I have always enjoyed connecting with readers via email and social media and receiving potential topic ideas. So when a few readers reached out recently to ask what my thoughts are about the newly created Evermore Retirement ETFs, I was very intrigued. So I started doing more research about these ETFs.

What makes these Evermore Retirement ETFs different than the all-in-one target allocation ETFs like VGRO and VBAL and all equity ETFs like VGRO and XGRO? Are these first-ever target-date ETFs in Canada good for your retirement portfolio?

Here are my thoughts and review of the Evermore Retirement ETFs.

Note: Unfortunately, Evermore has decided to terminate these retirement ETFs.

What are target date funds?

Target date funds aren’t new to the Canadian market. Many target date funds existed before the Evermore Retirement ETF announcement. However, these target date funds usually are high fee mutual funds or only available through specific group RRSP plans. This means they are costly and difficult to utilize.

Evermore Retirement ETFs have a much lower management fee compared to already existing target date funds. The Evermore team created these retirement ETFs with specific retirement years and use a glide path approach. This means each ETF’s asset allocation will gradually change as the ETF gets closer to the specified retirement date.

Essentially, the fund managers will adjust the risk exposure over time by changing the equities to bonds mix for each retirement ETF. The closer the fund is to the target retirement date, the higher percentage of bonds the fund will hold.

Brian See, Evermore’s Chief Investment Officer, explained the idea in this video below:

Evermore Retirement ETFs

Evermore created eight different retirement ETFs with different retirement dates and all of them have the same MER of 0.35% at the time of writing.

The fund prospectus gives a good overview of what Evermore is trying to achieve with these ETFs:

Evermore Retirement 2025 ETF

Initially, Evermore Retirement 2025 ETF seeks to provide capital appreciation by investing primarily in a diversified portfolio of equity securities, fixed income securities and/or money market investments, either directly or indirectly through investment in other exchange of 2025, Evermore Retirement 2025 ETF will seek to provide capital appreciation and income generation by gradually shifting its asset mix to increase the percentage of its assets allocated to fixed income securities and/or money market investments.

The eight available Evermore Retirement ETFs with specific retirement date are as below:

| ETF Name | Ticker | MER |

| Evermore Retirement 2025 ETF | ERCV | 0.35% |

| Evermore Retirement 2030 ETF | ERDO | 0.35% |

| Evermore Retirement 2035 ETF | ERDV | 0.35% |

| Evermore Retirement 2025 ETF | EREO | 0.35% |

| Evermore Retirement 2040 ETF | EREV | 0.35% |

| Evermore Retirement 2045 ETF | ERFO | 0.35% |

| Evermore Retirement 2050 ETF | ERFV | 0.35% |

| Evermore Retirement 2055 ETF | ERGO | 0.35% |

Interestingly, all of these ETFs are listed on the NEO Exchange, the same exchange that lists the Canadian Deposit Receipts (CDRs). Since the NEO Exchange is all about new fintech innovations in Canada, it wasn’t a surprise to me that Evermore listed the ETFs on this exchange.

The idea of gradually shifting the asset mix within each fund and providing both capital appreciation and income generation makes a lot of sense. In theory, bonds serve as safe havens when the market is down. Bonds also provide fixed income. So holding more bonds closer to retirement time or post-retirement should reduce the volatility of your portfolio.

At a 0.35% MER, the management fee is quite reasonable and it’s only about 0.10 to 0.15% higher than the all-in-on target asset allocation ETFs that Vanguard, iShares, and Horizons offer.

To put things in perspective, for a $500,000 portfolio, 0.15% difference is $750 per year. Yes, the $750 per year cost can compound to a large number over time but you are paying the small extra fee for not needing to adjust your asset mix and rebalance your portfolio which in terms saves your precious time.

Evermore Retirement ETFs – Deep Dive

Similar to the all-in-one ETFs like VBAL and VGRO, the Evermore Retirement ETFs are constructed by holding different sets of ETFs. The all-in-one and all equity ETFs from Vanguard, iShares, and Horizon all only hold ETFs from the parent company, whereas Evermore constructed the retirement ETFs by using funds from BlackRock, BMO, and Vanguard.

At the time of writing, all of the Evermore Retirement ETFs holding seven different ETFs:

- iShares Core S&P/TSX Capped Composite (XIC)

- iShares Core S&P Total US Stock Market ETF (ITOT)

- iShares Core MSCI EAFE IMI Index ETF (XEF)

- BMO MSCI Emerging Markets Index ETF (ZEM)

- Vanguard Canadian Aggregate Bond Index ETF (VAB)

- Vanguard Total Bond Market ETF (BND)

- Vanguard Total International Bond ETF (BNDX)

It’s unclear to me why Evermore used funds from different companies. If I had to take a guess, I’d guess that Evermore used these ETFs because they have the lowest MERs.

