Over the last few years, I have written posts on our financial independence assumptions and tax consequences when we live off dividends.

- Our financial independence assumptions

- Our financial independence assumptions – what about taxes?

- Revisit our Financial Independence Assumptions

Originally, we thought a dividend income of $40,000 per year would be sufficient. At a 4% dividend yield, this would mean a dividend portfolio valued at around $1 million. To bridge any spending gaps, we would generate income via part-time jobs or sell shares.

But $40,000 is definitely on the lean FIRE for a family of four. We don’t want to just scrape by and have to carefully watch every single penny we spend when we are financially independent.

Furthermore, since my original calculation in 2016, many variables have changed. Although we try to be as frugal as possible, our expenses have increased, mostly due to our kids getting older and having more kids-related expenses.

We also realized that creating memory dividends is extremely important (an important concept from Die with Zero), so we have been “learning” how to be better spenders to create ever-lasting memories.

The result is that we are much more relaxed about spending money on things like family trips. In recent years we visited Maui, New York City, Disneyland, Denmark, Iceland, the Canadian Maritime Provinces, Taiwan, Japan, and Calgary. We also visited various locations close to Vancouver. These trips obviously cost money, but they have created many great memories we will cherish for the rest of our lives.

A few months ago, I provided an update on our financial independence journey and stated we need $60,000 to sustain our current lifestyle. That is a $20,000 or 50% increase from my 2016 projection. This amount doesn’t include RRSP, TFSA, and RESP contributions.

Knowing that we most likely will spend more money on travel and exploring the world when we reach financial independence, I believe $70,000 in dividend income per year should provide us with a sufficient margin of safety.

The plan is not to stop working completely and sit on the beach all day drinking pina colada. We plan to continue to generate income via part time jobs and side businesses. Stepping away from my current full time high tech job will be a big step forward in creating a slower paced lifestyle.

I thought it’d be interesting to determine how much we need to reach financial independence.

How much do we need to reach financial independence?

To answer how much we need to reach financial independence, we will set different annual spending amounts. To simplify the math, I will use 3%, 4% and 3.5% dividend yields/withdrawal rates.

| Annual withdrawal amount | $ Required @ 3% | $ Required @ 3.5% | $ Required @ 4% |

| $50,000 | $1,666,667 | $1,428,572 | $1,250,000 |

| $60,000 | $2,000,000 | $1,714,286 | $1,500,000 |

| $70,000 | $2,333,333 | $2,000,000 | $1,750,000 |

| $80,000 | $2,666,667 | $2,285,715 | $2,000,000 |

| $90,000 | $3,000,000 | $2,571,429 | $2,250,000 |

Based on an annual spending of between $50,000 to $90,000 we will need between $1.25 M to $3M.

That’s a wide range!

Knowing our historical spending and the need for some buffer, I’d focus on the $70k and $80k range with the idea that we’d need between $1.75M to $2.67M. If we take the midpoint of this range, it’d mean we need $2.21M to reach financial independence and live off our portfolio.

The total amount needed will be lower if we supplement the money generated from our portfolio with part time income. What happens if we could generate between $10,000 to $20,000 in part time income each year for about 10 to 15 years? The result would be a reduction in the annual amount needed to between $50,000 to $70,000.

The table again so you don’t need to scroll up:

| Annual withdrawal amount | $ Required @ 3% | $ Required @ 3.5% | $ Required @ 4% |

| $50,000 | $1,666,667 | $1,428,572 | $1,250,000 |

| $60,000 | $2,000,000 | $1,714,286 | $1,500,000 |

| $70,000 | $2,333,333 | $2,000,000 | $1,7500,000 |

We will need between $1.25M to $2.34M to reach financial independence if we plan to generate between $10k to $20k in part time income each year. If we take the midpoint again it’d be $1.795M.

If we take a rough average between $1.795M and $2.21M, we’d get $2M. So aiming to have a portfolio value of $2M or more seems like a good idea.

Interestingly, the $2M number doesn’t align with Cashflows and Portfolios projection of $950k to retire at age 45 ($71.6k spending per year). But that’s somewhat expected given the calculation above is simple and doesn’t take into account these various variables.

Knowing that in 2024 our dividend portfolio generated over $56,000, if we generate part time income for $20k or more a year, we can basically call ourselves financially independent if we really want to.

Given all the layoffs at my company specifically in the last few years and in the high tech sector generally, it is very comforting to know that we have some financial security thanks to hard work since our financial epiphany in 2011.

To summarize:

- If we don’t generate part time income, we need between $1.75M to $2.67M or $2.21M at the midpoint.

- If we generate $10k to $20k part time income each year, we need between $1.25M to $2.34M or $1.795M at the midpoint

Post FIRE simulations

There are many different post-FIRE calculators available on the internet. The best ones are probably the following with each providing some visualization looks on whether your retirement savings can last long enough to support your retirement and spending.

