In December, I wrote about the Canadian dividend stocks we’d consider buying for TFSA in 2025. With the TFSA contributions behind us and purchases made already, it’s time to look ahead to other dividend stocks we are considering buying in 2025.

We typically follow this contribution and purchase pattern – max out TFSA first, then max out RRSP, and finally contribute to non-registered accounts. It is always advantageous to max out the tax-advantaged and tax-deferred accounts before contributing to non-registered accounts because non-registered accounts will create tax implications for us.

Since we are talking about purchasing stocks in RRSP and non-registered accounts, we are no longer only looking at Canadian dividend stocks, we are considering US dividend stocks and US index ETFs as well.

Long time readers will recall we already hold many individual dividend stocks and index ETFs in our dividend portfolio. Therefore, for the 2025 purchases, we plan to add more shares to existing positions rather than starting new positions. With that in mind, here are five dividend stocks we plan to buy in 2025.

Stock Consideration #1: Brookfield Asset Management

I mentioned BAM in our stocks to consider for the 2025 TFSA list and I decided to mention it again on this list. Why? Because I believe that BAM is very well managed and is poised to grow both dividend payout and share price.

Currently, BAM makes up less than 2% of our dividend portfolio so it makes sense to increase that exposure to somewhere between 3 to 4%.

Well, basically the same reasons as before – Brookfield continues to be one of the best-managed companies in Canada. With the CEO Bruce Flatt at the helm, it’s hard to ignore Brookfield Asset Management.

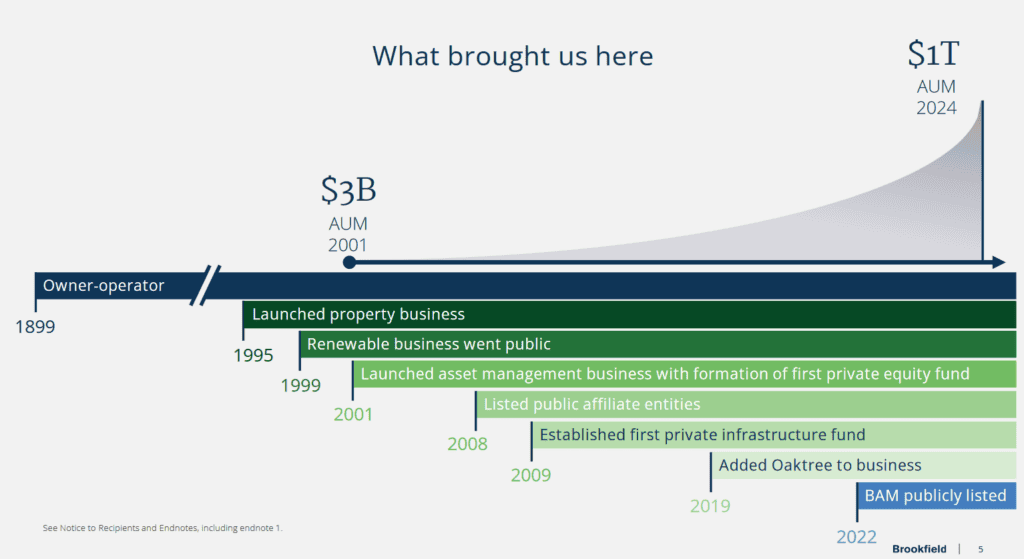

Brookfield Asset Management has an impressive record over the years – growing its assets under management (AUM) from $3 billion in 2001 to over $1 trillion in 2024. BAM has a hefty goal to double the AUM to $2 trillion in the next five years!

Brookfield Asset Management manages many different types of assets – renewable power & transition, infrastructure, private equity, real estate, and credit. The company operates in over 30 countries so it is well diversified geographically.

Why do I like BAM? Because I think the management uses a simple three step approach when it comes to growing the overall business:

- Identify high qualify businesses

- Acquire them and invest in them

- Enhance cash flows through operational improvements

This seems very easy on the surface but hard to do in practice. Fortunately, BAM has a good track record to demonstrate that they have been able to successfully grow its business and follow the simple three-step approach effectively.

Furthermore, BAM is expected to grow between 15-20% for the next five years with dividend payout to grow between 15-20% over the next five years. These are signs that the management wants to reward shareholders.

Potential Risks for Brookfield Asset Management

Can Brookfield Asset Management continue to execute operationally? I believe that’s the biggest risk for shareholders. If Brookfield can’t enhance cash flow through operational improvements in the businesses and assets they own, the company will see a drop in profitability and revenues.

However, given the historical track record, I believe shareholders can rest easy and let BAM’s superb management do the work.

