would need to earn a salary of $58,150 per year. This is the minimum salary required for it to make sense for the second parent to work full time.

Part 2: Lifestyle benefits

The financial benefits of a stay-at-home parent are significant. But I feel the most important benefits are those that improve the family’s quality of life. These are things that tend to be tied to our core values, and are what most would consider to be ‘priceless’.

Here are seven ways my family has benefitted from having one parent at-home full-time:

1. Decreased stress

With a full-time stay-at-home parent, the entire family feels less stressed. Here’s how:

- Fewer transitions: Transitions are hard on everyone (especially young children). With one less work commute and no childcare commute, there are far fewer transitions for everyone each day.

- Time freedom: With only one work schedule and no childcare schedule to plan for, the family gains a lot of time freedom.

- Slower lifestyle: With fewer transitions and more time freedom, the family can choose a slower lifestyle.

- More energy: A slower lifestyle leaves everyone with more energy.

- More productive: With more energy, both parents are able to get more done and not constantly feel behind on life.

- Overall decreased stress: This entire chain of events leads to an overall less-stressful lifestyle for the entire family.

2. Worry-free days off

I’ve seen the stress that unexpected or frequent days off creates for working parents. It’s not easy juggling work and kids’ schedules! With a full-time stay-at-home parent, there’s always someone there to cover:

- Sick days.

- School professional development days.

- Early dismissals.

- School holidays.

- Snow days.

My husband can go to work worry-free even if one or both of our kids are sick. And if my kids get injured or sick while at school, I can drop everything to bring them home. This would all be a lot more stressful to arrange if both of us worked full time.

3. One parent is always there

For me, this was the biggest reason why I chose to be a stay-at-home mom. It was so important to me that either my husband or I be there for as much of our kids’ lives as possible. This is a privilege that we were willing to trade just about anything for.

While the most wonderful childcare providers (including loving grandparents) come very close to replicating the care a parent would provide, it’s not the same.

Each of us as parents have our own unique values we’d like to pass on to our kids. These values are taught in all the little moments that make up the days, months, and years of our lives. It’s such a gift when at least one partner can be there to teach and connect with their children in all these little moments.

4. Never miss out

Some of my most vivid childhood memories are of missing my mom when she went back to work full-time. (She stayed home with my twin sister and I until we started kindergarten, but out of necessity, returned to her job to help provide for our family.)

I remember the envy I felt towards other kids who had stay-at-home parents. Their parents could join us for field trips, Girl Guide outings, and sports days. These memories, while sad, motivated me to find every way possible to be at-home full-time with my kids.

I can’t put a value on how wonderful it’s been (for me and my kids) to have witnessed every milestone and special event in my children’s lives. And in doing so, I’ve also been able to include my husband by recording the events in photos and videos or retelling the event to him.

Importantly, it’s not even the big events that mean the most to me. Being there for the fleeting moments of silliness, sadness, anger, joy, messiness, craziness—all of it—is something I’d give up any material possession for.

5. More involvement at school

This is one area that has hugely benefited my kids. Volunteering at my kids’ school has benefited them (and us) socially and academically.

Social benefits

As a family, we’ve benefited from the strong connections we have at the school and in the community. Volunteering has allowed me to better connect with various members of the school community:

- Teachers and school staff: Since I’m physically present more often, I’m better-able to get to know the teachers and school staff. This makes it easier for us to communicate, which leads to better problem-solving should my kids need help. It also strengthens our relationships at the school and helps me stay on top of the latest happenings.

- Classmates: Being around the school also allows me to get to know my kids’ classmates and friends. This helps my kids socially by allowing me to figure out who would be the most-suitable friends. It also benefits our family socially since I grow to care for these children—further deepening our family’s connection to the community.

- Oher parents: Volunteering with other parents has created many new friendships. As a side benefit, this helps to build a network of parents that all our kids can be comfortable with and supported by.

Educational benefits

By offering my time at school, I not only benefit my kids, but all students at our school. Thanks to parent volunteers, our school has benefitted from:

- Better-equipped classrooms.

- A strong music program.

- A well-stocked and well-staffed library.

- Extra in-school and after-school programming.

- Playground upgrades.

- Reduced field trip costs.

6. More involvement at home

The after-school hours are some of the most important to me as a stay-at-home parent. While my kids aren’t the most pleasant to be with at this time of day (they’re usually hangry and tired!) it’s when I do a lot of connecting with them.

It’s the best time for me to:

- Listen and support: On the walk home from school, I hear about the problems and triumphs of the day, and help to coach my kids through their challenges. Usually, by the time my husband gets home, everyone has fully divulged their issues, and is ready to enjoy a quiet, relaxed evening together.

- Make a nutritious snack: Since I’m home in the after-school hours, I have time to make a nutritious snack for my kids. This saves money and is more healthy than buying packaged snacks.

- Help with homework: Between 3–5 pm, I try to help my kids get as much of their homework done as possible. Usually, most of it’s done before dinnertime, so it frees us as a family to enjoy our evenings.

- Cook a home-cooked dinner: Nearly every night, I have the time and energy to prepare a fresh, home-cooked family meal. We sit down to eat together, which provides yet another opportunity for our kids to connect with us and tell us about their day. (Additionally, regular sit-down family dinners have consistently been shown to be an important factor in children’s happiness and academic success.)