Knowing the numbers above, I thought it would be worthwhile to run some post-FIRE simulations to see the success rates. I decided to run the simulations using FIRECalc and Engaging Data with the following scenarios:

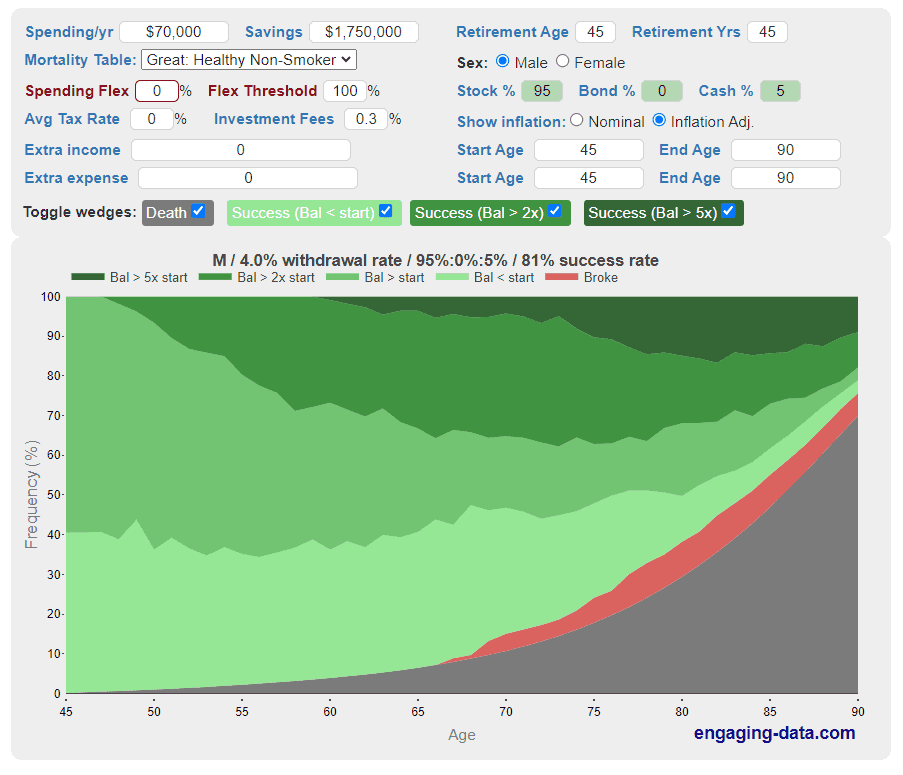

- $70,000 annual spending with a portfolio value of $1.75M. No extra income. 45 years of retirement

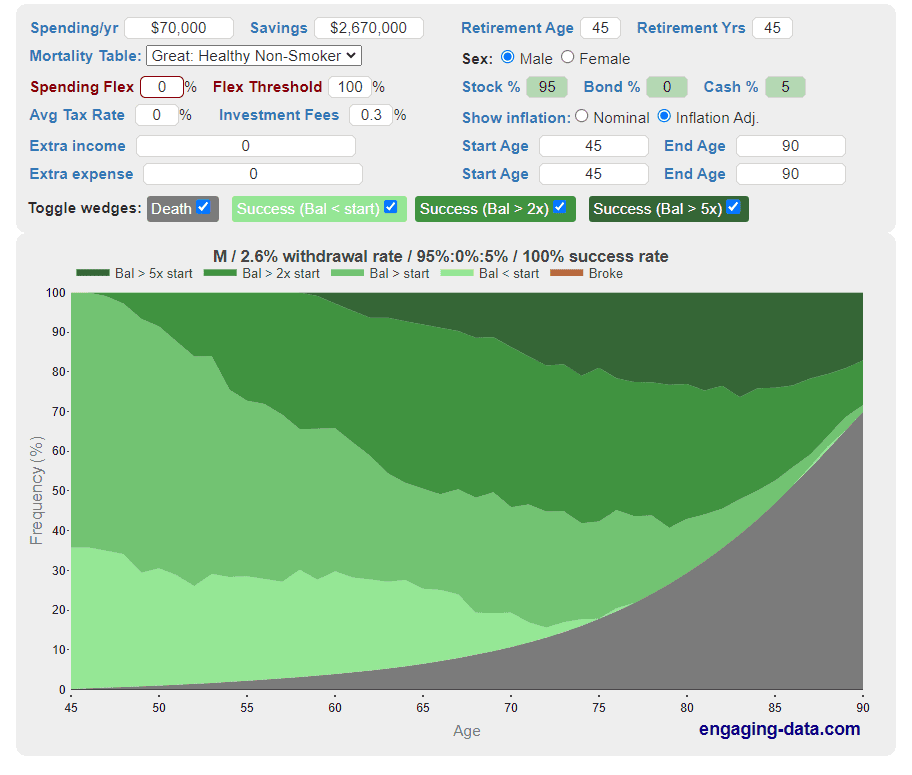

- $70,000 annual spending with a portfolio value of $2.67M. No extra income. 45 years of retirement