Another risk for dividend investors is a drop in dividend payout. Due to how BAM is set up, dividends will only be paid if the company is profitable and has free cash flow. If the company faces financial challenges or downturns, it is possible to see a decrease in dividend payout.

Having said all that, I believe a decrease in dividend payout is highly unlikely.

Stock Consideration #2: Invesco NASDAQ-100 ETF (QQQM)

We previously invested in Invesco QQQ ETF which tracks the Nasdaq 100. But after a bit of research and comparison, we found that QQQM has a lower MER (by 0.05%) which can make a big performance difference over a long period.

As a result, we have switched from QQQ to QQQM to take advantage of the lower MER.

The number one reason for adding more QQQM shares is to take advantage of the solid performance of the Nasdaq 100. Historically, the Nasdaq 100 has outperformed the S&P 500 and the TSX.

Why? Because the Nasdaq 100 has heavy exposure to sectors like technology, consumer services, and health care. And over the last few decades, these sectors have done very well, especially the technology sector (where the key innovations come from).

Adding more QQQM shares would allow us to grow our exposure to the Nasdaq 100. At the time of writing, our exposure to the Nasdaq 100 is slightly over 2% so it would be nice to have this number grow to about 5%.

Since total return matters more than dividend income, adding more QQQM shares will hopefully help propel our dividend portfolio value toward new highs.

Potential Risks for QQQM

The biggest risk for QQQM is its heavy exposure to the technology sector. When I looked at its top ten holdings, nine out of the ten holdings are in the technology sector. The only holding not in the technology sector is Costco.

Due to the heavy exposure to the technology sector, if we see a dot-com-like crash, things can get pretty ugly very quickly for QQQM shareholders.

But again, no pain no gain, right? We are holding QQQM for potentially higher returns, therefore, we should anticipate a higher risk.

This is exactly why we continue to believe that portfolio diversification is important and that we can’t simply go all in on QQQ or QQQM.

Stock Consideration #3: National Bank

Over the last five years, National Bank has outperformed compared to its Canadian banking peers. Although the stock saw a dip when the company announced the plan to acquire Canadian Western Bank, the share price has since recovered and gone higher.

One of the National Bank’s advantages is that it is small compared to the Big Five Banks. This means there is still a lot of growth available to the National Bank. Acquiring Canadian Western Bank will allow the National Bank to accelerate domestic growth, especially in Western Canada.

Although NA composes a little over 5% of our dividend portfolio, I would not hesitate to add more. I’d be comfortable seeing NA making up between 6 to 6.5% of our dividend portfolio.

NA has 14 years of dividend growth streak with an 8.2% annualized dividend growth rate over 15 years. With a dividend yield of slightly over 3%, it is quite attractive for dividend investors like us.

Potential Risks for National Bank

Like all Canadian banks, National Bank makes a large percentage of its profit from mortgages. The biggest risk for the National Bank, therefore, is mortgage delinquencies and defaults.

Throughout 2024, Canadian Banks set aside money to cover bad loans and I expect them to continue to do so throughout 2025. Although interest rates have decreased from a high of 5% and the inflation rate has also gone down, some homeowners will still default on their mortgages.

Does this mean one should avoid buying National Bank completely? I don’t think so.

National Bank and other Canadian banks are well-regulated and have been protecting themselves from bad loans by setting money aside. This is exactly what the Canadian banks did during the COVID-19 pandemic. When there weren’t as many loan defaults as expected, the banks then used the loan loss provision money to invest and or return the money to shareholders in the form of a higher dividend payout and/or bigger share re-purchases.

I expect not as many mortgage defaults in the coming years as anticipated so National Bank will reinvest the loan provisioning money for business growth and distribute it to shareholders in the form of dividend payout increases.

Long term, I expect the bank to continue making record-setting profits and reward its shareholders.

Stock Consideration #4: Costco

As a shareholder, I love Costco and the well-known fact that the warehouses are always packed. As a shopper though, I love Costco’s awesome prices but I don’t like how the warehouses are always packed.

Ah, the love-hate relationship!

