As you may know, we only invest with money that we have. We don’t borrow to invest, meaning we are not utilizing Smith Maneuver or trading on margin. Why don’t I invest using margin?

Very simple. Because I have seen firsthand how badly one can get burned when trading on margin.

Back in the late 90’s and early 2000’s, a few of our family friends were aggressively buying dot-com stocks. These stocks were doubling or tripling very quickly. Making money was easy. blinded by greed, they started borrowing money from their brokers to buy high risk, high reward dot-com stocks.

The idea is simple. Instead of buying $5,000 worth of stock using your own money, you only pay half and borrow half. Your stock broker then charges interest for lending you the $2,500 and expects the principal to be paid later. Trading using margin allows for multiplied rate of return. Instead of getting 50% return on an investment, you would get 100% return.

The cost involved for trading on margin

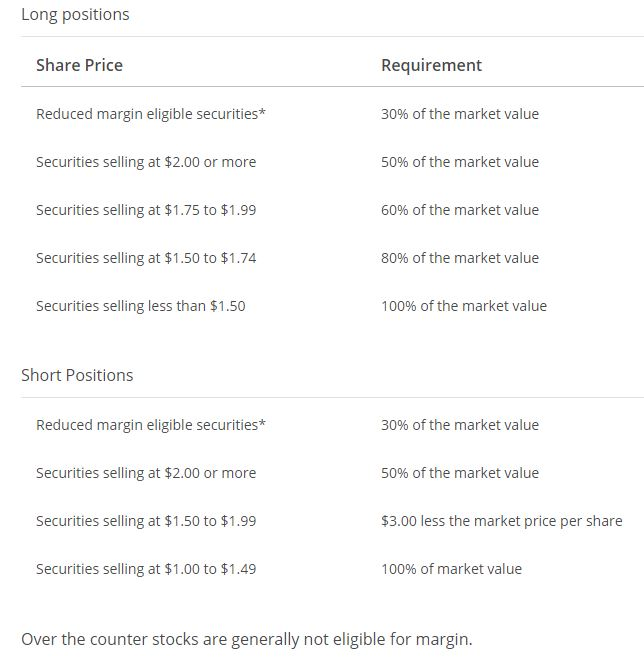

If you are trading with Questrade, Questrade sets a margin requirement. The margin requirement is the minimum amount of maintenance excess you must have in your account in order to enter a position, or a percent of the current market value.

If you are trading blue-chip dividend stocks, the margin requirement would be 50% of the market value. Meaning you can borrow up to 50%. If are you trading penny stocks, the margin requirement is significantly higher.

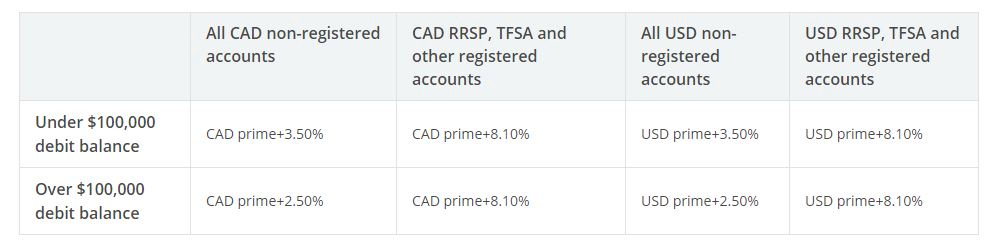

To make money, Questrade charges interest for lending you the money. The interest rates are different depending which type of account you are trading with and the size of your portfolio.

Currently the CAD prime is 2.95%. So trading margin using a CAD non-registered account with less than $100k would cost you 6.45% of interest rate.

Dangers of trading on margin

The good thing about trading margin is that you can significantly increase your rate of return. You can also deduct the interest rate in your income tax filing.

Our family friends that used margin were making money hand over fist when stock prices were going up. But when the dot-com bubble finally burst and stock prices were falling, they lost big time.