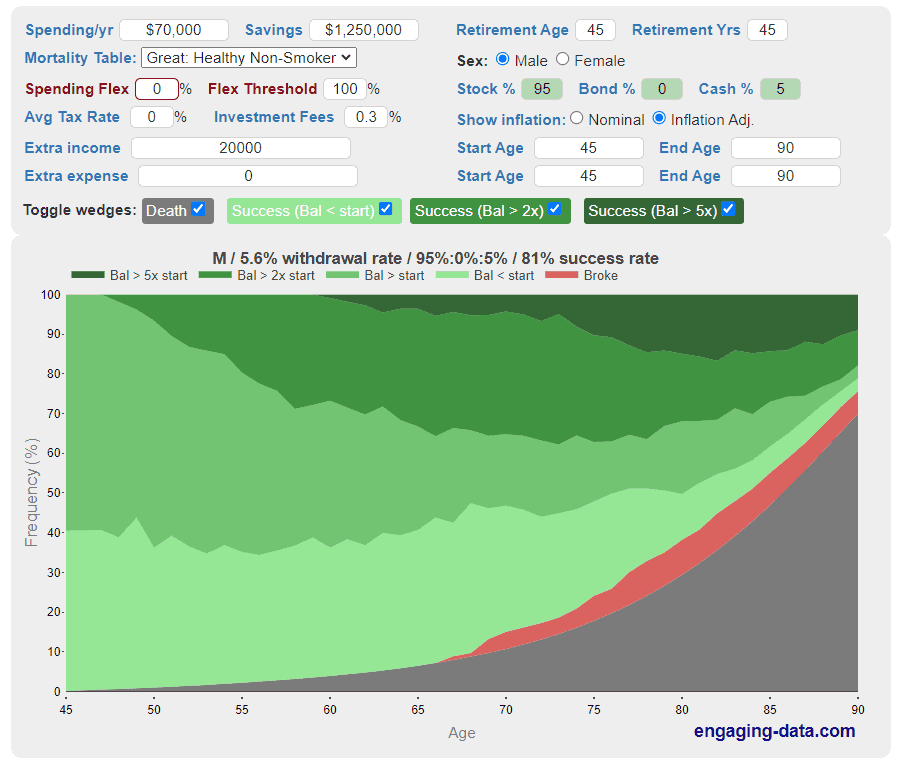

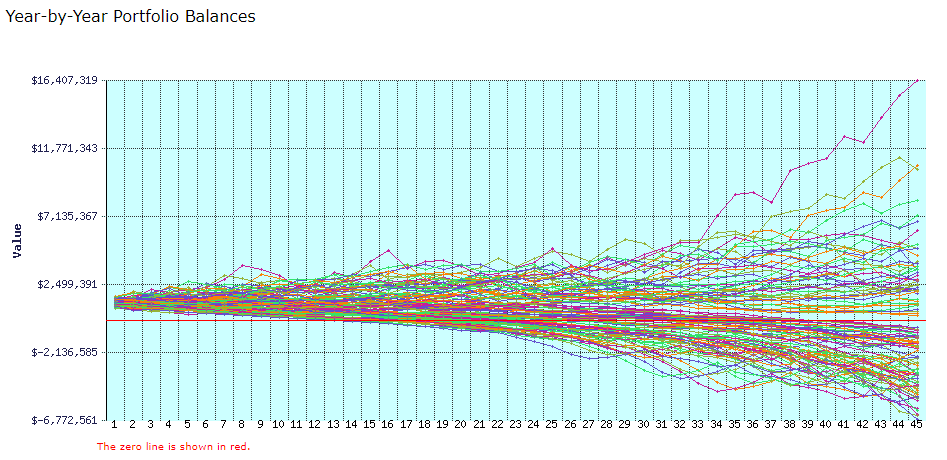

- $70,000 annual spending with a portfolio value of 1.25M. $20k part time income per year for the first 10 years. 45 years of retirement.