7. Easier scheduling/more time freedom

When my husband and I both worked, appointments and chores had to be scheduled for evenings and weekends. This often left us with little time to relax and just enjoy our off-hours.

As a stay-at-home parent, I have a lot more time freedom. This means when the kids are at school, I’m able to schedule:

- My medical and dental appointments;

- Meetings and appointments with repair people and other service providers;

- Haircuts;

- Car maintenance;

- Menu planning;

- Food prep;

- Financial tasks;

- Chores;

- Errands.

Additionally, kids’ activities and appointments can be scheduled for after school, school days-off, or school breaks:

- Playdates;

- Parent-teacher meetings;

- Kids’ medical and dental appointments;

- Kids’ activities and sports.

As a result, most of our evenings and weekends are luxuriously slow-paced. This gives all of us time to relax, spend time together, and enjoy the freedom of having nothing to do!

I’m so grateful that we have the option to choose this kind of lifestyle. The gift of time freedom pays off in so many incalculable ways:

- Less stress and anxiety (from less rushing around and having more time to just relax).

- Better relationships (due to more quality time together).

- Increased confidence and happiness (from having the time to learn and master new skills and hobbies).

- More creativity (from having to figure out what to do because every hour isn’t fully planned and booked).

- Less grumpiness and arguing (because everyone can get to bed on time and sleep in most weekends).

8. Career benefits for the working parent

One final benefit that can’t be overlooked is the benefits to the working parent’s career. All the above lifestyle benefits lead to:

- The working parent having a clearer mind and more flexible schedule.

- Better focus at work and the ability to work harder and more efficiently.

- Being able to provide the employer with more value.

- Greater opportunities for promotions.

- More income for the whole family.

I look at it like this: with both partners funneling all their effort into supporting one person’s career (instead each focusing on their own career) it’s possible that the resulting gains in income could make up for (or even exceed) the lost income of the stay-at-home parent.

Summary: Lifestyle benefits

There are many lifestyle benefits of having a stay-at-home parent. These benefits improve the entire family’s mental, emotional, and physical health.

While it’s not possible to quantify how much these benefits are worth, I do know this: happiness increases, stress decreases, and life gets a lot simpler and slower. For us and some families, that’s worth the trade-off of a second income.

Additionally, these unquantifiable benefits can lead to the quantifiable result of more income for the family. The stay-at-home parent is able to make the working parent’s life outside of work easier. This allows the working parent to better focus on and advance in their career. This could make up for or exceed the lost income of the stay-at-home parent.

Part 3: Opportunity cost

We can’t discuss the true cost of a stay-at-home parent without also considering the opportunity costs. Lost wages and benefits can be a substantial factor and can’t be overlooked.

In this section, I’ll detail what a family could stand to lose when giving up one parent’s income.

1. Earned income

The average salary in BC for 2017 was $49,244. This seems a bit low to me, so instead, I’ll base this section on what I would have earned had I continued working.

When I left the workforce in 2005, my annual salary was $48,000. Based on the inflation calculator from the Bank of Canada, my salary would have increased to $60,000 in 2019. (At the non-profit I worked at, there wouldn’t have been opportunity for promotions. Any pay increases merely kept up with inflation.)

However, earned income can’t be calculated for one spouse in isolation. Because of the spouse or common-law partner amount, earned income must be calculated for the couple.

So, based on one spouse earning $80,000 and the second spouse earning $60,000, here’s how the earned income would add up (assuming no RRSP contributions or other tax deductions):

| One spouse earns $80,000; the other earns no income | One spouse earns $80,000; the other earns $60,000 |

| Total net income of $62,982 | Total net income of $60,708 + $46,348 = $107,056 |

Opportunity cost: $44,074/year

2. Extended health benefits

For some families, the lower-income spouse has the superior (or only) benefits package. Losing these benefits means the family would need to pay out-of-pocket for expenses such as:

| Expense | Out-of-pocket cost |

| Dental exams x 2 adults x 2/year | $375 x 2 x 2 = $1,500 |

| Dental exams x 2 kids x 2/year | $180 x 2 x 2 = $720 |

| Prescription medications for the family | $1,300/year (based on our spending) |

| Eyewear for one child | $400 every two years (average of $200/year) |

| TOTAL: | $3,720/year |

Opportunity cost: $3,720/year

3. Company-provided retirement benefits

My non-profit didn’t offer any retirement benefits, so I didn’t lose anything in this area. However, many companies do offer an RRSP contribution match. Based on this Reddit thread, typical RRSP matching in Canada is 100% match, up to 5% of your salary.

On my hypothetical 2019 salary of $60,000, I could have earned $3,000 in matched RRSP contributions for 2019.

Opportunity cost: $3,000/year

4. Government-provided retirement benefits

Stay-at-home parents lose out on CPP (Canada Pension Plan) benefits since it’s based on earned income. Based on my hypothetical salary entered into the CPP calculator I would’ve received $8,000 per year in CPP benefits had I continued working.

Opportunity cost: $8,000/year

5. Perks and discounts

This is a hard one to calculate since there’s such a wide range of perks and discounts that companies can offer. At my job, I had access to things like:

- Free or discounted event tickets.

- Group discounts on services and products.

- Free parking (even when I wasn’t working).

- Occasional free food or swag.

These perks and discounts could’ve saved us around $200 per year.