When you purchase a stock fully with your own money, you can decide when to sell. When trading on margin, however, you have less control of your investment. You have contractual obligations with the broker. When the stock price starts to go down, you are either required to deposit additional funds into your account to to meet the maintenance requirements, or forced to sell your securities. If you don’t take these actions, the broker will liquidate your position for you to protect themselves.

This is very scary during a bear market and stock prices are gapping down. Often the stock broker will simply liquidate your positions before you can take any actions, and you end up with a huge loss.

These family friends that traded on margin during the dot-com bubble lost more money than they made during the dot-com bubble burst.

It was unpleasant. Getting stuck in this kind of mess created a lot of tensions, some marriages fell apart as a result.

Growing up, I took these lessons to heart and learned to stay on the more conservative side when it comes to investing. Hence, I don’t invest using margin and do not plan to ever use it. If I gamble on an investment, I only invest with money I can afford to lose, and I limit my exposure to this particular investment.

Dear readers, do you invest using margin? If so, what’s your experience so far? If not, why not? I would love to hear from you.

Your conclusion is correct but one of your premises is wrong: margin vs. HELOC are two separate things.

You can absolutely get margin-called. But you will likely never get called to pay your HELOC as long as you don’t have a mortgage to renew and as long as you’re making interest payments.

I just thought it is important to differentiate these two products.

Like you, I’d never borrow from margin. Too risky for minimal gain.

What do you think of the stock HNHPF, Hon Hai Precision in Taiwan? I’ve heard great things about it.

Sorry I’m not familiar with this stock.

Interesting. I trade with Questrade, and their accounts by default are margin accounts. I wonder if it’s possible to remove the ability to trade on margin and only trade with money you have in your account. I was just thinking that I’d rather trade using my own money only.

Yes taxable accounts at Questrade are default as margin accounts. We only trade with money that we have in the account.

I’ve invested on margin before, and it didn’t end well in the stock market. Too inexperienced, too emotional.

But I did go on $1,000,000 margin when I bought my 3rd property in SF (cost $1.24M) in 2014. That turned out well, so I decided to sell another property just to get my exposure back down again.

PRices are nuts now. I wonder when things will cool.

Sam

Exactly I feel that one would get too emotional when trading on margin. Yes I wonder when SF real estate would cool. I always get amazed how expensive houses are in by Facebook and Apple.

I have run a Heloc for several years for a non-registered investment account. As long as the dividends are paying the interest on the HELOC AND paying down some of the principal every month I am happy For eight months this year I have paid $962.65 in interest and pulled $4.337.20 in dividends. naturally the dividends less interest are taxable but at a lower rate.

I have run as high as $160K margin but I am now down to $29K with a portfolio value of $69,970 so I have a $40K safety pad in there for a pull back. As I am now retired I will be zeroing the HELOC by selling some stocks and transferring the remaining stocks to another non-registered investment account. That will be drawn down so I do not have to utilize my RRSP’s for several years.

And I will consider re-entering the HELOC for investment if circumstances are right for me.

RICARDO

@ Bob, small percentage of investors even know what “margin” is, those that do it are few & generally aggressive investors, while others go the ETF’s & be done with it or invest using a robo-investor company

margin or leverage, are these the same thing?

is it possible to margin & always get a guaranteed positive return?

would you buy a 5% dividend blue chip (a Bank) on margin, then sell a LEAP deep in the money to get downside protection as well as increasing the dividend rate?

or maybe use margin where the current IB brokerage margin rage in Canada is 2.25%, then invest in a HISA paying 2.5% or a 5 year GIC 2.75%

Or keep investing without margin in a volatile market in dividend paying stocks (buy & hold) cross your fingers.

So many variables or ways to invest with or without margin – different strokes for different folks

I think there is no silver bullet answer here, because risks – and risk appetite differ a lot among individuals. Minor to moderate leverage is IMHO totally acceptable if used appropriately. With 1 % interest rate, investing e.g. in blue chips yielding 3-4 % might not be a bad idea. At least I do it. But on the other hand, I’m able to pay off (if necessary) the principal in a decent time period using dividends only (and even more rapidly if other income sources are utilized), so I would say the risk in my case is “manageable”.