Due to the retirement target date, each retirement ETF has a slightly different mix of these underlying seven ETFs and also a small percentage of cash.

| Retirement Date | Ticker | XIC | ITOT | XEF | ZEM | VAB | BND | BNDX | Cash |

| 2025 | ERCV | 15.10% | 22.60% | 9.70% | 2.40% | 29.80% | 14.80% | 4.90% | 0.60% |

| 2030 | ERDO | 16.10% | 24.10% | 10.40% | 2.50% | 27.80% | 13.80% | 4.60% | 0.60% |

| 2035 | ERDV | 19.20% | 28.80% | 12.40% | 3.00% | 21.60% | 10.80% | 3.60% | 0.70% |

| 2040 | EREO | 23.70% | 35.50% | 15.30% | 3.70% | 12.60% | 6.30% | 2.10% | 0.80% |

| 2045 | EREV | 26.40% | 39.60% | 17.00% | 4.20% | 7.20% | 3.60% | 1.20% | 0.90% |

| 2050 | ERFO | 27.90% | 41.80% | 18.00% | 4.40% | 4.20% | 2.10% | 0.70% | 0.90% |

| 2055 | ERFV | 28.50% | 42.70% | 18.30% | 4.50% | 3.00% | 1.50% | 0.50% | 0.90% |

| 2060 | ERGO | 28.50% | 42.70% | 18.30% | 4.50% | 3.00% | 1.50% | 0.50% | 0.90% |

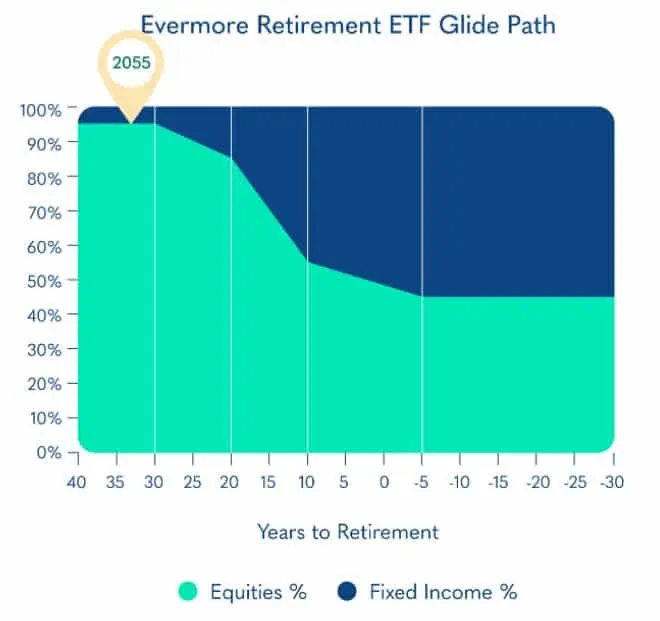

As expected, the equities and bond allocation mix changes over time. You can see the glide path per the picture below. When the retirement timeline is long, the ETF holds A majority of the assets in equities; when the retirement timeline is short, the ETF shifts closer to a 50-50 mix between equities and bonds.

The equities to bonds mix for the different Evermore retirement ETFs are below.

| Retirement Date | Ticker | Equities | Bonds |

| 2025 | ERCV | 50% | 50% |

| 2030 | ERDO | 54% | 46% |

| 2035 | ERDV | 64% | 36% |

| 2040 | EREO | 79% | 21% |

| 2045 | EREV | 88% | 12% |

| 2050 | ERFO | 93% | 7% |

| 2055 | ERFV | 95% | 5% |

| 2060 | ERGO | 95% | 5% |

For me, it’s interesting to see that ERFV and ERGO are currently constructed identically. Given the long retirement timeline of 35 years for ERGO, I was surprised that the Evermore team didn’t invest 100% in equities for this ETF and instead chose to hold 5% of the ETF in bonds. If it were me, I’d totally hold 100% in stocks.

Since geographical diversification is important, readers will be happy to learn that all of these retirement ETFs are well diversified geographically, both in equities and bonds. In fact, all eight ETFs have an equity geographic allocation of 30% Canada, 45% US, 20% international, and 5% emerging and a bond geographic allocation of 60% Canada, 30% US, and 10% international.

Having said that, I wasn’t able to find the underlying sector allocation for each ETF. It would have been helpful if Evermore could provide such information.

Should I hold Evermore Retirement ETFs – My thoughts

So, should Canadian investors consider holding Evermore Retirement ETFs thereby simplifying their investment strategy?

Well, first I think it’s awesome to see new and innovative investment products in Canada. Best of all, the low management fee means more Canadians will benefit and take advantage of the power of compound interest. Canadians can compound their investment portfolio rather than pay extra fees each year. Having more simplified and cheaper investment products available to Canadians is a good thing and I applaud Evermore for doing that.