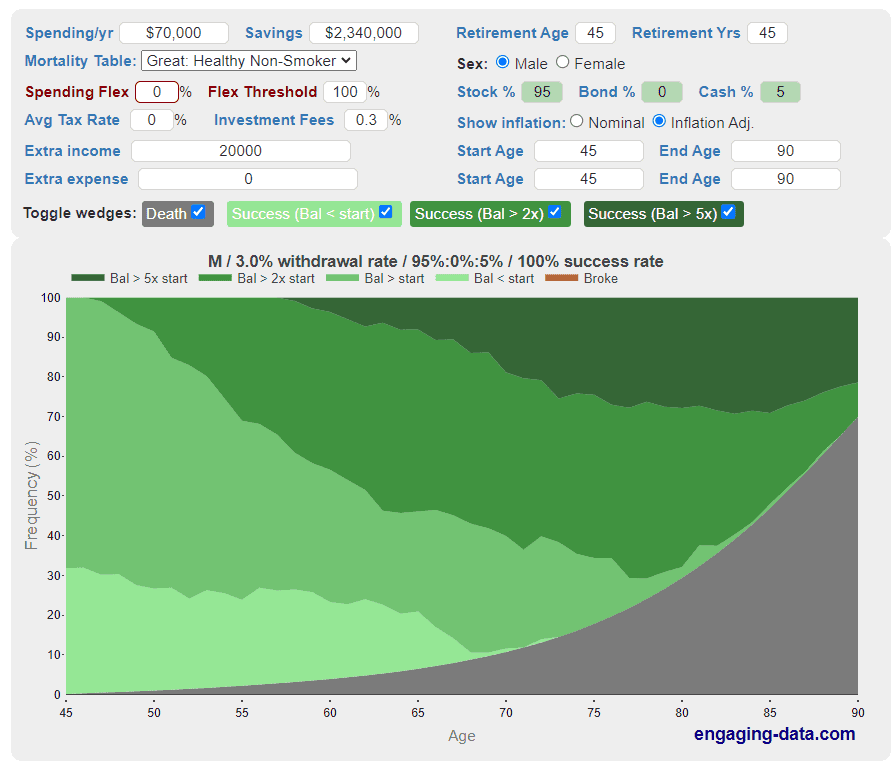

- $70,000 annual spending with a portfolio value of 2.34M. $20k part time income per year. 45 years of retirement.

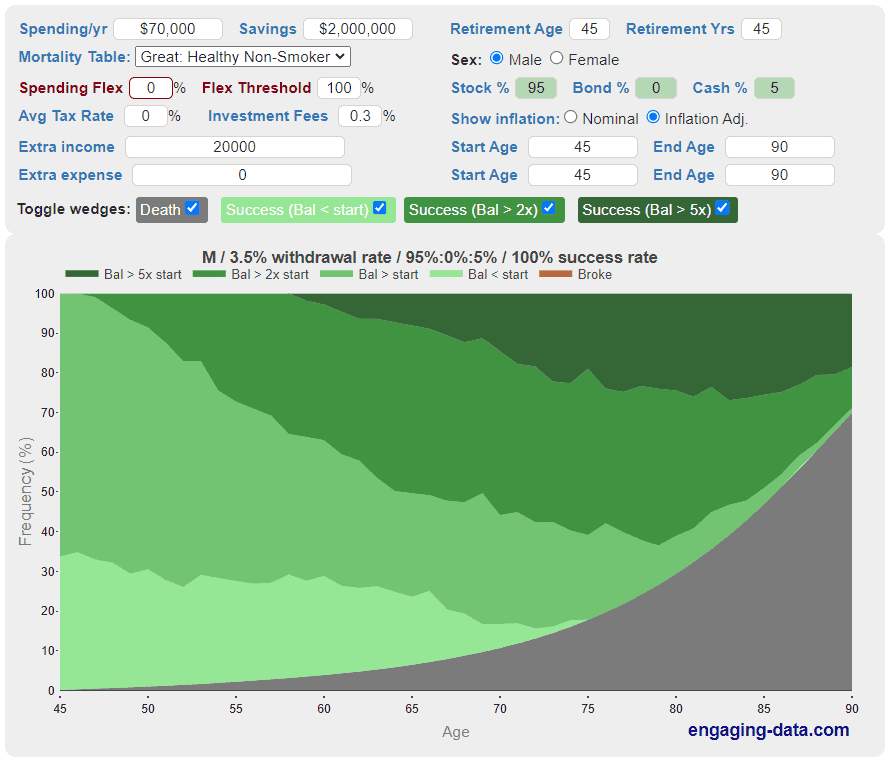

- $70,000 annual spending with a portfolio value of 2M. $20k part time income per year. 45 years of retirement.

Scenario 1

Scenario 1 has the following parameters: $70,000 annual spending with a portfolio value of $1.75M. No part time income. 45 years of retirement.

Here there’s some risk of running out of money. It’s not a surprise given the low portfolio value and the 45 years of retirement. Interestingly, the potential failure only shows up after age 65.

Scenario 2

Scenario 2 has the following parameters: $70,000 annual spending with a portfolio value of $2.67M. No extra income. 45 years of retirement.

Since scenario 2 has the largest portfolio value, it’s not a surprise that things are looking relatively solid with no risk of running out of money at all.

