In recent years, there are more and more new and innovative investment products available to Canadians. These new products, mostly in the form of ETFs, typically have low management fees and provide excellent sector and/or geographical diversification. For example, the all-in-one ETFs and the all-equity ETFs from the likes of iShares, Vanguard, and Horizons have allowed Canadians to manage their own investment without needing to manually re-balance regularly.

However, it is easy to see that most of these ETFs are not built specifically for retirement as they either track a specific index or have a set mix of equities and bonds. Although there have been target date mutual funds available for years, they are extremely costly. Fortunately, earlier this year, the team at Evermore launched a set of low fee target date ETFs to make investing for retirement easier.

Some of you may recall that I reviewed these Evermore Retirement ETFs recently. Overall, I was very happy to see such new and innovative products in Canada. While these Evermore Retirement ETFs aren’t necessarily the right fit for me and Mrs. T, I think they can be excellent investment products for investors that are not comfortable with adjusting the asset mix and rebalancing their portfolio regularly.

I truly believe the Evermore Retirement ETFs are a game-changer in the Canadian investment space and they are great for those investors that prefer a semi hand-off approach to their retirement portfolios.

After publishing my review, Greg White, CMO & Co-Founder of Evermore, reached out to me wondering if I’d like to chat with him and Evermore’s CEO & Co-Founder Myron Genyk and CIO Brian See to learn more about these retirement ETFs and answer questions.

I was not going to pass on such an excellent opportunity to pick on their brains. After a 30-minute video call with Myron, Brian and Greg, to talk and go through my questions, they agreed to extend the session in the form of a written Q&A.

Please note, I have no association with Evermore. I did not receive any compensation for this article or the review. My goal for the Q&A is to provide as much info as possible to Canadian investors while answer some of the questions the readers and I had about the Evermore Retirement ETFs.

Evermore Retirement ETFs – Q&A with the Evermore Team

Q1. First of all, Myron, Brian and Greg, thank you very much for taking the time for this interview and answering questions about the Evermore Retirement ETFs. Could you do a quick intro and tell readers about yourself?

Myron: I am a Co-Founder and CEO at Evermore. I’ve been working in and with ETFs for a while, since 2007, in different capacities. Most notably, on the derivatives desk at National Bank, and then at BlackRock Canada in a capital markets role. The maturation of the ETF industry has been quite something to witness and experience, and I’m really excited to be driving of further innovation in the space.

Brian: I’m the CIO of Evermore and joined the company in late ‘21. I have over 15 years of finance and investment experience and was with CIBC Asset Management for 7.5 years managing various portfolios. Before that, I was with the OMERS pension plan working on various investment mandates. I also spent some time on the sellside in equity research and in a family office along with industry roles within energy and logistics.

Greg: I am a co-founder and the Chief Marketing Officer at Evermore. Right before launching Evermore I was running my own creative agency focused on the financial services sector. Although my focus has been in marketing for a while now, I started my career on the wealth management side over 20 years ago and I am also a CFA charter holder.

Q2. Wow, there’s a lot of investment knowledge between the three of you. We’ll get right into it. Could you explain the reason behind picking funds from different ETF companies like iShares, Vanguard, and BMO?

Brian: Because we are an independent fund manager, unaffiliated with any ETF provider, we were able to consider the entire ETF universe, giving us the freedom to find the best underlying funds for our retirement ETFs. For practical reasons, we focused on Canadian and U.S. listed ETFs. There were 3 considerations:

- 1) The products had to be low fee from a total cost basis. This meant not simply picking low MER ETFs, but also considering the layers of withholding taxes. For example, some products may have low MERs, but you end up paying a lot more in withholding tax.

- 2) The ETFs needed to have excellent liquidity – meaning not just large volumes but narrow bid-ask spreads, which would translate to tighter bid-ask spreads for our Evermore ETFs.

- 3) Finally, the ETFs needed to have a long history and track record versus using new ETFs with a more limited record.

We didn’t set out to choose funds from iShares, BMO, or Vanguard. But given their long records of offering low-fee index-based ETFs, it was perhaps obvious in hindsight that we might choose funds from their suites.