It is certainly easier to be a DIY investor in Canada now than 10 or 15 years ago. There are so many great low cost ETFs available that can be purchased easily with discount brokers like Questrade, National Bank Direct Brokerage, or WealthSimple.

If you’re already holding all-in-one ETFs in your investment portfolio, should you consider switching to one of these Evermore Retirement ETFs and further simplify your investment portfolio?

Well, that depends on what kind of investor you are.

For example, we currently hold XEQT for both children’s RESPs. The current plan is to shift to a 50% XEQT and 50% XGRO mix once they are between 15 to 17 years of age. We will shift to 100% XGRO when they are 18 years old or older. To change the mix, we plan to buy XGRO with the new RESP contributions as well as sell XEQT shares and use the proceeds to buy XGRO.

Similarly, if you are holding VGRO and want to increase your bond exposure as you get older, you can choose to either sell all VGRO shares and invest in VBAL instead or sell a portion of VGRO shares and use the proceeds to buy VBAL shares.

If you are comfortable with adjusting and rebalancing your portfolio over time by yourself, it will be more cost-effective to hold the all-in-one ETFs than holding one of the Evermore retirement ETFs.

Furthermore, I’m not 100% sure if I agree with the equities to bonds mix at the different time slots on Evermore’s retirement glide path. As I alluded to earlier, if my retirement timeline is in 2060, and given a retirement age of 65 years old, that would mean I am 27 years old this year. If I were 27 years old, I would not be allocating 5% of my portfolio to bonds. I would definitely hold 100% of my portfolio in stocks.

If my retirement timeline is 2050, meaning I am 37 years old in 2022, I would also be allocating 100% of my retirement portfolio to stocks. If it were me, given the current low interest rates environment, I would not even consider investing in bonds until at least 45 or even possibly later (i.e. only hold bonds with the 2025, 2030, 2035, and 2040 retirement ETFs).

However, please do keep in mind that my risk tolerance is very different than other Canadians, especially considering most of our investment portfolio consists of individual dividend stocks rather than passive index ETFs.

Also, because we are also more total return focused and volatility doesn’t worry us too much, we are comfortable staying more or less 100% in equities in our 40’s even in our early to mid 50’s. So, if you are more risk averse, the glide path that Evermore uses might be more suitable for you.

Now, if you currently hold one of the high fee target date mutual funds, I’d highly recommend switching to one of the Evermore retirement ETFs as soon as possible to save you a lot of extra fees over time.

If you are an investor that’s not comfortable with adjusting the asset mix and rebalancing your portfolio yourself and prefer a semi hands-off approach to your retirement portfolio, then these retirement ETFs might be a great choice for you.

Remember, since these Evermore Retirement ETFs are still very new, the asset under management (AUM) is only $1M CAD for each ETF. This is quite low in the ETF world. But I’m convinced that these Evermore Retirement ETFs are very attractive to some Canadian investors, so I believe the AUM will definitely increase over time.

Dear readers, what do you think about my Evermore Retirement ETF review? Are you considering investing in one?

If you’d like further readings, check out my Q&A interview with the Evermore executive team.

The low AUM seems scary to me. This is because things with little to no track record, or things with no track record where they prove that they can provide good returns with scale seems like it could be a wildcard in terms of analyzing its returns.

I sure like this discussion after the articles.

If you look at the original concept that Bob has, is to have the dividends earn what he earns and more. Why would a person change this proven track record of growth? He shows the excel sheet that this is a fact and not a guesstimate. I suggest friends to read his articles because he has clearly proven that over a period of time his dividend growth is improving to the point he can “choose” when to retire. You want the money to replace your income. As I deregister RRSP’s I save a percentage of cash for years that a market could dip and have an option to spend some or buy more blue chips as the market cycles. My portfolio is solid blue chips, with a focus on dividends, no mutual funds and a few ETFs.

I would like to know more from James V (directly if he allowed) regarding wintering in the Philippines. Bob has also made this point clear, it is very important “how much you spend” not just save. I winter in Maui and would love somewhere cheaper near water. But I don’t like long plane rides.

Hi Paul,

The whole premise of the post isn’t about changing our dividend growth strategy and starting buying these Evermore Retirement ETFs. It’s more about people that are utilizing mutual funds and ETFs today and whether it makes sense for them to switch to these new products or not. 🙂

I heartily agree with James V, James R and ID: This post is a good summary of a new Canadian financial product and I agree that it is better to invest into stocks directly at higher proportion if we are hands-on investors with higher tolerance for risk AND longer investment time window ☺

Thank you for a great review Bob!

You’re welcome. I may have a chance to talk to Evermore CEO and CIO more about these funds in the upcoming weeks and get more understanding about the slide path and why logic behind the current set up.