Opportunity cost: $200/year

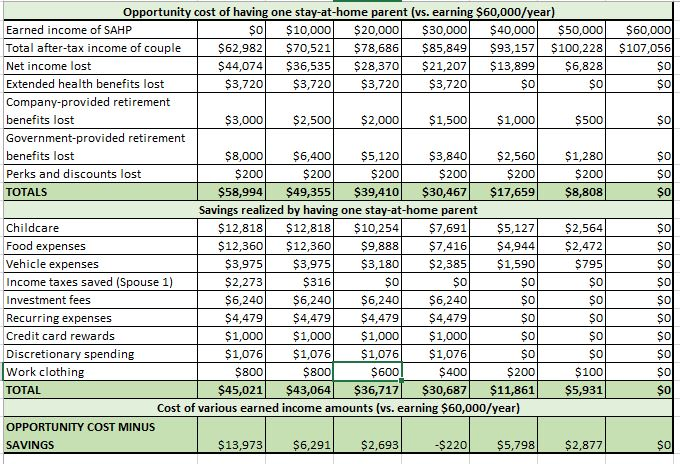

Total opportunity cost

Let’s take all the lost income listed above and tally up the opportunity cost:

| Expense | Opportunity cost of one stay-at-home parent |

| Earned income | $44,074 |

| Extended health benefits | $3,720 |

| Company-provided retirement benefits | $3,000 |

| Government-provided retirement benefits | $8,000 |

| Perks and discounts | $200 |

| TOTAL: | $58,994 |

Part 4: The final cost of one full-time stay-at-home potent

Based on the math I’ve presented above, this is the final cost of one full-time stay-at-home parent:

| Savings realized by having one parent at-home | Opportunity cost of having one parent at-home | Difference |

| $45,021/yr | $58,994/yr | $13,973/yr |

Final cost of a full-time stay-at-home parent: -$13,973/year

Based on the average assumptions I’ve used in this article, a 4-person family living in the Vancouver area would lose $13,973 in income per year if one parent stayed at home full time. (Assuming a $60,000 salary if the stay-at-home parent were to work instead.)

Part 5: Part-time work (something to consider)

Throughout the article, I’ve compared the cost of a full-time stay-at-home parent to a full-time working parent. But there’s another option that could trump both those options: part-time work.

Part-time income allows the family to meet their financial needs while still maintaining a less-stressful lifestyle.

Let’s do the math to see how part-time income affects the finances of our hypothetical family.

Assumptions:

- One parent earns $80,000 per year.

- The second parent’s potential full-time earnings are $60,000/year.

- The part-time income comparisons in this section are all calculated against the above scenario ($80,000 + $60,000 dual-income household).

Additional assumptions:

At $10,000 of part-time income:

- The stay-at-home parent can rely on their partner to cover them for their few hours of work each week.

- No childcare is needed.

- The higher income spouse loses most of the spouse or common-law partner credit.

- All other savings remain the same because the stay-at-home parent still has the time to optimize the family’s finances.

At $20,000 of part-time income:

- The stay-at-home parent works one to two days a week.

- Some childcare is needed.

- The family eats out a little more.

- Vehicle costs increase a bit.

- Work wardrobe costs increase a bit.

- The higher income spouse loses all the spouse or common-law partner credit.

- All other savings remain the same because the stay-at-home parent still has the time to optimize the family’s finances.

At $30,000 of part-time income:

- The stay-at-home parent works two to three days a week.

- More childcare is needed.

- The family eats out a little more.

- Vehicle costs increase.

- Work wardrobe costs increase.

- The higher income spouse loses all the spouse or common-law partner credit.

- All other savings remain the same because the stay-at-home parent still has the time to optimize the family’s finances.

At $40,000 of part-time income:

- The stay-at-home parent works three to four days a week.

- They now have access to company-sponsored extended health benefits.

- More childcare is needed.

- The family eats out more.

- Vehicle costs increase.

- Work wardrobe costs increase.

- The higher income spouse loses all the spouse or common-law partner credit.

- The stay-at-home parent no longer has the time to fully optimize the family’s finances, so those savings are now lost.

At $50,000 of part-time income:

- The stay-at-home parent works four to five days a week.

- They now have access to company-sponsored extended health benefits.

- More childcare is needed.

- The family eats out more.

- Vehicle costs increase.

- Work wardrobe costs increase.

- The higher income spouse loses all the spouse or common-law partner credit.

- The stay-at-home parent no longer has the time to fully optimize the family’s finances, so those savings are now lost.

Spreadsheet used to calculate the numbers (you can download it here in case you want to change the numbers)

Note: Values in line 3 ‘Total after-tax income of couple’ were calculated using the assumptions listed above and Tax Tips Canadian Income Tax Calculator.

Comparison

| Spouse 1 earnings | Spouse 2 earnings | Cost to the family vs Spouse 2 earning $60,000/yr |

| $80,000 | $0 | -$13,973 |

| $80,000 | $10,000 | -$6,291 |

| $80,000 | $20,000 | -$2,693 |

| $80,000 | $30,000 | +$220 |

| $80,000 | $40,000 | -$5,798 |

| $80,000 | $50,000 | -$2,877 |

Based on this comparison, the smallest loss in income (versus earning $60,000 from a full-time job) is at $30,000 of part-time income. In that scenario, a part-time stay-at-home parent actually adds $220 per year to the family’s income!

Interestingly, at $40,000 of part-time income, the cost to the family actually increases. This is the case because the second parent no longer has the time to fully optimize the family’s finances. In addition, the costs associated with going back to work increase.