Scenario 3

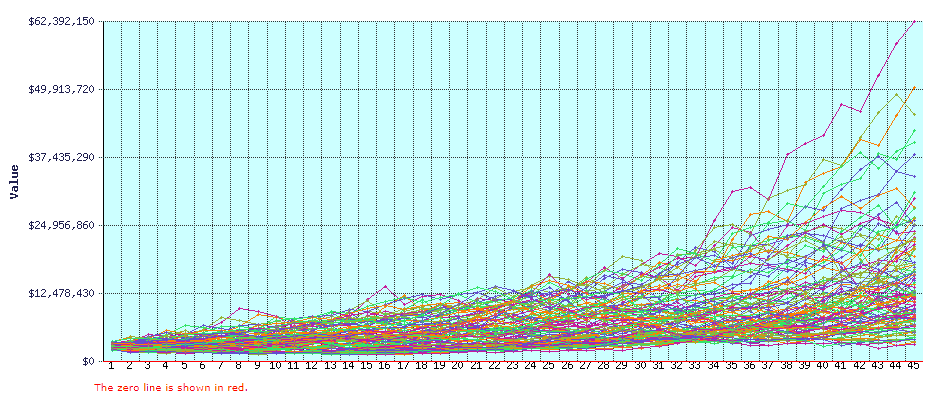

Scenario 3 has the following parameters: $70,000 annual spending with a portfolio value of 1.25M. $20k part time income per year for the first 10 years. 45 years of retirement.

Since there’s no part time income option available for FIRE Calc, many lines are below $0, meaning we’d end up broke in these portfolio simulations. But this is not realistic given we are ignoring the $20k part time income each year.

Scenario 4

Scenario 4 has the following parameters: $70,000 annual spending with a portfolio value of 2.34M. $20k part time income per year. 45 years of retirement.

Overall, this scenario seems relatively safe without any risk of going broke during the 45 retirement years. This is a bit expected given the large net of $2.34M.

Scenario 5

Scenario 5 has the following parameters: $70,000 annual spending with a portfolio value of 2M. $20k part time income per year. 45 years of retirement.

This scenario seems relatively safe.

Some thoughts & analysis

As you can see, I could have run many more different scenarios. In other words, it’s easy to get carried away with running post-FIRE simulations and determining whether the different scenarios are safe.

Here are some thoughts and analysis from the five scenarios above:

- The two simulators I used are very simple. For example, FIRE Calc only takes in 3 parameters. While Engaging Data’s simulator allows for more parameters, they are set for the entire duration of the retirement. Take part time income. The $20k I set was used for the entire retirement duration. It would be useful to set the part time income for only certain years.

- Although I could have done a lot more simulations by using other online calculators or spreadsheets, I didn’t want get into the nitty gritty details. The five scenarios I ran above gave us a relatively high level picture of the success rate of the different investment portfolio values.

- Flexibility is very important in retirement. Rather than spending the same amount of money each year (i.e. $70k) or using the same withdrawal rate (i.e. 4%). Being able to spend a little bit less based on market performance and being able to generate some income will create more margin of safety in retirement.

- Scenario One at $1.25M has a success rate of 81%. But if you look at the chart closer, the failure rate starts at age 67 (0.8% broke). But knowing the typical retirement spending trend, there’s a good chance that we’d end up spending less than $70k at that age given the kids would be out of the house.

- The Engaging Data simulator has two parameters – spending flex and flex threshold. By using these parameters, it would increase the overall success rate. This ties to my flexibility point previously.

- I used a portfolio breakdown of 95% stocks and 5% cash. The success rate can be drastically different if we hold a small percentage of bonds (for a stable income). The simulations also didn’t take into account living off dividends and not touching the principle in the first few years of retirement. There are many levers one can adjust a few years prior to retirement and post retirement. One of the levers is to reduce your annual spending. Another lever to adjust is having a large cash reserve so you aren’t forced to tab into your principle if there’s a bear market in the first few years of retirement. You can also shift a small portion of your portion into higher yield dividend stocks or preferred shares to generate more income (potentially have a lower total return though). The more levers you have on your hand, the higher the success rate you will have.

- Generally speaking, having a large cash reserve is a good idea in post retirement, especially the first 5 to 10 years of your retirement. The large cash reserve could be considered as a rainy day or emergency fund. Having a large cash reserve allows you to not touch your principle. The worst thing to do would be to retire in a bear market and withdraw money that makes up a large percentage of your principle. For example, imagine retiring with $1M and withdrawing $40,000 from your portfolio every year. At the same time, the market see an annual 30% correction for the next five years. If you do that you’d end up with a portfolio value of just under $170k at the end of the fifth year. If you use a 4% withdrawal rate, you’d end up with a portfolio value of just over $203k but you’d be withdrawing below $20k starting in year 3. Cash and cash flow are the king in retirement.

- Generally speaking between $1.25M and $2.67M in retirement savings should work for us. Since we want a bit of flexibility and a margin of safety, I would lean toward the midpoint of this scale. Knowing what we know, I think perhaps $2M in investment portfolio is a good number to aim for.