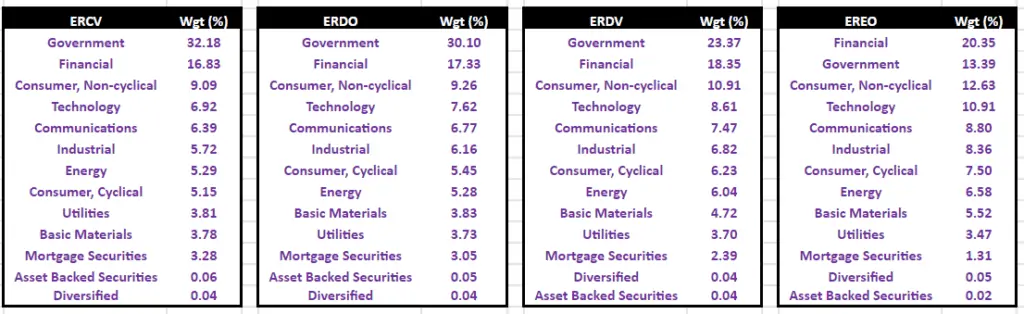

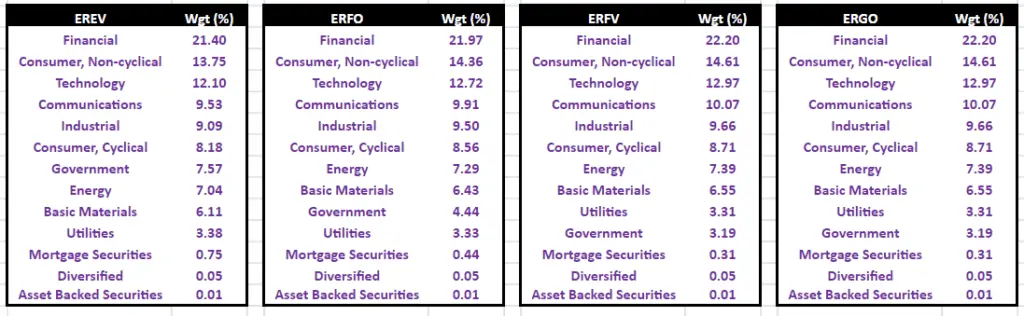

Q3. There is some great information on the Evermore website. However, I noticed that the sector breakdown for each fund is missing. Given these are retirement ETFs, it’s certainly a good idea to make sure you’re sector diversified. Could you let us know if you plan to provide such information? What’s the sector breakdown for these funds like right now?

Greg: The website will be updated with sector weights on a monthly basis starting with the April 30th effective date. As of March 31st, the sector weights were

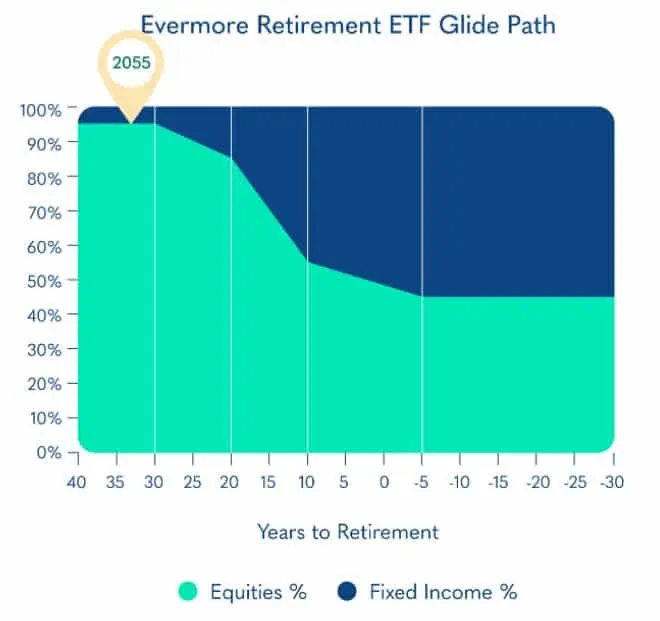

Q4. Let’s get to the most important question – glide path. Why hold so much bonds in the retirement ETFs? For example, the Retirement 2060 ETF holds 5% in bonds. Wouldn’t it be better to hold 100% in equities to capture as much potential growth as possible, given that the investment timeline is more than 35 years?

Furthermore, given the current low interest rate environment, why is the retirement fund capped at 45% equities and 55% bonds post retirement?

Myron: These are really important and interesting questions, so let’s slowly unpack these.

First, let’s define what we are trying to achieve here. We wanted to create an easy, one-ticket solution for retirement funding. Something so that, if someone saved a reasonable amount of their earnings over a career spanning approximately 40 years, they would have enough to sustain a comfortable retirement lasting approximately 30 years. Something that minimized the odds of people outliving their nest egg.

For decades, academic and industry studies have shown that asset allocation has the greatest impact on returns. More recently, academics have been exploring investor biases and behaviour and their impact on returns; here, risks include investors selling during bear markets, or investors being generally underinvested in the markets, or the paradox of choice, and so on, as well as the ways in which investment products can be structured to mitigate these undesirable investor tendencies.