Also of interest: at $40,000 of part-time income, the cost to the family is roughly the same as at $10,000 in part-time income (-$5,798 vs. -$6,291—a difference of $493). Similarly, at $50,000 in part-time income, the cost to the family is roughly the same as at $20,000 in part-time income (a difference of $184).

I have to wonder then—is it worth the longer hours required to earn more than $30,000 in income? It might be if you enjoy your job and prefer that over spending more time optimizing finances at home. But maybe it’s not worth it to you since it means more hours away from your family.

To make this decision, do the math with your own numbers. It will help you see if your earnings, costs, and hours align with what truly matters to your family.

Wrapping things up: How much does it cost to be a stay-at-home parent? -$13,973 per year!

Based on the average assumptions I used for each category, a four-person family living in the Vancouver area could save an average of $45,021 per year with one parent at home full time.

But once we factor in the opportunity cost of lost income and benefits, the same family loses $13,973 per year in income if one parent stayed at home full time. (Assuming a $60,000 salary if the stay-at-home parent were to work full time.)

One important thing to consider is that the second parent would need to make $58,150 per year in order to earn an after-tax income of $45,021. This is the break-even point where the second parent’s earned income matches what they could save as a full-time stay-at-home parent.

But finances aren’t the only factor! We can’t ignore the lifestyle benefits of having a stay-at-home parent. These benefits improve the entire family’s mental, emotional, and physical health.

While they’re unquantifiable, I’d argue that the lifestyle benefits are even more important than the finances. Additionally, these lifestyle benefits could in fact lead to the working parent earning more money for the family.

Finally, there’s one more option that’s worth considering: part-time work. Based on my calculations, if the second parent works part-time earning $30,000 per year, this would be the most financially-optimal scenario for a four-person family.

Shockingly, a family with the second parent making $30,000 per year in part-time income actually nets an extra $220 per year compared to a family where the second parent earns $60,000 per year at a full-time job! On top of all that, the part-time $30,000 earning family would still realize most of the lifestyle benefits of having a stay-at-home parent.

In summary, evaluate what’s most important to you. Do you need the extra income? Or do the lifestyle benefits outweigh the income? If you want the best of both worlds, consider a part-time job—it may be the best solution!

I’d love to hear your thoughts—comment below and tell us:

- Do you and your partner work full time? Why or why not?

- What benefits and challenges have you encountered because of your choice to have (or not have) one parent stay home?

- Have you calculated the cost of your decision? (If so, please share where you live and how much it costs your family.)

Finally, I’ve overlooked anything, please leave a comment below. I’m happy to converse with and learn from you!

Thank you Chrissy for such an insightful article! It has been fun working on this article with you.

One thing that would be useful in your calculation is the cost of the income earning spouse passing away or the unfortunate case of divorce. I’ve seen many families with SAHMs with 3 kids typically, with the spouse suddenly passing away while in their mid to late 40s. It seems more common these days with social dating platforms and apps that the working spouse has an affair or finds love elsewhere and takes their SAH spouse for granted resulting in a divorce.

Skip going back to work and create a rental on your property (convert garage, living space to legal suite), use the rental income to create an income stream and stay home full time. Love your comparisons and numbers. Easy to manipulate for each individual situation. Thank you!!!

One thing you are forgetting is that if the second parent works part time they are paying into CPP which will give them a greater CPP income later. They may also be paying into a pension. For example, I work part time for the feds and I am able to still pay into my pension while doing that.

Very good point Sarah. Thank you for pointing that out.

Marie—this is a fantastic comment. The non-FIRE parents who live near me are exactly like the ones you know! Many of my mom friends are just like this, and spend their days shopping and going for coffee dates. So you’re right that being a SAHP doesn’t necessarily mean cost savings or that one spouse will take on the finances.

You also bring up some extra benefits/downsides for the working spouse which I missed. Those are all valid and true, so thanks for mentioning them.

Finally, I appreciate that you shared your family’s work arrangement. In my eyes, that’s pretty darned ideal! Your family is getting the best of both worlds by working part-time from home. Kudos to both of you for setting up such a great situation to raise your kids in!

I love how ambitious this post is! I am a US suburban mom in the Midwest to three school age kids. I have been at home, full time, part time and have a spouse who has also done all three. Sometimes you need to try a few things to see what works for your family. The SAH I know that regretted not at least working part time were all due to the struggle of having to suddenly find a job on atrophied skills and skinny outdated resumes due to divorce, paying for college or retirement, or high one-time expenses from house repairs or unemployment so the decision is important to think through.

Most of the article is spot on but there’s a few things that are not true in this area. In our area SAHP with small children underfoot do not have more time or energy to research investment fees or insurance deals than a working parent with a lunch break. Non-FIRE minded SAH here eat out and pick up coffee often to treat themselves, impulse shop at Target just to get out of the house, worry about wearing the same frumpy clothing at school pickup daily, and need a second car for errands and activities so the gap in spending is much smaller if comparing non FIRE working and at home spending. The non tangible benefits and drawbacks listed are mostly good but omit the reduced stress the non working parent brings for working parent business trips, jealously of the working parent at the close relationship the non working parent has to attend school activities and be with kids, and peace of mind a second working spouse brings to reduce the pressure on a the only working spouse to accept any request of boss to keep the job, benefits and pay raises or pushback on attending school activities.

