As I write this on Oct 12, we just experienced the “worst day” of the stock market since April. The S&P dropped by 2.7%, the NASDAQ dropped by 3.56%, and the TSX dropped by 1.38%. All this was driven by the tariff tension between China and the US – China announced a rare metals export curb while the US announced a new 100% tariff on Chinese imports as retaliation.

Many tech companies rely on rare metals for their devices and products, so the tension caused many big tech stocks to drop.

- Nvidia dropped by 4.91%

- Apple dropped by 3.45%

- Amazon dropped by 4.99%

- Tesla dropped by 5.06%

- Microsoft dropped by 2.19%

- AMD dropped by 7.78%

- Alphabet dropped by 2.05%

- Meta dropped by 3.85%

Since I work for a tech company, its stock didn’t fare well either, dropping by almost 7% on Friday.

Ouch!

It’s not just tech stocks that got hammered, some non-tech stocks didn’t fare well Friday either.

- Canadian Natural Resources was down 4.16%

- BlackRock was down 3%

- Brookfield Asset Management was down 6.43%

- Brookfield Corporation was down 4.48%

I didn’t calculate the exact dollar amount our investment portfolio value dropped by on Friday, but I believe it was roughly between $55-$65k. It’s actually more if you consider my company’s restricted stock units (but these RSUs are not vested yet so I don’t usually count them).

Whichever way you slice it, $55-65k is a lot of money. The thing is, as the value of our investment portfolio gets larger, a few percentage drop means a drop of tens of thousands of dollars. On the other hand, when the market goes up by a few percent, the increase is quite significant too.

That’s why focusing on the actual dollar amount doesn’t mean as much once the portfolio value gets larger. One should focus on the percentage increase or decrease instead. Percentage change makes a great deal more sense than simple dollar amounts.

The fear & greed index went from a neutral score of 53 a week ago to a fear score of 29 on Friday. As a result, many people are freaking out and thinking that worse things are yet to come.

It’s rather funny if you ask me, because it seems that everyone claims to be a long-term investor when the market is up But when the market drops by 3%, then everyone freaks out!

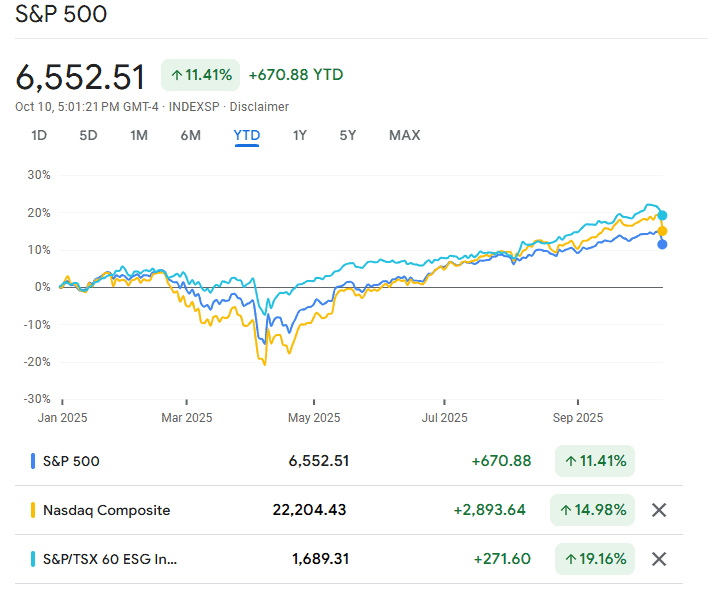

If we zoom out a bit, we’ll see that the market has performed extremely well so far in 2025. In fact, the S&P is up 11.4% YTD, the NASDAQ is up 14.98%, and the TSX is up 19.16%.

The drop on Friday looked like a small little blip on the YTD chart that one shouldn’t even be concerned about.

The reality is, over the long term, we are going to see days like Friday. A 3% drop is pretty insignificant in the grand scheme of things. Over my investing career so far, I have seen much bigger daily drops and we came out on the other side just OK.

