A few months ago, I questioned whether going all in on QQQ in our RRSPs makes sense. Thanks to engaging readers, the article created some very interesting discussions.

One of the questions that many readers asked was – Why are you investing in QQQ? Why not invest in QQQM instead?

To be completely honest, I was surprised to see this question because I was only aware of QQQ. I didn’t know there was such an ETF called QQQM. After some quick research, I discovered that QQQM is a relatively new product from Invesco whereas QQQ is the long-standing Nasdaq 100 ETF from Invesco.

What are the differences between QQQ and QQQM? Is one better than the other?

Many readers have pointed out that QQQM has a lower MER than QQQ. So that begs the question, does it make sense to switch from QQQ to QQQM to save the expense ratio difference?

I figured this is an interesting question to answer not just for myself but for readers deciding to invest between QQQ and QQQM.

Let’s take a look, shall we?

What is QQQ

Invesco QQQ ETF tracks the Nasdaq 100 Index by holding the 100 largest companies listed on the Nasdaq. The ETF is rebalanced quarterly and reconstituted annually to ensure it tracks the Nasdaq-100 index.

QQQ started in March 1999 so it has been around for over 25 years. That’s quite a long time in the ETF world. At the time of writing, the ETF has $288.01 billion in market value (AUM). QQQ is the 5th largest ETF by AUM (asset under management) in the US, trailing only behind SPY, IVV, VOO, and VTI.

Because QQQ tracks the Nasdaq 100 index, it is very tech heavy. This should be a given for anyone looking to invest in QQQ.

At 0.20% MER, QQQ is relatively inexpensive and comparable to XEQT, VEQT, and other all-in-one ETFs. However, QQQ’s 0.20% MER is more expensive than other index ETFs like VOO (0.03%), SPY (0.0945%), VTI (0.03%), and VCN (0.05%).

What is QQQM

Invesco QQQM ETF also tracks the Nasdaq-100 index and the ETF is rebalanced quarterly and reconstituted annually .(In fact, in terms of holdings and strategy, the two ETFs are virtually identical). At the time of writing it has $31.2 billion in market value (AUM).

QQQM is a relatively new ETF that was started in October 2020. As readers pointed out, at 0.15% MER, QQQM is slightly cheaper than QQQ by 5 basis points.

Comparison: QQQ vs. QQQM

Are there other key differences between QQQ and QQQM other than MER? Why would Invesco have two ETFs that track the same index?

Here’s a quick summary of the key differences between QQQ and QQQM:

| QQQ | QQQM | Comments | |

| Number of holdings | 101 | 103 | Both hold more or less the same amount of stocks |

| Inception Date | Mar 10, 1999 | Oct 13, 2020 | QQQ is over 25 years old; QQQM is younger |

| Expense Ratio (MER) | 0.20% | 0.15% | QQQM is lower by 0.05% |

| Market value | $288.01 billion | 31.2 billion | QQQ is more than 9 times larger than QQQM |

| Dividend Yield | 0.64% | 0.65% | QQQM has a very slight edge |

| 3 Year Performance | +9.50% | +9.88% | QQQM is slightly better (because of the lower MER) |

| 30-day average trading volume | 46,434,632 | 2,379,944 | QQQ has ~19.5 times the trading volume than QQQM |

It shouldn’t be a surprise that QQQ and QQQM are virtually identical. The key differences are the MER, market value, and trading volume. Since QQQ has been in the market for over 25 years, it makes sense that QQQ has a bigger market value (AUM) and a higher average trading volume.

As expected, the top 10 holdings for the two ETFs are the same stocks. Although the percentages are slightly different, I’d say the difference is negligible.

| QQQ | QQQM | |

| AAPL | 9.07% | 9.07% |

| MSFT | 8.15% | 8.14% |

| NVDA | 8.02% | 8.02% |

| AVGO | 5.19% | 5.19% |

| AMZN | 4.82% | 4.82% |

| META | 4.81% | 4.81% |

| TSLA | 2.73% | 2.73% |

| COST | 2.61% | 2.61% |

| GOOGL | 2.50% | 2.51% |

| GOOG | 2.42% | 2.41% |

| Top 10 % | 50.32% | 50.31% |

The top 10 holdings make up more than 50% of both ETFs and the other 91/93 stocks QQQ/QQQM hold constitute a little bit less than 50% of the ETF. The top 10 holdings making up the bulk of the ETF isn’t unusual.

