Long time readers will know that we hold both individual dividend stocks and index ETFs in our dividend portfolio. We are doing a hybrid investing strategy to capture the best of both worlds – holding individual stocks allows us to dictate which companies we want to hold (usually because we like the long term outlook) and holding index ETFs allows us to geographical and sector diversification. At the end of the day, we care about ‘total return.”

Holding individual dividend stocks requires more research and knowledge, but that’s part of the fun of being a DIY investor.

- How to start investing in dividend paying stocks

- How to start dividend investing with a s little as $1,000

It’s always good to understand the financial numbers of a company that you plan to invest in. One can read through all the annual and quarterly reports, compare the different financial metrics, and even do technical analysis to determine whether it makes sense to invest your money or not.

However, if you start getting into the very nitty and gritty details, it’s very easy to get stuck in the ‘analysis-paralysis’ loop.

Therefore, I believe it’s always important to step back and look at the big picture. Some questions I like to ask include the following:

- Is the company producing products that you or other consumers rely on daily? And will continue to do in the future?

- Is it difficult to replace these products with cheaper equivalents?

- Does the company have fundamental advantages over its competitors?

- Do I believe the company can continue to excuse its core strategy for the next 10 years or more?

- Am I comfortable with holding this stock for at least a decade or more?

While getting into a stock at a good price is important, sometimes investors arbitrarily create a target price without any valid reasons, wouldn’t move from this target, and completely miss investing in a solid company because the share price never hit the target price.

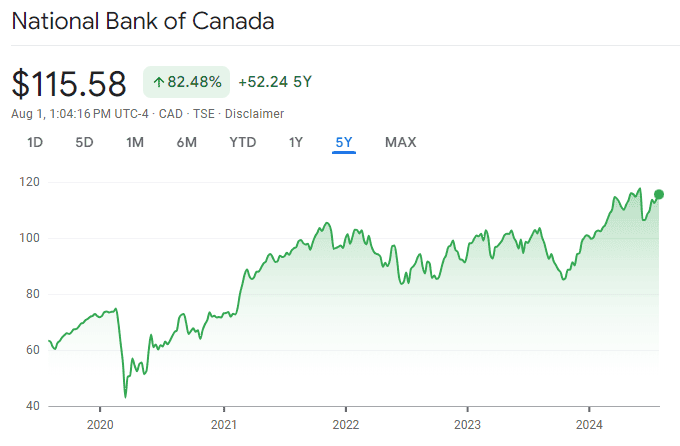

For example, imagine in March 2021 you wanted to initiate a position in National Bank because you missed the opportunity during the COVID-19 pandemic downturn. Due to the historical price during the downturn, you arbitrarily set a target price of $80 and an absolute ceiling price of $85.

You then convinced yourself that no matter what, you wouldn’t buy a single National Bank share unless the price was at $80 or below.

During 2021, National Bank’s share price never fell within your price target so you completely missed the boat on a solid Canadian bank.

Let’s say you continued with the desire to initiate a position in National Bank and kept your $80 price target and $85 ceiling price. Again the share price never fell below $80. It got close a few times during 2022 (~$83), but because you were so set on your target price and refused to pay $3 over your target price, you didn’t initiate a position.

Fast forward to 2024, and you are still waiting on the sideline because the share price never hit below $80 and the share price has climbed to above $110 since.

A missed opportunity because of this arbitrarily set price target?

Yup, I think so.

Again, this is why I think it’s more important for us DYI investors to step back and look at the big picture. Sometimes you may need to ignore the price target. If a company is solid with a great future outlook, you may need to ignore a few dollars of share price difference during your initial entry. After all, you can always dollar cost average in the future.

With that in mind, I thought it’d be interesting to list my five highest conviction positions in our dividend portfolio.

My five highest conviction positions

Please note that everything in this post is purely my personal opinion and is not buying and selling recommendations. Please always make buying and selling decisions on your own after doing your own research..

#1 Apple

I have written a lot about Apple in the past and I continue to like Apple long term. If you look at Apple’s history, it’s easy to point out that the company went through some identity crisis in the ‘90s and early 2000’s. But things have changed since the launch of the iPad and the company has completely transformed around the launch of the iPhone.

Apple is one of the most recognizable brands in the world. Years ago Apple used to be seen as a pure hardware company but it has transformed itself into a services company and perhaps can now be considered as a consumer staples company. The beauty of Apple is the strong ecosystem that Apple has built around its different products. Once you’re in the ecosystem, it gets increasingly difficult to get out of it.