It is against this backdrop that we approached our portfolio construction. Broadly, this consisted of three steps, which were performed more recursively than sequentially. First, we selected our asset classes, landing on broad equity ETFs and broad bond ETFs. Next, we determined the geographical allocations for each of these two asset classes. Finally, we determined the glide path, which is the allocation between these two asset classes over time.

The first step, how we selected these two asset classes and rejected others, was fascinating work, and we plan to publish a white paper describing our process and outlining our results.

The second step, setting the geographical allocations, can be more easily explained: for each asset class, we determined which geographic allocations landed on the efficient frontier; for equities, we chose the efficient portfolio with the best Sharpe ratio, and for bonds, we chose the efficient portfolio most negatively correlated with the optimal equity portfolio. Now this is simplifying a bit, but that was the general idea.

Bob, your questions mostly concern step three, how we determined our glide path, the relative weights of stocks and bonds at different points in time. We plan to fully discuss our methodology in that future white paper; in the meantime, here is a very high-level overview of that process:

- Set the most reasonable market assumptions: expected returns, volatilities, correlations, inflation rate, etc.

- Set the most reasonable investor assumptions: number of years working and then in retirement, the real salary growth rate, the savings rate and the replacement rate, etc.

- Create a universe of several thousand possible glide paths.

- Run a Monte Carlo simulation (10,000 loops) for these assumptions across all glide paths. Note which types of glide paths minimized the odds of an investor outliving their nest egg.

- Repeat Monte Carlo simulation, for different market assumptions and/or different investor assumptions.

- Repeat Monte Carlo simulation, again with new assumptions, again noting which glide paths were more successful. And repeat. And repeat. And repeat.

We repeated this process across several dozen sets of assumptions. Just a few of the possible changes we made included:

- Increasing the correlation between stocks and bonds. In the extreme, a high correlation between stocks and bonds made almost any glide path less desirable.

- Gradually increasing a retiree’s replacement ratio. (Replacement ratio refers to what percentage of their final year’s salary does someone want/need to finance their desired lifestyle in retirement. In Canada, this is approximately 50%; in the U.S., this is approximately 70%, with health care costs making up most of the difference.)

- Forcing a bear market of at least –20% for two years right at the beginning of the investor’s retirement, and maybe another bear market 10 years in, to consider “sequence risk”.

- Bumping up spending one year early in retirement, to simulate an emergency use of funds.

At this point, we had a pretty good understanding of which glide paths might perform better under various conditions. And we also had a list of possible glide paths that minimized longevity risk similarly well across a range of reasonable assumptions.

At the beginning of this answer, I mentioned behaviour biases, and what may cause investors to act in sub-optimal ways. And so, when we were running all these Monte Carlo simulations, we not only tracked the distribution of terminal wealth (including the proportion when this was zero, indicating an instance when someone ran out of money), but we also tracked statistics like the Sharpe ratio, the Sortino ratio, and the maximum drawdown. More research can help us understand the circumstances and the extent these statistics impact the tendency for investors to “stay the course”; until that work is done, it is admittedly difficult to quantify their utility in maximizing the best outcome for the investor.

While these behaviour-stabilizing metrics weren’t used as tie-breakers per se, they did factor into the discussion when choosing the best glide path out of our now smaller set of possibilities. More granular Monte Carlo simulations (100,000 loops) were also used to choose from the smaller set of generally good glide paths.

And so, this is the process that was used to determine the glide path for our Evermore Retirement ETFs. We started with the universe of possible glide paths, then reduced that to a smaller set of possible glide paths focusing strictly on longevity risk, and then ultimately chose our glide path by combining minimizing longevity risk while considering metrics that might cause investors to panic and cash out too soon.

Brian: And specifically, to your questions:

- Across many sets of assumptions, the initial asset allocation of 100/0 and 95/5 had statistically similar knock-out probabilities. While the mean terminal wealth was higher using 100/0 rather than 95/5, the path to get there was also more volatile and higher volatility may lead to an investor cashing out too soon. We took the view that, since “you can’t take it with you”, and dying penniless is an awful outcome (though this is avoidable by reducing spending in retirement), the 95/5 allocation was a preferable starting point.

- Bonds have experienced yields below historic averages in recent years, particularly since the Great Financial Crisis. It’s now April 2022, and with rates increasing substantially over the past few months, we might be witnessing a renormalization of bond yields. While we ran simulations using a variety of bond yield assumptions, our base case is only slightly higher than where yields are right now. As an aside, our terminal equity allocation of 45% is higher than that for the larger target date funds in Canada and in the U.S.