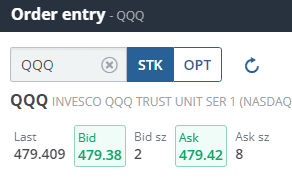

Because QQQ has a higher trading volume, its trading spread, or the difference between the buy (ask) and sell (bid) prices, is much smaller than QQQM.

For example, if I look up QQQ on Questrade when the market is open, the bid and ask spread is between 3 to 4 cents or about 0.008% of the last share price.

Meanwhile, the bid and ask spread for QQQM is about 10 cents or about 0.05% of the last share price.

According to Invesco, the average trading spread for QQQ was 0.00% while the average trading spread for QQQM was 0.02%.

What does the lower bid/ask spread mean? If you trade in and out of the ETF more frequently or if you’re a short term trader, you would prefer the lower trading spread. Since we plan to buy and hold an ETF for a long time, the trading spread shouldn’t make a huge difference.

So why did Invesco launch QQQM in 2020 given the close similarity between QQQ and QQQM? Why didn’t they simply lower QQQ’s expense ratio from 0.20% to 0.15% and call it a day? We’ve seen Vanguard lowering the expense ratio for VXC to match its competitor’s product (i.e. XAW).

I believe it all comes down to money and profitability. Since QQQ is the 5th largest ETF by AUM in the US at $288.01 billion with an average daily trading volume of more than 46 million shares (or about $22 billion), lowering the expense ratio by 0.05% will cost Invesco a lot of money.

How much would it cost Invesco in revenue by lowering the MER by 0.05%?

About $144 million in revenue a year!

That’s a lot of money whichever way you slice it!

By having both QQQ and QQQM, Invesco can attract short term traders (i.e. institutions and more active traders) and long term investors (like you and me). Since big institutions typically prefer trading stocks or ETFs with a very high volume (i.e. better liquidity), they prefer trading QQQ over QQQM and the 0.05% MER difference doesn’t matter as much.

Since individual DIY investors typically don’t buy or sell millions of shares and trade daily, we don’t care as much about trading volume or liquidity. We care more about the total cost of ownership.

Is it worth switching from QQQ to QQQM?

If you’re initiating a new position in the Nasdaq 100 index, I think it’s no brainer to buy QQQM and save yourself 0.05% in MER.

But what happens if you already own QQQ? Does it make sense to switch from QQQ to QQQM and save the 0.05% MER each year?

Let’s run a few different scenarios.

| QQQ (0.20%) | QQQM (0.15%) | Annual difference | |

| $20k | $40 | $30 | $10 |

| $50k | $100 | $75 | $25 |

| $100k | $200 | $150 | $50 |

| $250k | $500 | $375 | $125 |

| $500k | $1,000 | $750 | $250 |

| $1M | $2,000 | $1,500 | $500 |

Over the course of 10, 20, and 30 years (assuming the ETF value stays the same). That’s a difference of…

| Delta after 10 years | Delta after 20 years | Delta after 30 years | |

| $20k | $100 | $200 | $300 |

| $50k | $250 | $500 | $750 |

| $100k | $500 | $1,000 | $1,500 |

| $250k | $1,250 | $2,500 | $3,750 |

| $500k | $2,500 | $5,000 | $7,500 |

| $1M | $5,000 | $10,000 | $15,000 |

As you can see, the difference does add up over time. Let’s not forget that when you invest more money into QQQ/QQQM each year, the difference compounds.

Currently, we hold QQQ in our self-directed spousal RRSP in Questrade and self-directed RRSP in Wealthsimple. Even if we consider the $4.95 commission with Questrade, it makes sense to sell QQQ, pay $4.95, and buy QQQM at no commission (free ETF trading from Questrade).

- You can open an account with Questrade using my referral code and get up to $250 bonus cash.

Note, you only need to hold over $9,900 worth of QQQ to cover the $4.95 commission from the MER difference.

For Wealthsimple, since it’s commission free trading, it is simply to swap out QQQ in favour of QQQM and save the 0.05% MER fee each year.

- You can open an account with Wealthsimple Trade referral code and get a $25 credit bonus. If you become a Generation or Premium client within 30 days you can get $250 or $1,000 bonus rewards.

Even if your discount broker charges higher trading commission fees, for example, $9.99 per trade with TD Direct, if you hold more than 40k of QQQ, it is worth switching from QQQ to QQQM and saving yourself money in the long run.

So where does that leave us?

Well, I think it makes sense for us to switch from QQQ to QQQM and save the 0.05% MER fee every year, especially considering we plan to increase our exposure in the Nasdaq 100 index over the next few years.

So, a few minutes placing selling orders then placing buying orders with the proceeds to save us 0.05% of management fees each year is very much worth the time. (Que )Cue???) the 15 minutes saves you money Geico commercial).