Currently we have one full time in office and traveling spouse and one part time work from home spouse and it works great for us. Bonus that two working parents meant the kids stopped complaining that they had to go to school while we stayed home (I think they thought we just watched TV all day). Seeing me working at home on paid work on their days off helped them also accept that their school homework is a part of life in a way that watching me mop floors or do laundry never accomplished.

Overall great job!

Aw, thanks for this comment Kim! We’re happy if the article might help others as they consider this decision. I LOVE that you and your husband have such a family-friendly work arrangement. I hope it becomes the norm one day.

I’ve never heard of “Equally Shared Parenting” and will add it to my list (even though I’m way past the baby years now)!

This is amazing and I’m sending it to my friends with newborn babies 🙂 Thank you for putting this together!

We read the book “Equally Shared Parenting” before having a kid, and it shaped our goal to both be part-time work-from-home parents.

Excellent article! I’m glad to read something with more realistic incomes and expenses. Most of the FIRE blogs are people with very high incomes or living in places with very low costs of living.

I have the luxury of being able to work part time. I could easily argue that if you are a SAHP to kids that are not in school yet that you dont have the time to optimize anything. I can get more done on a lunch hour than I can staying home all day with my child!

Thank you Heather. We wanted to paint a realistic image on the impact of a stay-at-home parent. I think Chrissy did a fabulous job!

Hi Heather—part-time work is really ideal. You’re so fortunate to be able to arrange your work life this way. It’s an option I would’ve happily taken if it was possible in my old position.

LOL about getting more done on a lunch hour… that’s so true! (Even when your kids are tweens or teens!)

Wow, this post is like a novel!! Thanks for crunching the numbers! This reinforces my idea that working part-time is the way to go. Although I still maintained a lot of cooking at home ratio while I was full time with one kid, we did get take out once a week and I was more tired. I feel more creative with my food options right now, but I am still tired.

It is a big sacrifice to be a SAHP to your career, and even possibly to your own identity as a woman- having kids is exhausting and I commend all SAHP (including myself right now, as I happen to be on mat leave but am exhausted haha). I don’t think it’s for everyone. Somehow I can’t seem to channel my energy towards making craft projects for my toddler to do (you know, the 152 toddler activities that you can create to keep them busy).

Echo on your identity comment. Not every woman could be a great housewife. That’s another reason why I decided not to go home to be a SAHM. I feel I am more me while working than just being mom.

So it’s really a personal decision and the best choice would be very different for different people. I just hope everybody enjoys their choices.

Absolutely, May—stay-at-home parenting isn’t the right choice for everyone.

I had a friend who felt so sad whenever she saw a well-dressed woman on her way to work. She’d be standing there in her yoga pants, toddler on her hip, wishing to be back at work.

Some might say she was lucky to have had the option to be a SAHM. But she felt trapped by that role and couldn’t wait to get back to her career—even if it meant more stress for the family.

She’s been back at work for a few years now, and she and her family have never been happier. Your comment definitely speaks the truth for many parents.

Ha ha, every time I need to scroll to the bottom of this post to reply to comments, it does seem to be as long as a novel!

I am nodding my head as I read your comments on parenting, GYM. It really isn’t an easy job wherever you’re a SAHP or a working parent!

I totally agree that being a SAHP isn’t for everyone and that there are other losses we need to account for—not just financial.

Thanks for sharing your insight!

I have struggled whether I should go home to be a stay home mom or not ever since I had kid. More so after two kids. I want to point out while a stay home parent will make the breadwinner less stressed by no need to rush for kids activities and other house errands, it will also makes the breadwinner more stressed as now the financial burden is all on one parent. My husband went through two layoffs in past five years. It’s much less stressful for him than his co-workers who are the only breadwinner, as I can still provide for the family. Especially in metro Vancouver quite a few of them have high mortgage payments.

For us, financially it’s a no brainer we would end much better as a dual-income family. Thanks to Chrissy and Bob for the detailed numbers. Now I can have a concrete number of my financial contributions to my family. LOL. It’s not a small number as I make more than $60K. But I still wanted to quit my job from time to time as it’s really exhausting to work a full-time job and raise two children.

It’s definitely true the living cost is much much higher. For us, the rule is any time if we have two options, one cost more money but less trouble, another one less money but more trouble, we always go with the more money but less trouble option.

One benefit to have both parents working is that the kids have to be more independent as they can not depend on us all the time. Hahaha.

Hi there May—I’m so glad you left this comment from your perspective as part of a dual-income household.

You bring up an excellent point—that the working spouse will have more stress about job or income loss. That’s certainly something that can’t be overlooked. Thank you for pointing that out to us.

It sounds like you and your husband have been very thoughtful about your choice to work vs being at-home. You’re very aware of the consequences of the decision you’re making and have decided on the best scenario for your family. That’s excellent planning! My husband and I definitely weren’t that deliberate in our decision-making!

Thank you for taking the time to leave such an insightful comment. (And for so politely pointing out some of the things we didn’t consider!)

This is probably one of the most well written posts that I’ve seen! I should note that some of your numbers would be high compared to my city. Obviously, Vancouver has a much higher cost-of-living than say Saskatoon, etc. However, the concepts still apply!