Will the market continue to drop over the next few weeks? I have no idea, but I strongly believe that things will work out just fine over the long term – the stock market has a long term historical return of 10% not counting inflation. If you look at our historical yearly portfolio returns, you’ll notice that some years we came out negative but over the long term, our portfolio has returned very well.

| Portfolio return excluding contributions | TSX return | S&P 500 return | |

| 2012 | +8.67% | +4.0% | +13.41% |

| 2013 | +33.04% | +9.55% | +29.6% |

| 2014 | +24.08% | +7.42% | +11.39% |

| 2015 | -5.97% | -11.09% | -0.73% |

| 2016 | +19.62% | +17.51% | +9.54% |

| 2017 | +12.33% | +6.03% | +19.42% |

| 2018 | -2.38% | -11.64% | -6.24% |

| 2019 | +11.32% | +19.13% | +28.88% |

| 2020 | +3.2% | +2.17% | +16.26% |

| 2021 | +32.8% | +21.74% | +26.89% |

| 2022 | -5.4% | -8.66% | -19.44% |

| 2023 | +10.48% | +7.79% | +24.73% |

| 2024 | +30.4% | +17.99% | +23.31% |

| Averages | +13.25% | +6.30% | +13.62% |

What did I do on Friday? At first I was planning to do absolutely nothing. As mentioned before, in the second half of the year, we are usually busy saving for next year’s TFSA contribution. However, Friday was a pay day for me and a quick calculation showed that we should be able to save $14,000 before the end of the year.

So as the stock market continued to go down, I decided to move $1,500 to my non-registered account to purchase some Brookfield Corporation shares. Later in the day, with some dividend residual cash, I then purchased 6.2808 shares of Canadian Natural Resources.

My rationale behind these purchases? I thought it was worthwhile to take advantage of the small market dip by deploying a small amount of dry powder. If the market drops more in the upcoming weeks, we can move more money to buy more and dollar cost average our way down. If the market goes up, that would suit us just fine too (note: if we deploy all $14k saved up for TFSA, that’s OK as well because we could move stocks in-kind from non-registered accounts to TFSAs. If the stocks are down, we can claim capital loss).

It’s important to take a little breather amidst the daily chaos! Step back and look at the market from the high level. Macro trends are always more important than micro trends. Remember this, time in the market is far more important than timing the market!

Tech stocks – more exposure or not

We have held Apple and Alphabet in our dividend portfolio for a very long time. These two stocks have done well for us, giving us multi-bagger paper returns. In our higher risk “play” portfolio, we invest in Amazon, Tesla, and Nvidia. These three stocks are way more volatile than the stocks in our dividend portfolio, but all three have performed well over the years.

A few years ago, we started investing in QQQ/QQQM to increase our exposure in the tech sector (QQQ/QQQM tracks NASDAQ 100 and the NASDAQ is a tech-heavy index). The QQQ/QQQM has performed well, with a five-year return of +104.78% (or just shy of 21% annually).

As we shift more money toward the tech sector, we are seeing a higher alpha (overall return) and a higher beta too (overall risk and volatility).

This begs the question whether this is a smart idea – do we take a higher risk for a potential of higher returns? Or do we need to find the right balance between risk and total return?

For example, we closed out Pepsco and Johnson & Johnson and used that money to buy the likes of Alphabet, Apple, and QQQM. Short term, these moves seemed like a good idea but whether they pay out in the long term remains to be seen.

In September, I mentioned the idea of closing out Proctor & Gamble. I pointed out that PG has been underperforming in 2025 due to slowing consumer demands and tariffs driving up costs, which hurt PG on both fronts (i.e. lower revenues and higher costs). I don’t see the condition improving for PG in the near term. However, does it make sense to close out PG and reinvest the money in say QQQM, Alphabet, or take the riskier approach and invest all the money in Nvidia?