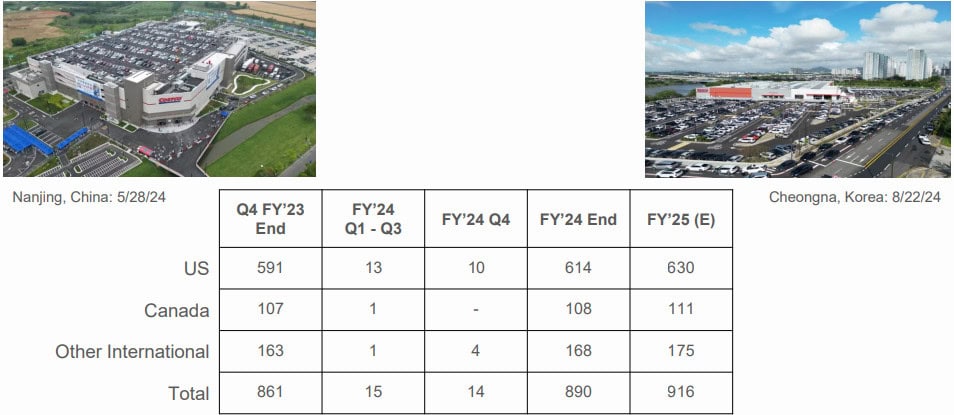

Costco is the third largest retailer in the world and operates a chain of membership-only big box warehouse club retail stores. At the time of writing, Costco operates 890 warehouses worldwide with 614 in the US, 108 in Canada, and 40 in Mexico.

As a shareholder, I believe Costco still has a lot of growth possibilities. Costco has 14 stores in Taiwan, 7 in China, 4 in Spain, and 2 in France. The company should be able to continue to expand in these countries by opening more warehouses.

In fact, Costco plans to expand from 890 warehouses at the end of 2024 to 916 by the end of 2025.

Unlike other retailers, Costco doesn’t make a lot on sales. Instead, it makes money through its membership fees. Recently, the company hiked membership fees for the first time in seven years which will impact an estimated 52 million members globally. Given the worldwide membership renewal rate is over 90% and the US & Canada renewal rate is over 92%, the membership fee hike should help Costco bring in more revenue.

Potential Risks for Costco

The biggest risk for Costco is whether the company can continue to see over 90% membership renewal rate globally. If the renewal rate drops, this will significantly impact Costco’s revenue. Can Costco attract new members with the higher fees? That’s another interesting metric to examine.

Costco stock has performed strongly over the last five years, returning 200% during that period. But at over 50 PE ratio, the stock is anything but cheap. Can the stock price continue to appreciate over the long term?

Despite high traffic at Costco warehouse and a crazy parking situation especially on weekends, people seem unable to say no to good prices, Mrs. T and I included. The warehouse bulk purchase model has worked for Costco for years and I have no doubt it will continue to. As shareholders, we expect to continue to get rewarded.

For the last consideration, I’m going with another index ETF. Why? Because I believe hybrid investing – owning both individual dividend stocks and index ETFs is the best approach to investing long term.

One word – diversification.

XAW is extremely diversified geographically and sector-wise. This ex-Canada all country ETF has 8,689 underlying holdings with over 65% exposure to the US, over 5% exposure to Japan, over 3% exposure to the UK, and over 2.5% exposure to China. When we look at it sector-wise, XAW has more than 10% exposure to the IT, financials, industrials, consumer discretionary, and health care sectors, respectively. Thus, it is very well diversified.

Since we own a lot of Canadian dividend stocks, utilizing XAW allows us to increase our exposure globally. It also allows us to invest in international stocks like Microsoft, META, Berkshire Hathaway, Broadcom, and Taiwan Semiconductor Manufacturing Company that we don’t hold in our portfolio. XAW is a simple and low cost way to own US, international and emerging market stocks.

Potential Risks for XAW

Because XAW’s geographical allocation is over 60% in the US, the performance is heavily weighted to the US market. Therefore, if the US has a recession, XAW will perform poorly.

About 12% is invested in emerging countries. Since emerging countries could be considered more risky and volatile than developed countries, this could drag down XAW’s overall performance. For example, if we look at XEC, iShares Core MSCI Emerging Market index ETF, that XAW holds, the ETF has almost 25% exposure to China, 20% exposure to India, and almost 20% to Taiwan. So any economic downturns and/or geopolitical issues to these countries could impact XAW’s performance.

Having said that, I think the overall risk is low for XAW due to its diversified nature. XAW holds over 8,600 different stocks and only seven of those stocks (Apple, Nvidia, Microsoft, Amazon, META, Alphabet, and Berkshire Hathaway) make up 1% or higher of the XAW.

Summary – Five dividend stocks we plan to buy in 2025

There you have it, the five dividend stocks we plan to buy in 2025 in our RRSPs and non-registered accounts. Since we plan to buy some US stocks and an ETF, we would need to consider using Norbert’s Gambit to save on the exchange rate with Questrade. Since Wealthsimple Trade doesn’t support Nobert’s Gambit, we may need to just take the exchange conversion fee that Wealthsimple charges.