I grew up in a one-parent household and have seen the benefits and cons of it. While it was great having my mother home all the time, we’ve felt the crunch of money quite a few times. Personally, I expect my household to be dual income, however, my workplace allows me the luxury of being able to work from home and flexible hours so I can still have the best of both worlds. This could help to mitigate some of these costs. I know of a couple in my workplace, one of whom stays at home in morning until kids go to school but then work till 5 and the other would come into work early but pick kids up after school. This helped to eliminate the daycare costs. Yes, they do pay for summer camps but they saved 10,000 in daycare alone. Obviously, it’ll depend on the workplace.

Thank you very much KQ. Chrissy did a great job. I realized that some numbers might be high in comparison but it still gives you a reasonable overview what the impact might be. When both parents are working, a lot of coordination is needed if you don’t use childcare at all. 🙂

Hi KQ, thank you for your kind words. I’m glad this post has been helpful to you and others. Makes all the time and effort Bob and I put in worth it!

Your comment, like many others here, reflect how much variance there is—not just in Canada vs. the US but also in different provinces and cities. It’s been so interesting to me, and frankly, I’m more than a little perturbed that Vancouver is as expensive as it is! I honestly didn’t think there’d be so much of a difference regionally… but it appears to be so. 🙁

I agree that a flexible work schedule/environment goes a long way once kids come into the picture. I envy couples who have had these options right from the start. We may not have made the same decision had I been able to bend my work schedule to better fit around my life.

Thanks guys for doing a detailed research on this. I think all parents have their preferences on what would be best for their situation but I think it would be ideal for a family is to have one of the parents work from home while the other is a full time stay at home parent. You would still be busy with work but at least you have some of the lifestyle benefits that a full-time stay at home parent would have. You kind of have the best of both worlds, you have earned income with staying at home.

Great job guys with this!!

If work allows one of the parents work from home that’d be totally awesome, or being able to work from home part time would really help too.

You’re right Kris—one parent being able to work from home would be ideal. I have friends in just such a situation and, despite having their two kids in at least four activities each, seem to lead relatively relaxed lives!

I’m my situation, I’ve been able to ‘work’ from home by hosting students. It’s worked out very nicely. We not only earn income using extra space in our house, but we can also write off expenses we’d have to pay for anyway. Also, the whole family can get involved, which is both rewarding and educational. 🙂

ADDENDUM: Eagle-eyed Court from Modern FImily caught an error in the post!

In Scenario 1: Full-time stay-at-home parent, the total for all-day camp for 5-12 years old should be $7,200, NOT $4,800.

This also affects other numbers, but not significantly, so we’ve opted to leave the post as-is.

Thanks for the catch, Court!

Very interesting and thorough article! We are also lucky enough to consider the option of one parent staying at home, but neither of us would be happy to be full-time parents. Being a parent 24/7 is exhausting! So, we currently have gone with part-time + full-time parents route.

Only thing to comment – I would also consider a scenario where the parents had already optimized everything before the baby arrived! That would save around 11K/year right there!

I feel for Mrs. T from time to time. Fortunately both kids are out of the house for 8 hours each week to give Mrs. T a bit of breathing room here and there.

Right, that’s a good scenario to consider. Thanks for pointing it out.

Hi Marii, thanks for your comment. You’re right about full-time parenting being HARD! As much as I’ve loved being there for my kids, I’ve also had my struggles.

Thankfully, we survived and things just get easier with each passing year.

You make such a good point about being optimized before baby arrives. That would make a huge difference since most of those optimizations would just continue into the future, with little or no need to revisit very often.

Thanks Chrissy and Bob for sharing this research. It’s a lot to consider and I’ll be returning to this down the road when I’m closer to starting a family. Also, some of the lifestyle benefits are hard to quantify but I’m glad you included them.

Glad you enjoyed the post Brian.

Thank you so much for your kind words, Brian. Makes it all worth it!

Wow wow wow Chrissy AMAZING job with this!!! I’m so super impressed and thank you now I don’t need to write a post on our decision for Nic to retire early and be a stay at home mom and for me to transition to part time as we approach our FIRE number – I’m just going to refer people to this post!!!! The only figures that stood as as high to me (as an Albertan) are the gas costs (we’re closer to $1.00/L) and car insurance (we’re under $1,000/year/car). But I can’t imagine those would swing the results much really.

The hardest part to explain is the NON financial benefits. How do you put a cost to that AMAZING feeling of being able to witness first hand all your child’s milestones, to be there for field trips, to walk with him home everyday from school, to help with homework everyday, to cook a nutritious meal everyday, to have time to volunteer, and I think most importantly to have time for yourself to feel energized and be the best parent you can be. To me those are invaluable and worth the ~$14k difference. Excellent job!!!!!

Yup, Chrissy did an amazing job writing this up. So glad that she included the non financial benefits. You definitely need to consider these benefits when it comes to determine whether to go back to work or not.

Oh Court, you’re just the best!

I’m stunned that your gas and car insurance are SO much cheaper in Alberta. It’s insane here in Vancouver. Gas has actually topped $1.60 in recent weeks. My next car is DEFINITELY going to be an EV!

And yes to the non-financial benefits. We really can’t put a price on those experiences.

Thank you again and again for your enthusiasm and for sharing this post. <3

This is a very comprehensive article! And as a full-time parent for the past 19 years, I’ve never felt so validated as to have $45k/year attributed to this choice. And I think the savings could be even greater. Many dual-income families I know have a cleaning lady come in every two weeks. And for me, being at home and also enjoying cooking, I have done a lot of things like bake our own bread, make yogurt, make granola cereal, bake desserts, make jam, and much more that would cost 3-5x the price if I bought them at the grocery store. For our family, I have also felt that me being with the kids has allowed my husband to go farther in his career, being able to go on regular business trips or needing to work late. Thank you for all your work on this!