- As mentioned, the simulations above are very simplistic. We really should fit into the calculations the notion of three phases of retirement – exploring, nesting, and reflecting. Your annual expenses would decrease as you go through the three phases.

Summary – How much do we need to reach financial independence?

One can run a lot of simulations via a spreadsheet or online tools. Ultimately, there’s no way to guarantee with 100% certainty that your retirement plan will work. Life is fluid and things can – and do – change. The important part is to understand that plans can and will change and be adaptable to these changes in plans.

So how much do we need to reach financial independence? For me, I don’t think there’s a magic number. But if I have to put a number, I think $2M in our investment portfolio should give us a sufficient margin of safety.

We are very fortunate that our dividend portfolio generated more than $56,000 in dividend income for us in 2024. If we continue doing what we have been doing since 2011, I am pretty certain we will hit the $2M mark and reach financial independence before the end of this decade. The key, of course, is to enjoy life while on the financial independence journey, and not rush to reach financial independence.

Hi Bob, you mentioned you couldn’t add part-time income into your simulation.

I have been playing with projections and simulators myself and the best one I found is ProjectionLab. https://projectionlab.com/

Not a plug or sponsor. Came across it myself while researching on Reddit. The only downside is that it has a monthly fee. (cancellable at any time)

I tried it for a month and found it to be quite good. Just something for you to look into 🙂

Thanks Jeffrey, will take a look and give it a try.

Great stuff, Bob!

Just to clarify the work we did for you, for your post that you linked to (which remains very relevant for anyone wanting to consider FI/FIRE), while these were overviews of what you could spend to retire at 40, 45, etc., these are in fact very real calcuations; recall they included part-time work in many cases/scenarios, until the last one. 🙂 Even then, so many factors are assumed like rates of return, taxation, inflation and more which are always subject to change – and change they will for all of us….

That said, back to you, you have a robust overall plan and you’ve thought of many risks to mitigate.

I do think, over time though, your thoughts about personal finance and investing and “how much is enough” will change. Life has a way of doing that to all of us.

Continued success my friend, best wishes for 2025 and stay in touch!!

Mark

Thank you Mark.

Phew, financial independence …

Use to be pretty close to this, until we had the kiddo and then immigrated. From being middle-class in Romania to starting from scratch in the US. Cannot complain, we love it here, but it’s been a pretty big battle to get my business up, get a house etc. The only upside is that I don’t think I’ll ever fully retire or just enjoy the FIRE lifestyle, as I love working online and (shockingly) it relaxes me 😀

Kids are expensive but we’ll worth it.

If you enjoy working online then no rush to FIRE.

There is no perfect or right answer. The age old personal finance is “ personal”. “Old you” may have FIREd but the “today you “ is living well with all the trips you take and the life you are living . You look like you are doing what you want to do and it is easier when you have the Income to take these trips including ones subsidized by work.

Living life is the point. If you have a bucket list of travel you want to do while young, have the time to do it, and can still work to fund them then take advantage. It will feel tougher without the income.

I am in my OMY currently. I am thinking of it as a victory lap. It is a easy year at work at the normal stupid things matter less. I get to graduate when my oldish graduates high school this year

I won’t lie the extra year of cash cushion building during what may be an interesting investing year due to politics isn’t bad either.

As much as we all think retiring is about money I would argue that it is more about emotions. Math is easy, being a human is hard

Hi Vader,

Well stated. Yup it’s personal. If we can plan life via spreadsheet then being a human would be super simple.

Thankyou as always for the detailed analysis, learning a lot.

What I appreciate the most is your candor and honesty with your journey.

We’re ready to fire, but also not. And that’s ok. We haven’t yet aligned as a couple on what our next life will be. There’s lack of confidence in the numbers. Our lifestyle is getting better and we want our numbers to keep up rather than having to pare back. So we’ve committed to keeping an eye on the prize, with the prize being a moving target

And for us, that works.

Hi Al,

You’re very welcome. It’s important to align as a couple so you can chart out your post FIRE life. Lack of confidence in the numbers is one of the biggest reasons why people fall into the one more year syndrome. For us, our numbers aren’t quite there just yet.

Nothing wrong with a slightly moving target. Life isn’t static after all.

You and your family seem to enjoy a wonderful quality of life together. Being secure financially early in life as you are now will only be sweeter in the years to come. Don’t rush it, you will know when you’re ready.

Thank you Laura. 🙂

I just want to throw in something that people tend to not consider in older age, and that’s the cost of drugs. My mom has diabetes, and she’s prescribed so many types of drugs. She and me dad have always been of modest means, and both are in their 70s, retired, but now are needing to pay for drugs. Property tax, utilities and just everyday things continue to go up and they find that they really have to watch their spending. They can’t afford to pay for therapies or alternative treatments out of pocket. All this to say that I wouldn’t think spending is less in later years, but likely the same if not more.