For example, many people I know started their Apple journey with an iPhone. AirPods were next on the shopping list to pair with their phones. They then purchased an Apple Watch for ease of accessibility and AirTags to track their devices. It wouldn’t come as a surprise for these users to have multiple iPads and MacBook laptops too. Before they know it, they are tightly integrated within the Apple ecosystem.

Although we own an iMac at home, we are probably the outliers as the typical Apple users because we don’t own any other Apple products. I do see the attraction for owning iPhones and other Apple products for the tightly integrated ecosystems though (for example, I see the attraction for AirTags but they don’t make sense for Android users).

Apple has never been a company that comes out with a first-to-market product. They always take their time to study the market and launch with a high quality product that’s been perfected. Although some people argue that Vision Pro is a very niche product that not many consumers will purchase, I think it has some unique usage cases and I can see future Vision Pros gaining popularity, just as what happened to Apple Watch.

Therefore, I’m convinced that Apple will continue to do well in the future and have no concern with adding more Apple shares to our portfolio.

#2 Visa

Visa is yet another well-recognized global brand that facilitates electronic fund transfers throughout the world, most commonly through Visa-branded credit cards, debit cards, and prepaid cards.

As one of the largest payment processors in the world, Visa has a nearly impenetrable moat. Yes, Visa does have competitors like MasterCard, AmericanExpress, and even lesser ones like Paypal and new Fintech companies, but Visa is in a well-established position to fend off these competitors.

Because of the wide moat, it is well-positioned for future growth in developing countries. In addition, Visa is a company that doesn’t have to worry about inflation because people will continue to use Visa-branded products regardless of the inflation rate. This is also true whether there’s a recession or a bull market (yes consumers can cut back on their spending but Visa can combat this by increasing transaction fees on merchants).

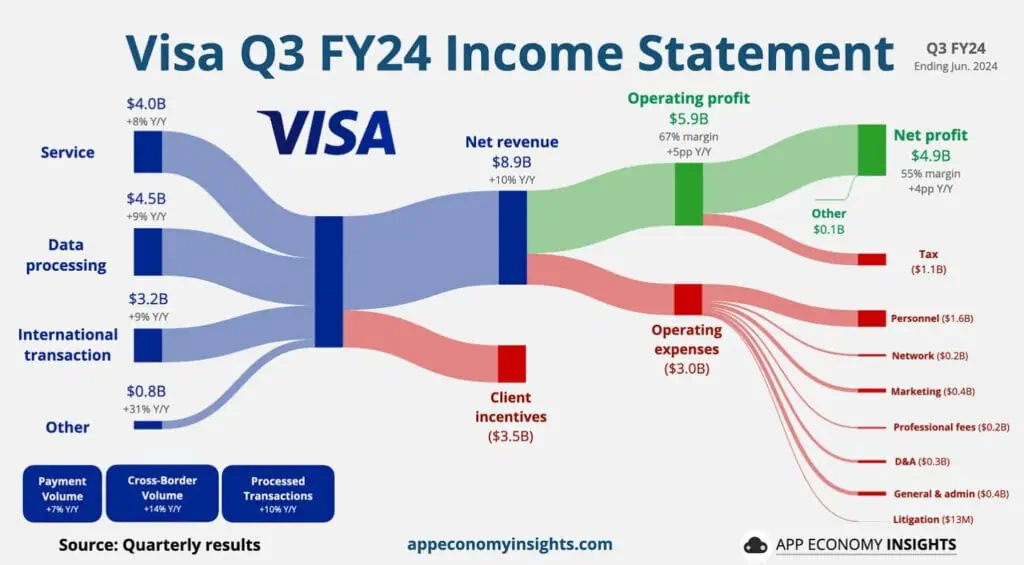

Another thing to consider is how Visa makes money. Visa makes money via different streams:

- When a transaction is completed using a Visa card, the merchant is required to pay an interchange fee

- To access Visa’s electronic payment network, merchants and financial institutions need to pay Visa service fees

- When transactions are processed, Visa charges processing fees.

- When there are international transactions, which is common nowadays, Visa charges international transaction fees

As you can see from the visualized Visa income statement above, we’re talking about billions of dollars from each of these income streams. Visa also enjoys a very high profit margin.