Yes total returns matter and in theory these tech stocks should provide higher returns than PG. But are we willing to stomach the higher beta? Are we able to sleep well at night knowing that we already have over 15% in our dividend portfolio tied to the tech sector through the various stocks and ETFs? (More if you consider my company’s RSUs). Being heavy in one particular sector, I believe, is never a good idea.

As I write this, I will admit that I don’t know the answer and I don’t plan to make that decision in the near term. Throughout my investing career, I have learned that it’s always important to analyze my decisions before making one. I also learned that whenever I make a decision, I want to be able to sleep well at night and not end up second guessing myself afterwards.

These investment decisions are what makes investing interesting and force me to keep on learning!

The danger of leveraging

For the most part, I don’t follow the cryptocurrency market at all. I do get some coverage via X (formerly known as Twitter) whenever some crypto bro’s post shows up on my feed.

Based on what I have seen in the last few days, the cryptocurrency market went down the toilet on Friday too. A quick Google search validated this – Biggest Crypto Liquidation Ever Sees $16B Longs Decimated Amid Market Chaos.

Ouch! Talk about extreme volatility!

No wonder the crypto fear & greed index went from a greed score of 57 down to an extreme fear score of 24.

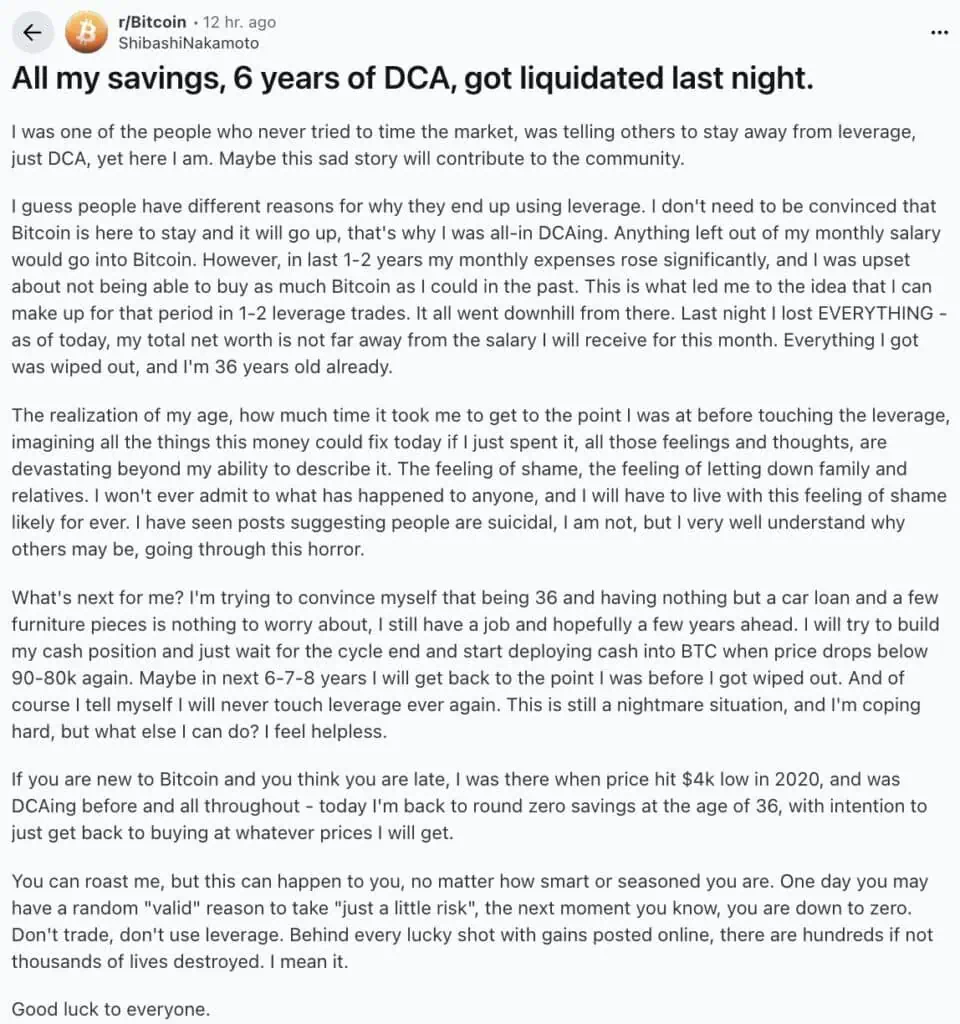

So a lot of crypto investors lost money big time. What shocked me was when I came across this story below:

This 36-year-old investor lost EVERYTHING on Friday and his total net worth is not far away from the salary he will receive for October. Everything he has was wiped out on Friday.