Hi Brenda,

That’s a good point, health expenses could be significant as you age.

Good one Brenda – seeing this with my in laws. Drugs, RMT, chiro, travel medical insurance. It’s eating into their daily expenses! Will build this into my projections.

Great post as usually. Love the risk analysis.

Some great feedback from posters as well.

I’m in my early fifties and really starting to look at unplugging. As an earlier poster mentioned you do have to look at all your sources of income but I don’t think enough time is spent on the expense side. I’ve recently done a detailed expense analysis and was shocked to see that my family needs $120K per annum to live. I am very cost conscious (Don’t eat out at all) but I do enjoy my cottage, toys, some travel and that doesn’t even include putting 3 kids through university. Every situation is different is what I’m saying I guess and its just as important to know what you need and why you need it. I do see the picture is getting clearer and I’m also going to be working a little longer than I thought.

Thank you!

Yes one way to look at this is reducing annual expenses so we don’t need as high dividend income. 🙂

Personally I think its wrong to focus on how much capital we need to retire. It should always be about how much income is needed, especially for dividend or dividend growth investors. If we were strictly focusing on a capital $ target how would pension CPP & OAS figure into the equation? Each is $ income usually paid monthly. For example say one is paid $2,500 company pension, $1,200 CPP, $700 OAS and $1,800 RRIF income every month. How does one convert those monthly income payments into an overall “X”M capital amount?

Hi Bernie,

Very fair. Unfortunately most of the FIRE calculators I found only consider withdrawal rather than cash flow via dividend. You simply can’t calculate everything. 🙂

Hi Bernie

I built that out for our family working with our financial planner. Dividend income is one (large) piece of the post retirement income pie, but there are also work pensions, RRSP, CPP and OAS were factored in. Helped me feel a little more at ease so I wasnt fully dependent on just the dividend income.

Hi,

Using a Range of 3.0 to 4.0 % average dividend income imo and experience is a pretty conservative range for your retirement years. That was the average dividend range of our investment portfolios during our latter accumulation years, but when we retired (a few years ago), I sold most of our high growth, low dividend stocks (railways, groceries, ATD, DOL, WCN as examples) and capital growth focused stocks and invested the proceeds in the higher paying bluechip dividend growth stocks we already owned (and added a few others). We are currently, averaging 4.5-5.2% dividend income. This approach could greatly reduce your $2million target.

Best of luck with your decision.

Hi Paul,

That’s a fair comment – going with higher yield dividend stocks rather than low yield ones to boost dividend income. Something to consider for sure.

Wow, tough crowd! 🙂

In all seriousness, I feel like if I was in a similar situation (long term employee at a company which has been making frequent layoffs) I would consider sticking around for a year or two just in case I was next in line for a payout. Not saying that is your thought process, but that consideration would be hard for me to ignore, personally.

Many things to consider, I think it makes sense to sit tight until you are absolutely certain that you are ready to take the next step.

Haha it’s all good. It’s nice to get feedback from folks.

As mentioned in last week’s post, we randomly set 2025 as the year to live off dividends. While we can probably do that this year by supplementing dividend income with part time income, we aren’t quite ready to pull the trigger yet. The idea is to step back in 2 years but as we can closer to that so called “end date” we’ll have to re-evaluate. I really don’t think we’re falling into so called “one more year syndrome.”

The thing we don’t want to do is to continue to hold off FIRE only indefinitely. 🙂

Do the calculators factor in government benefits, your kids having part time jobs so they learn the value of a dollar, average market returns historically and dividends? RESPs, scolarships and bursaries as well as being an emptynestor. You will not need as much as you think…talk to people who have been there and done that as you already have)they can’t spend it fast enough) .

To me you keep moving the finish line and will fall into a never enough trap. Take into account less driving as you are not working and needing to put as many miles on your vehicle. Also having less costs per month once your mortgage is gone and kids moved out gradually over time. You actually spending less once the retirement honeymoon phase is past.

I pulled the plug 10 years early and let my finances build while i worked in a less stressful field part time and looking back I would not give that up for the world as it allowed me to see and guage how much i needed and made while i was still capable of going back full time if i needed to (i didn’t). Now I no longer want to do anything but enjoy my hobbies, travel and me time. your finances and resources will do better than you think and you will make more than the 3-4%. You only get the chance to live once…don’t waste it on moving the finish line as you will be dead and leaving a lot of money to the tax man who wont care, but will be happy to take it. You already have basic expenses covered, what is holding you back from pulling the plug next year and living a bit more and allowing your money to grow while your wife still works part time too? I too was a type A personality but, I learned to live…its worth the chance.

Hi Lou,

My simulations were very simple so I didn’t include things like kids having part time jobs, scholarships, bursaries, and empty-nestors. Simply too many variables to consider. 🙂

You bought up very good points, you probably won’t need as much as paper calculation. Since you are ahead of us on the FIRE front, I really appreciate your comment/feedback.