Thank you Kari. A stay at home parent certainly can do a lot of DIY stuff while at home to help reduce the overall cost, as you stated.

Another way to look at the numbers. If you earn $60,000 after-tax, and spend $45,000 in extra costs or foregone savings, you’re really only netting $7.50 per hour of work! That’s well below minimum wage.

I know, it’s crazy to think about that way. 🙁

Yikes! It’s pretty terrible when you look at it like that!

Makes it very clear how important it is to sit down and do the math. (Says the person who took 14 years to do so.)

Hi Kari, I’m not sure why, but I always thought you worked full-time! Never knew you were a SAHM as well.

I’m so impressed with how much food you make at home. WOW. I cook most of our meals, but need to get better at making some of the things that you do. Bread would be nice… we tried making sourdough this summer and failed miserably! I should probably start with an easier bread first.

And you’re so right about our partners being able to travel for work or work longer hours. This is the case for my husband as well, and it makes things so much less stressful for him.

We’re a homeschooling family, with just the youngest left at home in the day with me.

I’ve worked part-time from home for the past 3 years. It was only 10 hours per month, but just this fall has gone to about 40-50 hours per month. Even working part-time I see our expenses climbing – I needed new business casual clothes for bi-weekly meetings downtown. And I can’t keep up with everything I did before. We’re ordering in a bit more, and I haven’t baked in ages.

And that’s why I thought you worked full-time! You sure have a lot of balls in the air… with FOUR kids. I’m impressed.

Thanks also for sharing your anecdotal info. It lines up with my observation of other families who are dual-income… so it looks like our calculations and assumptions weren’t too far off!

Hi from Victoria BC here. Just wanted to say wow what a comprehensive post. Also, the #s are pretty bang on. We have a daycare issue in this province. We were lucky enough to come across at spot at daycare facility (1200/mos) just at the right time when I needed to return to work full time, otherwise, the next possible option was to pay 2400/mos for my child up to 3 years at a group centre. We gave consideration to my not returning to work at that price point. By the way, my LO is still on 2017 wait lists for Sept 2020 spots as we do not have a spot for when she turns 3. I have friends that pay what they make for daycare, in order to keep their jobs. @ 3-5 years, the #s do not drop that much, the average is 1k a month here, and rates go up every year or every half year (5-10% depending on centre). Unable to speak for school aged situation at this time as we’re not there yet.

Thank you Island FI. Yes here in BC there’s a daycare issue for sure. It’s too bad that daycare costs so much money!

Hi Island FI: thank you for sharing your real-world experience.

Daycare costs are no joke, and even worse are the long wait lists. I feel for parents who rely on daycare. It’s a huge line item that’s largely out of our control.

Wow, super impressed with the amount of thought and time you put into this breakdown! I imagine our own cost savings would be a bit lower given that we’ve really been working to optimize many of these areas. My step-kids are already almost grown, but we’re drafting out our own plan for a future kiddo now. Thankfully, by the time we plan to have our child, Adam will already be retired, which will be a huge advantage. If he wasn’t, I’d be curious to do our own savings breakdown in comparison to yours. Great read!

Thank you, Chrissy put a lot of time and thoughts into this article. So very thankful she was able to do that.

Aww, thanks for the kind words Elise.

I’m impressed that you’re already planning for your future kiddo!

Despite being very money-conscious, we didn’t plan things at all! We just had a very good sense that we’d be okay after we had kids… and then we went with it. It sounds so bad and irresponsible when I say it now, but it’s the truth!

Wonderful, detailed post! As a SAHM for 14 years, I can agree with the benefits and balance that being available to my kids brings to our family. I recently had a friend comment that I had made a huge financial and professional sacrifice by leaving the workforce. Did I regret it?

Not at all. I’ve never run the numbers so I truly enjoyed this breakdown. I think it’s been a good trade off for us. Thanks for the insight.

Hi Ana,

Glad this article captured the benefits and trade off for a SAHP. Glad to hear that you do not regret being a SAHP at all.

I’ve also heard similar comments, but like you, I have no regrets. I can always make more money, but I can never experience my kids’ firsts again.

But the part-time work proposition is very appealing… my sister has a pretty ideal situation working three days a week as a teacher. Then she also has all school breaks off with benefits and a pension.

It’s a good balance of work and time with the kids. Not many jobs offer that kind of flexibility.

Thanks for taking the time to comment Ana!

Wow, what a comprehensive post! You covered a lot of ground here! For example, I like that you covered some of the non-financial benefits. Those are hard to put a dollar value on, but they most certainly have a lot of value.

Everyone’s numbers are going to be different of course, but as a stay-at-home dad I can say that having one parent stay home relieves *a lot* of stress on the still-working parent.

Thanks for your kind comments Mr. Tako. I’ve enjoyed following your story as a stay-at-home dad and am happy to hear you can relate to some of what I’ve written!

Yup, the non-financial benefits of a SAHP is very important and definitely something you have to consider!

Totally agree that everyone’s numbers are going to be slightly different.

Wow – this is a great article!! As someone who lives in the Vancouver area, and preciously a two income household, having utilized a nanny, daycare and before/after school programs, this is an excellent reflection of the costs we incurred as a family unit.