This person claimed that he had been dollar cost averaging Bitcoin for many years. Due to the lower savings rate in the last one to two years, he started using leverage to make up the shortfall. In other words, he borrowed money to invest in Bitcoin. According to the story, this investor was leveraged between one to two times.

Whenever you borrow money to invest, you need to maintain a sufficient cash buffer and a safe collateral buffer in case of a sudden market downturn. If you don’t (i.e. deposit money in your account), your broker will sell some of your holdings automatically to protect themselves.

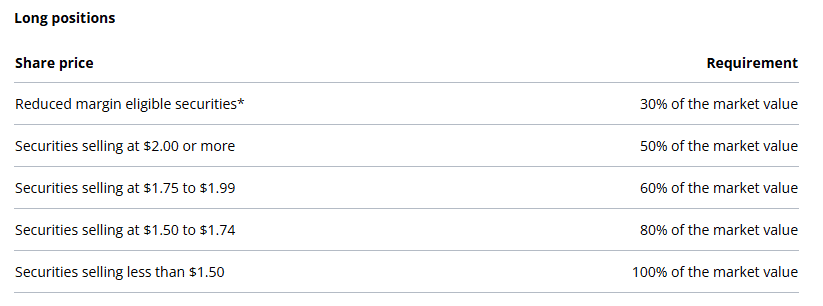

For example, if you trade with Questrade, Questrade sets a margin requirement. The margin requirement is the minimum amount of maintenance excess you must have in your account to enter a position, or a percentage of the current market value.

If you’re trading blue-chip dividend stocks, the margin requirement is 50% of the market value. This means you can borrow up to 50%. If you are trading penny stocks, the margin requirement is significantly higher. In addition to the margin requirement, you also need to consider the interest rates that Questrade charges for lending you money.

On October 10, Bitcoin price opened at $121,704.74, went as low as $104,582.41, and closed at $113,214.37. From opening price to the intra-day low was a drop of over 14% and from opening to closing that was a drop of almost 7%.

Because of the large drop in the Bitcoin price, coupled with the fact that the investor was leveraging one to two times, he didn’t have sufficient cash buffer/collateral buffer in his account. As a result, a margin call was triggered.

Getting a margin call is one of the biggest dangers of borrowing money to invest (i.e. leveraging). When you purchase a stock fully with your own money, you get to decide when to sell. When borrowing money to invest, leveraging, or trading on margin, you have way less control over your investment. You have contractual obligations with the broker. When the asset price drops, you are either required to deposit additional money into your account to meet the maintenance requirements, or forced to sell your assets. If you don’t take these actions, the broker will sell your assets to protect themselves.

Since this story was posted on Reddit, we need to take it with a grain of salt. Based on my quick calculation, a drop of 14% leveraged one time shouldn’t trigger a margin call. Even at 2x leverage, one should still be safe from a margin call. So I believe this investor had more than 2x leverage in his account. Needless to say, this investor was taking on A LOT of risks by going above 2x leverage, not to mention investing in a highly volatile asset like Bitcoin (even 2x leverage was too much in my opinion).

We have never borrowed to invest and don’t plan to do so anytime soon. (i.e. never) I used to invest in leveraged ETFs when I didn’t know what I was doing and I have learned the hard lesson of such a risky maneuver.