Dear readers, which stocks are you planning to buy in 2025?

Hi Bob,

I am currently debating between going all in on VEQT vs picking my own dividend stocks.

If you were starting out today, which strategy do you recommend? All-in-one ETF or picking multiple dividend stocks?

Hi Jeffrey,

That depends on how much money you’re starting out. If you’re starting out with a small amount of money, I’d go 100% all in on VEQT or XEQT. If you have say $100k or more I’d probably split 50-50 between all-in-one ETF and a handfull of dividend stocks.

Hi Jeffrey…. Im with you. Over the decades I have amassed a long list of individual shares and ETF’s. It’s primarily because of my ‘addiction’ to dividends. As the time-of-life arrives to begin to liquidate assets, I’m finding it difficult to choose what to sell. Im sure I’m not alone with feeling a relationship to specific holdings. If I swapped my holdings to VEQT (or similar), it would remove the barrier of what to sell. Yet here I sit, paralyzed by wondering what to sell first to create cash for VEQT!

“It is always advantageous to max out the tax-advantaged and tax-deferred accounts before contributing to non-registered accounts because non-registered accounts will create tax implications for us.”

While true, I think another concern is the “middle class trap”. Where, for example, you may own a home (with or without a mortgage) and have investments in an RRSP and want to retire earlier than 65. However, you may be trapped. You have no cash flow or assets you can live off because wealth is trapped in home equity and RRSPs (assuming you don’t want to withdraw from your RRSP early).

That’s a very good point. That’s why one should consider early RRSP withdrawls.

Does this selection mean that you plan to turn more towards growth investing?

No, not exactly.

WS has a very steep 1.5% FX conversion fees. I would use my USD bank account and transfer using this account instead of paying WS FX Conversion fees. As well I think, WS accounts should be kept for trading CAD stocks only and use IB for USD Transactions.

Questrade has a 1.5% FX conversion fees too, just that you can avoid that fee by using Norbert’s Gambit. 🙂 WS seems to have a bad name for currency conversion because they don’t support Norbert’s Gambit. It would be very nice for WS to support Norbert’s Gambit one day.

Interestingly, WS just updated their FX fees so you can get below 1.5%. Mind you, you need to exchange a large sum of money to reduce the FX fees – https://www.wealthsimple.com/en-ca/legal/fees/trade

Do you exchange CAD to purchase US stocks/ETFs? Wouldn’t you lose some money to exchange fees, unless you have USD income?

We use Norbert’s Gambit for CAD to USD conversion – https://tawcan.com/norberts-gambit-save-money-on-cad-usd-conversion/

Lately we have been accumulating USD via US stock dividends.

you might like to look at TEC (TD Global Tech Leaders Index ETF….it tracks the Solactive Global Technology Leaders Index) and has significantly outperformed the QQQ over the years. TEC has an MER of 0.35% which is higher than QQQ and QQQM but its outperformance easily makes up for its higher MER.

I would also prefer, after I have bought XIC, XIU, or more likely lower MER ETFs like VCN or ZCN (for Broad Cdn exposure) and TEC (which is 88% USA companies), that my next ETF would be an ex-North American ETF so that I am not investing in the Cdn or American stock markets….so I would not chose to buy XAW which has 65% USA holdings.

So the question is: Which ex-North American ETF is the best to buy that has a low MER?

thanks

JD

Hi Janice,

Can’t say I have looked into TEC yet. Interesting that it has outperformed the QQQ.For ex-North American ETF, you might want to take a look at VIU.

Looks like TEC is a Cdn. version ETF ? If the conversion of US / Cdn. takes into account, will there be much difference between QQQ / TEC ? Just curious

Not sure when the article was written but didn’t see any comments on effect of potential tariffs on your pics.

There’s only so much we as individuals can control. There are a lot of uncertainties with tariffs and we’ll see how everything plays out.

Hi Bob, great article once again! I see you mentioned XEC but what are your thoughts on XEF for additional diversification into the more mature international markets (i.e. europe and Japan)? And now that Questrade has zero fees on trading, will you be moving your money back? Appreciate your comments. Thanks!

Hi Barbara,

I haven’t really tracked XEF, been using XAW for ex-Canada international exposure. I think you need to just pick an international ETF and stick with it.

I’ve been very happy with Wealthsimple so not planning to move money back to Questrade yet. Plus, I’m locked with WS for a year (one of the conditions for getting the bonus).

OK, thanks very much for your response. I just read your new post. Your trip to Taiwan looked soo amazing and the food so yummy!