Now that we’ve reached financial freedom, the reduction in expenses related to work wear, eating out, and just overall not having the time to pay as close attention to our finances is undoubtedly dramatic.

Your article highlights all these aspects and more!! Love seeing the numbers laid out like that! Cudo’s to you both for putting in the effort to put together such an incredibly informative post.

For everyone I know who is contemplating the decision of staying at home or going back to work – I will absolutely be referring them to this post so they can make their decision fully informed on all of the pros and cons of each avenue!

Thanks for sharing your own experience Phia. It’s important for us to see feedback like Joe’s above and yours too.

It helps everyone to understand where the differences in spending might come in.

Based on your comment and what I’ve seen first-hand with friends and family who are dual-income households, I still think the numbers are pretty fair and realistic… for the average large Canadian city!

I’d love for more American readers to chime in and share their thoughts!

Thank you Phia. We wanted to the article to be as thorough as possible. I definitely challenged Chrissy on that. 🙂

Thank you Phia. We wanted to the article to be as thorough as possible. I definitely challenged Chrissy on that. 🙂

This is so good and so thorough. Clearly each experience is going to be different, but the cost to a stay at home parent is much bigger than most people want to think about. Clearly the upsides are also there, but it’s only fair to tackle the question with eyes wide open.

So true Angela. I didn’t have any reference point when I decided to be a SAHM. I may have chosen differently had I seen the numbers laid out like this.

Thanks Angela. Chrissy and I had a lot of back & forth on this article. Glad that we were able to present a thorough analysis.

To me, it looks like the financial savings are wildly inflated. Childcare is expensive, but that’s only for a few years. Once the kids start preschool, it’s much cheaper. After kindergarten, childcare expense is very small. Food saving looks very inflated too. Our food expenses didn’t drop much when I transitioned from working to being a SAHD. All the other stuff too…

Anyway, the biggest benefit for us is a more harmonious family. That’s worth the opportunity cost to me.

Hi Joe,

I don’t think the numbers are inflated, I think they are actually pretty realistic for us Canadians. Maybe it’s a bit different when you’re in the states. Also, the numbers may seem inflated because we are assuming that when both parents are working, they don’t have time to optimize many expenses. For ppl already on the FIRE path and already optimizing, things would look very differently.

Hi Joe,

I don’t think the numbers are inflated, I think they are actually pretty realistic for us Canadians. Maybe it’s a bit different when you’re in the states. Also, the numbers may seem inflated because we are assuming that when both parents are working, they don’t have time to optimize many expenses. For ppl already on the FIRE path and already optimizing, things would look very different.

Hi Joe,

Thanks for the comment and valid criticisms.

TBH, I actually tried my best to make the numbers slightly LESS optimized for the family with the SAHP and MORE optimized for the dual-income household!

I assure you that I used mostly real numbers of my own or from Bob (and when not available, I used numbers from trusted sources). Maybe this just goes to show that life in Canada is more expensive than in the US!

And of course, as Bob said, for families already on the FIRE path, they’ve likely optimized their finances to the point where they’re very similar if not the same. So in those situations, this case study wouldn’t apply.

In the end, your commentary opens up some interesting discussions, so thanks for taking the time to leave your feedback!

And ironically I thought your costs for daycare were too low (and I am in the US). It ignored after school care which can be $100s of dollars a month, it ignored the costs of those random days off. I could use all my vacation days and not even take time off around Xmas/Summer. And that leads me to another point, my daughter has nine weeks off in the summer and two weeks during the winter plus a spring break.

On the other hand, I agree with Joe as our food budget does not drop when I have been unemployed, in addition, my costs for clothes while I work is never that much and for investments, it takes no more work to put your money in fidelity/vanguard vs a high fee advisor. So honestly, I think you inflated the spending of the working couple but ignored some major spending they would actually need.

I couldn’t disagree with you more.

I think that given the complexities of every persons differing situation, spending habits and variance in cost of living by geographic area, this post provides an excellent run down of factors for every parent to consider when making the decision to stay home or return to work.

It mirrors many of the costs I have incurred, and areas where I have saved having been both a working Mom and a SAHM.

Covering every possible scenario, quantity of vacation days, school calendars. Y district, individuals spending approach to wardrobe or eating habits of an individual is an impossibility. I think Chrissy and Bob did an excellent job of making that clear by laying out the assumptions utilized to make the calculations so that people can tweak the numbers to their own individual situation.

That may mean it’s not a direct reflection of your exact situation, but it provides a blueprint from which, with the application of some common sense understanding that no two persons situation is going to be identical, people encountering this decision can easily formulate a cost analysis that includes their unique specifics.

Huge thanks to Bob and Chrissy for investing so much time in putting such a valuable and comprehensive resource together.

I appreciate your feedback, Phia—particularly because you’ve seen the situation from both sides.

I hope others can look beyond the inconsistencies with their own situation and use the article as you’ve suggested—as a blueprint.

Thanks for adding your two cents. It’s good to keep the discussion going!

Hi Ginger, thanks for adding to the discussion.

As hard as I tried to make the numbers fair and realistic, I realize this article won’t fit every scenario. (Too bad I don’t have the skills to turn it into an interactive tool!)

But as Phia points out, the article is meant to be a blueprint that you can refer to and tweak for your own situation.

Hopefully, if you can see it that way, it’ll be of more help to you. Thanks again for the feedback!