Again, investors are generally acting in their best interests if they “stay the course”. Really good advisors help their clients do just that. For the portion of an investor’s portfolio dedicated to investing for and then funding their retirement, we wanted to create a glide path that not only helped nudge investors to stay the course, but rewarded them for doing so, too.

Q5. Some readers asked, why not focus more on dividend stocks and use dividends as a way to protect your equity portion instead of holding a large percentage of bonds. Could you explain why the Evermore Retirement ETFs do not focus on dividend paying stocks or ETFs?

Myron: I definitely see the appeal of a dividend stock approach to investing. You usually get to see your cash flows increasing every quarter, every year. It can be an extremely satisfying and rewarding approach. But, with the goal of investing for and then funding retirement, there are a few reasons why we went with broad index ETFs rather than dividend ETFs.

Before getting those reasons, a quick thought on owning dividend stocks versus dividend ETFs. Holding dividend stocks requires almost as much mental capital as it does financial capital. Not everyone can do this.

To do it right, you should monitor each company ensuring it has adequate financial ratios and can be expected to continue or even increase its dividend payout, know what to do if a company begins to perform extremely poorly and have the discipline to execute on that plan, understand how to avoid yield traps, and so on.

Some people really enjoy doing this work, and that’s great. But for most people, especially those who lack the time or passion to closely track their portfolio, a portfolio of dividend stocks can lead to poor results and disappointment.

For these reasons, if someone wants exposure to dividend stocks, buying a dividend ETF and paying the MER might be worth freeing up their time, relieving them of the work and stress of portfolio management, and helping them stay the course.

This same reasoning can apply to owning one ETF that owns a portfolio of ETFs, rather than holding a portfolio of ETFs directly. As of April 2022, there is approximately $19B in multi-asset ETFs, up from nearly zero just five years ago. Clearly, there is a segment of investors who see the benefit of outsourcing asset allocation and security selection.

Now, as for why we chose index ETFs over dividend ETFs, there are five reasons:

First, industry concentration: Canadian dividend stocks tend to be concentrated in financials, energies, utilities, and telecoms. From a risk-return standpoint, being diversified across all sectors is usually the better long-term play.

Second, investors with registered accounts are agnostic to the characterization of returns. Canadians are incentivized to save for their retirement in their RRSP (or LIRA) or TFSA. All things being equal, Canadian dividend funds generally see more of their returns taxed as eligible dividends rather than broad Canadian index funds, which would see more capital gains. While a non-registered investor may wish to consider the characterization of their returns to minimize taxes, a registered investor (RRSPs, LIRAs, RRIFs) pays no tax until they de-register their savings by moving them into a non-registered account, with those withdrawals then taxed as income. And earnings within a TFSA and then subsequent withdrawals are not taxed at all. Registered investors (and investors using a TFSA) should be indifferent between earning a dollar of dividends and a dollar of capital gains.

Third, total return matters. Over most meaningful time periods, index ETFs have outperformed dividend ETFs on a total return basis. There are probably a few persistent drivers for this phenomenon. One relates to how different types of returns are taxed, as discussed in the previous point; because dividends are generally taxed more favourably, one might expect index ETFs and dividend ETFs to experience similar after-tax total returns, but this would imply that index ETFs would tend to outperform on a pre-tax basis. This is just a hunch; I’d be really interested to know if anyone in your community can point to any research on this. Another possible driver is demographic and behavioural; older and wealthier investors who may prefer for dividend stocks would be willing to pay a premium for that perceived stability and security, which could lead low- and non-dividend stocks to trade at a discount, which could lead to more attractive total returns as they mature in the long-run. Again, this is just a hypothesis; I’d love to know if someone has researched this.

Fourth, some dividend ETFs offer extraordinarily attractive yields by doing more than just investing in dividend stocks, with consequences to their total return or risk-return characteristics that are less obvious. Some ETFs boost their distributions with “return of capital” (or ROC), which is simply returning the investor’s money to them; other ETFs sell call options and distribute the premium received, limiting the fund’s future upside; other ETFs use moderate amounts of leverage, enhancing distributions and any upside, while also enhancing the downside. And while these three types of ETFs could be interesting investments, because of their unique risk-return and total return characteristics, we determined index ETFs would provide investors the best chance of enjoying their expected retirement lifestyle.

And fifth, dividend ETFs tend to be more correlated than index ETFs to bond ETFs. To minimize overall portfolio volatility, improve risk-return metrics, and help ensure that investors don’t outlive their savings, it is preferable to pair the bond component with an equity component that is less correlated, ideally negatively correlated. That’s another reason why we chose to use index ETFs rather than dividend ETFs.