Gereat news Bob, Ask them about why no Div funds with 5-20% cover calls , to increase the Div ? Retired people or semi retired look for these funds and they have cash to burn ! . How did they get the super low MER’s ? The funds they operate have established funds underlying them – why ? Funds of funds gets crowed at times . Also, are they confident they will beat Fortis, RY ,TD or BCE in 10 or 15 years (with their cap increase and Div included) in raw stock against a fund of funds ? I would be VERY impressed if they could do it . Ask them where do all the Div’s go they collect and how are they used . If you minus the Divs some of these funds collect , and add the Cap Gain … some don’t do well at all over 10-15 years . Too early to tell if this is “a cheap way to loose money or not” . I like the competition though and the low MER’s ! 🙂 James V

As I was reading I was thinking this is the first time I don’t agree with Bob.

I never discourage anyone for investing. But the turtle wins, slow and steady. A person could just invest monthly into three large market based ETF’s. I like XIU. But my point is steady investment will earn 10% with a ten year average. Why would you change that towards the end of the game, leave it alone. I would switch from reinvesting my dividends to have what I need as income and let the pot grow another 25+ years. Live off the dividends as income.

Although I am assuming the pot of money has compounded to more than what you require. If you are growing it to have just enough than I suggest you keep working to avoid the risk. People are amazed at how little you need in retirement.

Hi Paul,

Nothing wrong with having disagreements. 🙂

Like I said in the article, the Evermore Retirement ETFs aren’t for everyone. They are built for certain investors.

Furthermore Paul here is a option; I elect to spend roughly 1/2 the year back in the philipines at my house there. Other than my fixed costs in Canada at my house here… I enjoy a MUCH cheaper Semi-retirement splitting locations and get a vacation thrown in too (all I need is the internet and zoom to do most of my work really…) . Great diving. motorcycle rides, and jungle trexking and a wonderful hospitable traditional culture – So refreshing! . Living costs are 30-45% that of Canada’s . Many expats are showing up of course these days from around the world ,but Canadians are slow to learn that they have options in semi retirement or retirement other than the USA , to reduce their cost even further, while still enjoying hyper-fun and enjoyment and tropical breezes . Florida, Arizona, Texas, is OK I guess- I like it there, but expensive, northern Luzon, Negros, Palawan , and such is even better, given the price, fun, tropical warmth and savings over Canada. A cultural treat too and smiles like you have never seen before ! 🙂 . Just an option …for most ! Some even can retire sooner than expected if they choose living in like jurisdictions, et al , for half the year! Good health and happy Investing gang ! James V

Keep it simple. Life expantancy is 85 for someone approaching 60. That’s 25 years to finance. Reduce equity coverage by 20% every 5 years. Age 60 XEQT. Age 65 XGRO. AGE 70 XBAL. ETC ETC

That makes sense if you’re OK managing and rebalancing yourself. 🙂

Thanks for your well written review , as always. Well done thank-you .

I am a little ‘cool’ on Evermore funds , in that they are new with little track record to calculate from, and certainly don’t trade much ( low volumes) – so getting in/out may be problematic of sorts. I must agree with you, seeing some new products in the Canadian marketplace with lower management expense ratios is nice to see. I think Canada has the highest mutual fund and an ETF management expense ratios in the G-7 , terrible!… Simply because, Canadians are willing to pay it. Again, chronic need for finance education at the primary school level. As an investor semi-retired, I look for Cap Growth, with a dividend yield that grows as well over time. So for me, these funds don’t interest me in their philosophical approach (pre retirement). However to two issues stand out immediately is the lack of track record and the low volumes. It’s basically a fund of funds …. Which I’m not really keen on as well. They act more or less as a middleman , being a fund of funds type product. Happy Investing Crew ! …. James V

We will have to wait and see how Evermore does. Having more and new products in the Canadian marketplace with lower MER is always a good thing. We definitely need more financial education for Canadians old & young.

I think my challenge with this approach is that the “glide path” flattens out roughly 5 years into retirement, where I hope to be able to live another 25 – 35 years.

It’s way too conservative for me. Today I think I’ll be okay with 100% dividend paying blue chips in retirement, but we’ll see. However, I can’t see myself ever reducing to 50% equities. I would have to save considerably more for retirement. I’d rather risk having to lower my standard of living with more years of “retirement” than require more years of full time work to lower my risk level.

There’s no limitation quite like time.

Agree that it’s a bit too conservative for my taste as well, especially considering the low interest rates. Seems to make sense to flatten it out maybe 10 or 15 years post retirement.

For sure, that kind of makes sense to me also.

I honestly thought that your review was very thorough and “all encompassing” especially given the recent arrival of the Evermore ETFs .

Thank you for your analysis and terminology used to explain your analysis as it was very clear, organized and understandable.

Thank you ID. Glad to hear this is easy to understand.