Great post! I like the analysis since we’re getting close to our goalpost too and I keep second guessing when the right time is to pull the trigger (we are also moving our goalpost all the time) . Does your $2M number include ALL investments (RRSP, TFSA, pension, pension, non-reg) excluding your home? I’ve noticed that some bloggers quote different numbers.

Hi Marilyne

Correct, the $2M number is for investments only, excluding our home.

The reality is that FIRE suffers from diminishing marginal utility as you age. As you grow older and wealthier, the perceived benefits of FIRE decrease. The most significant advantages would typically occur in the early years of your children’s lives, generally in your 30s. Beyond your mid-forties, FIRE tends to function more as a safety net (for most people in the developed world, mainly a psychological one).

This is not to say that pursuing FI is bad; it is precisely the opposite. I am just reflecting on the reality of diminishing marginal utility on the RE front.

Hi Daniel,

Interesting point on diminishing marginal utility, I get your point but not sure if I fully agree. IMO RE does provide benefits at different stages of your lives.

“ The most significant advantages would typically occur in the early years of your children’s lives, generally in your 30s. ”

I agree. FIREing when the kids are young and still at home creates huge benefits for the family and the children. But firing after the kids leave home negates a lot of the benefits. You’ll be retired, but won’t have the most precious people in your life to spend time with anymore because they’ll be gone doing their own thing.

I wouldn’t trade being a stay at home dad since my son was born in 2017 for anything. The titles and the money and the promotions are not worth it. It’s not even close if you have the option to FIRE.

Please believe me on this Tawcan.

Totally believe you. 🙂

Great article with so many resources.

My philosophy is that you can’t have enough money.

It’s like those Government cost predictions for a project. What ever they say always double/triple the cost and double/triple the time to completion.

Nice analysis. It just seems like one more year though. What’s so important about your work that you keep on holding on and denying the things that you really want do?

You’ve been writing about financial independence for so long, it just seems like you’re never going to do it at this point.

Brandon from the Madfientist retired years ago and never mentions his wife works as an optometrist making six figures. Maybe you can go that route and claim FIRE, and don’t mention your wife providing, as a balance.

Good luck!

Hi Derek,

I wouldn’t say we’re never going to do it. It’s just a lot of internal analysis and thinking. As mentioned below, I’m the prime income provider for the household. We’re not like other “retired” folks where a spouse will continue working full time once another spouse retires. As mentioned, we may both continue to work part time if we choose to.

I echo the comments from Financial Samurai. When I read the article and have been following your blog for years, it feels like you will never reach your target as it gets moved higher and higher. I guess it is the “one -more year syndrome”. I can relate to this as well as I have been doing something similar in the last few years but hopefully I will make a decision this year. In our situation, I am asking myself what will I regret in 20 years and the answer is not I wish I worked more and made more. With your wife working and future part-time income, if FIRE is really what you want then you will have to make a decision sooner than later. I hope you do not take the above as criticism as most of us fall in the same trap.

Hi Kevin,

Yes, definitely need to watch out for the “one more year syndrome.” A lot of folks in the FIRE community fall into that trap, perhaps I’m slowly falling into it too? 🙂

Not taking your comment as criticism at all, it’s always nice to hear from people ahead of us and receive feedback.

$2 million sounds about right if you want to live on $60-70K after tax for a family of four. But wouldn’t your costs go up further in five years in 2030 as well?

It feels like the goal post continues to move every year. And that it might just be one more year every year until you reach the traditional retirement age of 60+.

Correct me if I’m wrong, but it seems like you are increasingly wanting to FIRE but are growing frustrated that you can’t or are not. This is based on recent posts and your annual posts about FIRE.

I would say just go for it or take a sabbatical to see what it’s like. You have a wife who can support you and the family. It’s not as scary as you think. If you take the leave of Faith, you will also head against regret from not making the move sooner and doing what you want.

Yes, I know there is a big difference between FIRE on paper and actually retiring early. And it is comforting to tell yourself that you are lean FIRE. But nothing to compare to actually having the courage to live the life you really want.

Give it a go and support your wife’s work efforts. There are men who FIRE nowadays and have wives continue to work.

Sam

Hi Sam,

It does feel like that doesn’t it – goal post continues to move every year? No, I’m not frustrated that I can’t FIRE. At this point, I think we are very close to hitting that milestone. Taking a sabbatical and give it a go it definitely a good idea.

How are you factoring inflation into your assumptions?

40,000 in the year 2016 is how much in 2025 dollars?

Did your portfolio distributions match inflation over that time?

What about going forward?

Hi Fred,

Yes inflation is taken into assumptions… the idea is that both dividend income and portfolio value should increase over time and growing faster than inflation.