My point on this story? When investing, don’t just think about the potential upsides. Do consider the potential downsides. More importantly, think about whether you can live with the potential downside. Invest with money you don’t need for the next five years at least. Don’t invest with money you need in the short term. Whether to leverage or not is a very personal decision. I can’t tell you whether leveraging is a good or bad idea. But I know for us, we will never leverage no matter how enticing the returns are.

Be careful out there!

What a sad story. I never got into crypto as they don’t have any intrinsic value. To each their own. Personally, I did take a HELOC loan but the money is invested in a wide variety of dividend growth stocks, REITs and ETFs across multiple industries. As much as I can, I live by my investing guidelines which is around 5% max in any one company and 20% in any one industry. Leveraging in itself is not bad. Ultimately, taking in more risks that you can realistically handle is what will make or break an investor.

“(note: if we deploy all $14k saved up for TFSA, that’s OK as well because we could move stocks in-kind from non-registered accounts to TFSAs. If the stocks are down, we can claim capital loss).”

I don’t think you can claim a capital loss in this case. I would think it is a superficial loss.

Right, I guess I should have expanded a bit on that idea. If the stocks are down, we’d technically need to sell it in non-registered first to claim capital loss. We can then transfer the money in TFSA then buy back that stock after 30 days. Thanks for pointing this out.

Impressive that you have basically have matched the S & P over the last decade. Curious how you achieved this with stocks such as BCE. AQN, REITS and perhaps many other lower performing stocks? Obviously the tech stocks would make up large gains but if your well diversified its still an impressive feat. From your dividend reports you seem to be heavy in CAN banks/ pipelines and utilities. Again, not easy to achieve well over 10% annual returns. Well done! Any stocks you can mention that stood out as winners?

From above I also own WCN and see it as a very good buy at these levels. Thoughts?

Thanks John, I guess we’ve been somewhat lucky.

The individual stocks are not equal weight so stocks like BCE, AQN, and REITs are all relatively small positions in comparison to the Canadian banks for example. Over the last few years stocks like TD, Apple, Alphabet, Royal Bank, and Costco have done well.

Yes, we’ll probably buy more WCN over the next little while to take advantage of the low price level.

Hi Bob do you still have your WCN stocks – I am losing a lot of money on it. Not sure if I should hold or sell.

Yes we still own WCN, I like the sector overall. WCN is a relatively small position for us.

There has been way too much craziness south of the border and I wanted no part of it so divested all of my XAW index funds in January of this year. I split the sale proceeds between VCN and VIU as well as increased my AA% of bonds in ZAG. With this I have avoided the unpredictable actions of DJT and his economy. VCN and VIU have done exceptionally well YTD (actually much greater than the US) so I am happy with that but wasn’t trying to time the market but rather not be invested in the US for personal reasons and more to Canada and new trading allies.

Interesting that you decided to divest all of your XAW funds. Yup, the TSX has done much better than south of the border this year but we’ll see what happens in the future. The decision makes sense for personal reasons.

I did a little buying on the dip on Friday. I’ve been keeping about 20% of my money BND and BIL just waiting for a market drop. The valuations are quite high now and it helps me feel safer if/when a crash happens.

If the market keeps going up, that’s fine too. I may not make as much money than if I was in 100% stocks, but I can look at the overall dollars (as you mentioned). When I do, I don’t care about a little money left on the table.

Yes valuations are quite high but who knows what will happen. It’s always a good idea to have some cash sitting on the side for deployment. 🙂

Friday I bought VOO, BRK in US acct and VFV in Canada acct. about $20K. I’m praying for end of year drop as usual so hope it goes down. Got to turn my BIL and cash into ETF. Not buying QQQ yet

Should be interesting times ahead.

Hey Bob what’s the for

Ila to calculate portfolio percentage minus dividends ?

Sorry what did you mean?

How do you calculate your percentage average for your portfolio before dividends?

Hi Frank,

Ah I see. I use a very simple calculation -> (N-D-S)/S

N = value now

D = deposit this year

S = value at beginning of the year

So the return would include dividends as well. Hope this helps.

A market correction: FINALLY!

We’ll see if this is a correction or if it’s short lived.

great post.

Thank you!