I don’t see Visa going away anytime soon. If anything, I strongly believe the cashless interactions will only increase moving forward and Visa is in a strong position to capture any future growth.

#3 Royal Bank

I can’t have a high conviction position post without mentioning one of the Canadian banks. Royal Bank is the largest bank in Canada by market capitalization serving over 20 million clients with more than 100,000 employees worldwide. Recently Royal Bank completed the acquisition of HSBC Canada to expand its Canadian client base further.

Although many see Royal Bank as a Canadian bank, over the years, the company has been expanding outside of Canada with operations in over 30 countries.

If we disregard all the financial metrics and analyze Royal Bank from a 30,000 foot view, Royal Bank’s large client base is extremely attractive.

Why?

First of all, how many people switch their financial institutions regularly? I can say with conviction that not many people switch financial institutions regularly because it’s extremely painful to do so. Second, how many people you know started banking with a certain financial institution because their parents use the same financial institution? I certainly am one of them – my parents bank with TD so I have a TD account and investment accounts with TD.

Therefore, there are a lot of advantages and benefits Royal Bank has for being the largest Canadian bank with millions of clients. The company will continue to gain clients for many years to come.

#4 National Bank

National Bank isn’t as big as Royal Bank, but I’ve been quite impressed with how well the company operates. Although many investors saw the recent Canadian Western Bank acquisition as a negative, I actually believe the opposite. I think the acquisition is the correct move for National Bank because acquiring Canadian Western Bank will immediately increase National Bank’s footprint in western Canada and increase and diversify the bank’s client base.

Because National Bank is much smaller compared to the Big Five Banks, it should be able to grow faster than these banks via capital markets, wealth management, and acquisitions. Furthermore, mortgages make up a smaller part of National Bank’s revenues, meaning National Bank doesn’t have as high mortgage exposure risk compared to other Canadian banks.

From a high level, I’m convinced that National Bank is a very well run Canadian bank and has further long term growth.

#5 Waste Management & Waste Connections

I decided to group Waste Management and Waste Connections together because they operate in the same sector – garbage disposal.

We humans will continue to generate garbage and someone needs to dispose of these wastes. Both Waste Management and Waste Connections generate most of their revenue from collecting trash and disposing of it. Both companies typically operate by signing long term contracts with customers (i.e. cities, apartment buildings, retailers, etc). Thanks to these long term contacts, the business tends to be quite stable.

Both companies have a large footprint in North America and compete against each other in some regions. However, by investing in both companies, you have them both covered.

I have high conviction in these two companies because of the following key reasons:

- They both can continue to lower their operational cost through technology and automation.

- Can increase collection fees with their customers when negotiating new contracts

- The garbage exposal business is recession proof

- Can generate more revenue by generating biogas from garbage

Who knew the waste disposal business could be so beautiful and lucrative?

#6 Bonus Conviction – Telus

I thought I’d mention an extra position. This one can be a bit controversial given how poorly Telus has done since early 2022.

Why do I have a lot of conviction with Telus?

- Telus, like Rogers and Bell, operate in an oligopoly for the Canadian telecommunication space

- Unlike Rogers and Bell, Telus does not have a media business so that puts Telus on a better footing

- It will take a number of years for Telus to build out its 5G stand-alone networks across Canada and this will take more capital investment. However, I believe Telus is in a good position to capture cellular related revenues moving forward once the 5G network is available across Canada.

- Telus can provide and expand telecommunication related services like security, healthcare, connected devices, etc to generate more revenues. The technology is a lot more resource efficient than 4G LTE so cost per bit is cheaper for operators like Telus.

- Telus CEO Darren Entwistle announced in May that he would forgo his cash salary in favour of shares to demonstrate confidence in the financial health of Telus. You can say this is a bit of an antic but for me, when a CEO does that, it says a lot about the long term strategy of the company.

- Although satellite internet is getting more prominent (i.e. Starlink), I strongly believe most customers will remain with cellular technology. Furthermore, it is not convenient for Internet of Things (IoT) devices to switch to satellite technology due to regulations. Therefore, I do not believe satellite technology will replace Telus cellular based services.

- Finally, Telus, like the other telcos, will continue to benefit from the high immigration to Canada (over one million last year). One of the first things a very high proportion of those new arrivals will need is a phone and a service provider.