Note: we hold QQQ in our self-directed RRSPs so there’s no capital gains implication if we sell QQQ and swap it for QQQM. If we were to hold QQQ in non-registered accounts, we’d have to take capital gain taxes into consideration.

Summary – QQQ vs QQQM, does it make sense to switch

In summary, I believe both QQQ and QQQM are excellent ETFs to hold. They are very similar ETFs issued by Invesco, tracking the same index, the Nasdaq 100 Index.

The key differences between the two are their AUM, expense ratios, and trading spreads.

Some readers may be concerned about the liquidity but at over 2.3 million shares traded on a 30 day average for QQQM, I don’t think liquidity is a concern for DIY investors.

To summarize, if you plan to trade more frequently, QQQ is a better choice due to the higher trading volume and smaller trading spread. If you plan to hold the ETF for the long term and add more shares regularly, then I believe QQQM is the better choice due to the lower MER fee.

We will plan to switch from QQQ to QQQM. Anyone else?

I checked QQC which trades on the TSX. Its MER is 0.2% (compared to QQQM’s 0.15%)

3 year performance QQC, 12.74% and QQQM, 9.88%. The figures are from my TD Waterhouse account

I assume QQC is not Canadian dollar hedged. There is a CDn hedged ETF QQC.F

I wonder if the performance difference is due to the US/CDN exchange rate

Won’t it better to invest in QQC rather than QQQM?

QQC trades in Canadian dollars so if you don’t want to convert from CAD to USD then yes QQC might be a better choice. I think the performance difference might be due to the currency exchange rate.

Wealthsimple is not a good place for your U.S. Dollar assets. You would lose about 5% on a buy and sell trade? They have very high currency conversion fees. There’s one hidden in the fine print.

You can purchase a lower fee currency conversion ‘package’.

True but that’s not the case when you have the US package. The US package is free once you are premium member.

I have tdb3042 us monthly income mutual fund in my tfsa

Mer is 0.81

Dustrubation (ttm) 5.15%

Whic etf would you recommend

QQQM

VOOG

SCHG

VUG

or any other suggestions

Thanks

Excellent comparison!

I have started moving out of QQQ into QQQM

You’re welcome.

Thanks Tavcan

What would be your thoughts on etfs for Tfsa and RSp ,o have mutual funds that have 0.8 mer want to replace them with etfs

Thank you

Ali

Hi Ali,

I would have no problem holding ETFs in TFSA and RRSP. For tax drags on foreign holdings, you might want to take a look at this – https://tawcan.com/dividend-tax-drags-foreign-withholding-taxes/

Thank you Tawcan

Unless you have diversity in your holdings and have large capital invested, ETFs are not the best choice. This is because generally with ETFs the risks are low BUT at the same time, the returns are low. If you are a small time investor, who’s willing to put in some time researching companies and keeping up with developments, you are best off investing in individual stocks as they can provide a greater rate of return. This is because a ETF holds a large number of stocks, a growth in one stock could get offset by a loss in another so it becomes difficult for you to manage it.

Sorry, not sure if I agree with your statement. 🙂

Excellent review. QQQT is available in CD. I can’t find QQM in $CAN hedged fund. Can you?

Converting CAD to USD very expensive and think volatile with the upcoming political changes

Yes QQQT is another option if you want to trade in CAD. This post is more looking from a USD point of view since we already have money in USD.

I was thinking on the same lines as Walter. The hedged version of QQQ is QQC-f. If the two are compared, the performance is somewhat different. Depending on which side of the exchange rate gamble that is taken, holding US$ investments, while the CDN$ declines, can substantially impact portfolio performance. It’s one more variable I avoid.

Thanks for the feedback. There’s really no perfect answer when it comes to hedging. You’re better off picking a strategy (i.e. hedging or no hedging) and stick with it. Long term I believe there’s not much difference between hedging and non-hedging -https://tawcan.com/hedged-vs-unhedged-etfs-in-canada/

Good analysis and good idea to exchange the two funds.

But the analysis on the very small amount of fees is more interesting in the context of having this investment in your rrsp. The real cost is that with all the capital gains in any rrsp, you are essentially converting capital gains to regular income when you start withdrawing. So the tax rate is double.

So it is good to pay attention to where you keep investments like this one. In the early years it might matter as you only have so much money and have no choice but to put in the rrsp/tfsa but as your wealth grows I would suggest investments with capital gains are better in a non rrsp account.

Hi Dale,

Valid points. Thank you for pointing them out.