Listen, I love dividends. Seeing those cash flows hit your account, it’s like earning another salary, without the commuting, deadlines, or responsibilities. In fact, I primarily hold two dividend ETFs in my non-registered account. However, for the goal of retirement investing specifically, for the reasons I stated above, I think using index ETFs is the way to go.

Q6. I think these retirement ETFs are great. Should we consider using them for RESP?

Greg: The Evermore Retirement ETFs have been built specifically for the goal of investing for, and supplementing your income during, retirement. When we think about investing strategies, we always put the goal first; that’s what goal-based investing is all about. The goal of saving for your child’s education in an RESP should be approached differently from your investing strategy for retirement.

With education investing, if you are starting when your child is born, those first ten years or so are where you have the most runway for growth via the equity markets. But as you approach the time when your child is about to start post-secondary school, parents probably want to shift whatever they have saved into more guaranteed return investments. The goal here is to pay for education, covering as much of the tuition and living expenses as possible. You wouldn’t want that first tuition payment to coincide with a bear market while being too exposed to equities.

Q7. Some readers are worried about Evermore being a new company and the low asset under management (AUM). Why should investors use Evermore products rather than just buying the standard ETFs from the likes of Vanguard and iShares?

Myron: When people discuss low AUMs or trading volumes, they usually use these metrics as proxies for liquidity. Liquidity can be defined as how easily, quickly, and cost-effectively something can be bought or sold. In fairness, AUM and volume can be good indicators of liquidity. I think a much better indicator is the bid-ask spread, and how much depth there is – that is, the bid size and the ask size. This directly represents the cost of getting into or out of a position.

Evermore’s ETFs tend to trade 1 or 2 pennies wide, with about $100k per side. And when an investor buys at the offer price, the amount that was shown is generally “refreshed” by the market makers – ETF trading desks at the large banks (for Evermore, that’s TD and National Bank) – meaning that even during periods of heavy trading, one can expect there to be the size on the bid or offer. And there is a good reason for this: the underlying holdings are extremely liquid, and trade with very tight bid-ask spreads, too. Generally, except for about a dozen or so older ETFs that have exceptional two-way trading volume, an ETF is only as liquid as its underlying securities.

Q8. Finally, are you and your family members currently holding Evermore Retirement ETFs? If so, which one(s) are you holding?

Greg: My wife and I are split between the 2045s and the 2050s. I’ll be 71 in 2045, and since I don’t see myself looking to fully retire until my seventies, it was the most appropriate choice for me.

Brian: Between my wife and I, we hold the 2045s and 2050s across our RRSP and LIRA accounts as we plan on retiring in that timeframe. My parents are in the 2025 ETF given they are essentially retired.

Myron: I feel like you are asking me my age! And in a way, I suppose you are! I hold the 2045s in my RRSP and LIRA, and my wife holds the 2050s in hers.

Tawcan: Oops did I indirectly just ask about their ages? That wasn’t my intention ha!

Wrapping up – Evermore Retirement ETFs

Thanks to Myron, Brian and Greg for taking the time to answer these questions, I really appreciate it. You have shared some excellent points for me and my readers to consider.

There isn’t a one size fits all solution when it comes to investing for retirement because we all have different retirement and life goals. For example, some want to die with zero while some want to pass on an inheritance to future generations. This is why while the Evermore Retirement ETFs may not be suitable for Mrs. T and me, they may be excellent products for other investors.

When it comes to investing for retirement and investing in general, my best advice is to do your own homework. Don’t blindly rely entirely on someone else to manage your hard-earned money. You should have the best interest for your own money, not someone else. Take charge!

I have had good luck with Harvest ETF’s , buying them on market dips and using them as a sleeve for income . Great way to get International exposure , if done right . About 10% of my holdings are ETF’s from Harvest, CI and BMO mostly … but I will only buy them on dips – locking in a high yield and low price ensures me Capital Gains on the unit price. HDIF is one that i’m tracking that is new – so looking for some dips under NAV , also may make another Purchase on TXF ( NASDAQ Tech Giants ) at about 16.00 , if the the market dips some more and Tech struggles in the interim. Anyway , just my look at ETFS . The Dems in the USA have shifted to Macro economics of the country into dangerous uncharted territory , so I’m being very cautious with their mismanagement of their economy. Id the USA catches a cold , we will surely catch the Flu in Canada – economics wise ( Ironically ,thank gosh for Oil/Nat Gas saving the market in Canada for the interim).

I see good articles.

‘Don’t blindly depend entirely on others to manage your hard-earned money’

I really like it

Thank you Kim.