With the depressed price and facing a lot of headwinds, it may be prudent to add more Telus shares and wait for the stock price to recover…. You definitely will need to have a lot of patience though.

Summary – My five highest conviction positions

Well, there you have it, my five highest conviction positions with a slightly controversial bonus position included. With the companies mentioned, I have no problem buying more shares and building up solid positions. I strongly believe all of them will continue to grow their dividends and provide solid returns over the long term.

What do you think about my picks? I’d love to hear your opinions.

Very helpful. I own Telus, RBC and Apple. Telus hasn’t been performing well for a while (nor BCE) but I’m hanging onto both. I’m curious what your thoughts are about BCE and if I should in fact hang on.

I’m debating on BCE. Although I don’t like the idea of cutting dividends, I think this is the most prudent thing BCE should do to clean up their books.

Visa is good but not the rest. I suggest amazon, meta, microsoft, alphabet, mastercard, booking holdings, iqvia

OK, we don’t own Meta, Microsoft, MasterCard, Booking Holdings, or IQVIA so not on our list.

Hi, I really appreciate your posts – thank you! I’m wanting to buy more USD but am having a hard time justifying the current exchange rate. Do you still purchase USD even when the exchange rate is so poor? Or do you wait until the currency rate has balanced out? Any suggestions would be appreciated.

Hi James,

You’re welcome. Right now due to the poor exchange rate we probably wouldn’t be exchanging CAD to USD. We’d only purchase stocks if we get USD from dividends.

I feel Telus/telecom industry is having issues with future income is my perception. I was a long time Bell shareholder because of its dividend. I saved $45/month this year while increasing my cell phone plans and home internet speeds. We don’t have USA competition but perhaps they are prepping for the reality. In a pen stroke this “competition” can change similar to Trumps tariffs. I think his tariffs are just the beginning of negotiations and this sector is an easy target. Look at what Ontario just agreed to deal with Elon Musks satellites versus dragging in fiber optic cable to remote areas…. exactly what many provinces are promising more connectivity but at what competitive price?

I’m new to investing, only 2 years in… and I came across your website when researching about XEQT, which is what I am holding the most positions in now. And I wanted to leave a reply about my #1 conviction stock, which is Intel (INTC) I think it will bounce back next year.

Hi Eddie,

Thanks for the comment. I’m not 100% convinced that Intel will bounce back. For technology leadership’s sake I sure hope so.

When I got to your list of questions, I tested it the company that I had the most conviction for ever. That company created the first smartphone. I love it and its app store. No, it wasn’t the fruit company that was first on your list. I’m talking about the Handspring Treo in 2001 that ran the PalmOS with thousands of 3rd party applications.

Handspring was private, but publicly-traded Palm bought them in 2003 – making it possible to invest in the future of mobile information. Of course the rest is history.

Very interesting. 🙂

This is very timely! I’ve been mostly in the S&P 500 with a dash of VYM, but with slow growth on the horizon (would you agree?) and enough VTI, I’m ready to dive into individual stocks. Great call on V and WM—they were already on my radar. I’m locking in V, RY, WM, and adding a wildcard: FLIN.

Long time follower, must be at least 8+ years 🙂

Thank you for being a long time follower, I really appreciate it!

Be aware that a lot of these waste management companies are owned by the mafia. Personally, I don’t want to invest in that, even if the company does look good. To each their own.

Umm ok, what evidence do you have that these waste management companies are owned by the mafia?

I guess you can state that all companies are Mafia run ..What ever that means ? Probbably heard it from a friends friend !!

Mind in providing ticker symbol for waste management? Does it trade on TSX? I know waste connection trades as WCN on TSX. Thanks

Waste Management ticker is WM and trades on NYSE.

I recently bought MICROSOFT CORP CDR CAD HEDGED CIBC DEPOSITARY RECEIPT REG S in an effort to get into the American Tech sector. The dividend isn’t as great as I’d like, since I’m looking for dividends, but I’m an old lady investor, who is trying to be modern re: tech stocks. Would I have been better to buy Apple as per your advice in this article? What is the difference between these two American tech stocks?

Hi Laurie,

I think Microsoft is a very solid tech company too. I wish we have bought MSFT years ago but we picked Apple instead.

Hi, TD has certainly taken a beating, what are your thoughts on TD?

I think TD will be a bit volatile in the short term but long term it will do just fine. Don’t see TD disappear anytime soon. 😉