I’ve never invested with margin and likewise have not intention to. The possibility of owing someone money following a loss does my head in. An interesting thing to me is how many people are uncomfortable investing in stocks on margin, but we essentially do the same thing buying our homes (a highly undiversified, leveraged asset).

There’s a wide range of possibilities to investing in margin. It doesn’t mean you have to spend 6.5%+ interest on dot-com bubble stocks with zero earnings burning billions a year hoping to turn it around. What about going to interactive brokers, pay 2.5% interest with a net tax deduction cost closer to 1.5% and buying a company like ATT? Just food for thought. I agree in the statement that I would never pay 6.5% to borrow money to buy companies with negative earnings and burning cash at an alarming rate.

Not urging that there are brokers that charge lower interest rate. But what’d happen when interest rate starts going up?

When I hear about investing on margin, I think of the way people invested prior to the start of the Great Depression in 1929. I have never done it. I honestly cannot even recall reading about anyone who has invested that way in many years. I am more of an investor than a speculator.

There are lots of differences between investor and speculator. I guess some may consider trading on margin is one of the points for being a speculator.

I’ve never done any investing on margin despite having a “margin” account at the brokerage.

Investing with debt is a pretty risky move to make, not something I would consider “normal”. Any investment like that would need to have a nearly 100% certainty of return to be a real investment. Otherwise it’s just be speculation — straight up gambling.

I’m not much of a gambler either.

We have a few “margin” accounts but we don’t use it. Too risky. 🙂

Dear Bob,

Sorry to hear about your family’s losses, not only the financial ones.

I do not purchase anything that I can’t afford outright (with the past exclusion of a mortgage and perhaps my health if required in the future).

Besos Sarah.

It’s not my family, family friends… big difference. 🙂

There was a time when I was thinking hard about trading on margin.

Robinhood introduced Robinhood Gold for $10 per month and don’t charge any interest for borrowing. They wanted to keep things simple.

Seemed like a great idea!

Not having to pay interest is a bonus because it doesn’t eat into returns.

However, those margin calls put me on edge. The dot-com crash is a great example, especially with the high values the market is trading at right now.

Decided to stick with the money I can afford to lose.

Wouldn’t the $10 per month “usage fee” be considered as interest though?

It could.

With the other benefits you get from from their Gold plan, plus free trades, I wouldn’t necessarily consider the whole monthly fee as “interest.”

I’m with you, I do not invest on margin. I am happy to invest in index funds, but on margin is beyond my risk tolerance (especially now that I am married and have a son…). I’d rather be able to weather a market downturn without losing my shirt and everything else.

Exactly, weather a market downturn without losing your shirt and everything is pretty important.

Argon is dangerous, fill stop!

Yet, I use it while trading options. I have approx 1,6 margin. That means for each 100 USD at risk ( the strike of a put) I have approx 65 USD. Dangerous? Yes and also manageable. It would mean all my options would need assignment at the same time. This is possible. I manage this by adding puts on gold silver and other save heavens.

Time will tell.

I don’t know enough about options to decide whether that’s riskier than buying stocks on margin. I suppose if you’re shorting then it’s a bit more dangerous?

I agree with you that investing on margin is dangerous, and could lead to bad consequences. If you were to do it however, do it at a place like Interactive Brokers where interest rates are much lower.

On the other hand, some claim that if you buy stocks but have a mortgage, you are essentially investing on margin. Thoughts?

I think both cases you are investing using borrowed money. But margin is usually with much higher interest rate than mortgage, so using margin is more dangerous.

If you have investment and mortgage, I think the best thing to do is selling the investment and paying your mortgage, then borrow the money using heloc and buy back the investment. This way the heloc interest is tax free. I believe this is the least expensive way to invest using borrowed money. And there will be no margin calls, as long as you can pay the monthly interest of heloc.

Of course, leveraging to invest always comes with higher risk.

Yup mortgage rate is typically lower interest. 🙂

I don’t think buying stock with a mortgage is like investing on margin. Yes you have a mortgage on your house, but that’s backed up by a pretty secure asset. Now if you were to tap into your HELOC to invest, that’s a different story.