Welcome to another monthly dividend income update!

We have been doing these monthly updates since the birth of this blog (over 10 years now). We do these monthly updates to keep ourselves accountable and show that we do walk the walk and are not just all talk and no action. It is also our way to demonstrate that it is possible to build up a sizable dividend portfolio over many years with the goal of living off dividends one day.

For the most part, we keep our investment strategy relatively simple.

- We invest with money that we don’t need for at least the next five years

- We max out our TFSAs and RRSPs every single year

- We invest in non-registered accounts when our TFSAs and RRSPs are maxed out

- We invest in Canadian dividend stocks in our non-registered accounts and TFSAs

- We invest in US dividend stocks in our RRSPs

- For diversification purposes, we own index ETFs like XAW and QQQ in accounts that are tax efficient (XAW in RRSPs and non-registered, QQQ in RRSPs)

No option trading, no leveraging, and no crazy nonsense!

We believe that keeping it simple is the best investment strategy. This may or may not be true for everyone though. That’s why personal finance is personal!

September meant back to regular school programming but with a slight twist.

Last year we started homeschooling both kids. Mrs. T and I didn’t make this decision. In fact, it was the kids that wanted to be homeschooled because they both wanted to learn more than the school curriculum offered and focus on academic areas they were interested in.

After consulting with both kids in May, we collectively decided to home school again this school year. While some people may think homeschooling is completely outside the norm, for us, we believe this is just an extension of the financial independence retire early (FIRE) journey for our family.

The FI and FIRE journey is very much outside of societal norms. We are focusing on becoming financially independent in the near future so we can choose to work on things that we enjoy doing. Since we’re already on the FI/FIRE journey, homeschooling seems like just an extra step along the journey. Homeschooling simply gives us further freedom and flexibility that we are seeking in our lives.

For example, if we want to travel for an extended period of time, we can do that and kids can still do school work and learn important social skills while on the road. Some readers may recall that we aspire to travel around the world for a year or two. We also would love to live in Taiwan and Denmark for an extended period of time. Again, homeschooling enables us to one day move forward with these plans.

Homeschooling was one of the key reasons why we were able to go to Denmark in April for over 7 weeks and stop in Iceland for a week on the way back home to Vancouver (In case you’re wondering, going to Denmark in July or August would have cost us an extra $2,000, so 1-0 for homeschool).

Furthermore, just because we’re homeschooling now it doesn’t mean that we can’t change in the future. We can enroll both kids back into regular schooling if we decide to do so in the future.

September also meant the start of another Scouting year. This year, both kids “swam” up to new groups. Kid 1.0 is now in Scouts and Kid 2.0 is now in Cubs.

Last year they had meetings on different time slots, but this year they have meetings at exactly the same time. This means I’m doing the weekly Scouter rotation – attend Scouts meeting one week, then attend Cub meeting the next week. If the two meetings happen to be at the same location, the drop off & pick up logistics would be simple. But when the two groups meet at different spots, we would need to scramble around and figure out the driving plans (we’re a one car household). I also volunteered to help out with the Scout Venturer Group (ages 15 – 17) for outdoor activities and camps. I was involved in Scouts growing up and I found the program extremely valuable, and that’s why I wanted to give back.

To keep both kids physically active, we also signed them up to weekly judo classes. Both of them have been having fun with it and have been practicing pinning me down on the floor.

I also have been heading back to the office a few days a week and Mrs. T has been busy with her doula services, helping clients with prenatal care, birth care, and postpartum care. Therefore, each week Mrs. T and I would need to look at our calendars and figure out a driving plan for all the different activities.

As you can imagine, things can get very complicated pretty quickly! Fortunately, my parents are close by and can help out with some of the driving. We can also get help from neighbours and friends.

Yes, we could get another car to simplify the logistics but that meant extra expenses. If we can avoid it, we will.

The backyard garden kept us busy throughout September. We really enjoy harvesting produce from our garden and enjoying the fruits of our labour.

Like August, I went on another business trip to San Francisco and San Jose. It was good meeting some new customers, it was also nice to finally meet a co-worker in person for the first time after having worked with him for years.

To keep life even busier, I also signed myself up for a 7 session “learn to curl” boot camp. I used to curl in high school so it has been almost 25 years since I threw a stone. Although I still remember how to slide and the different techniques, I need more practice!

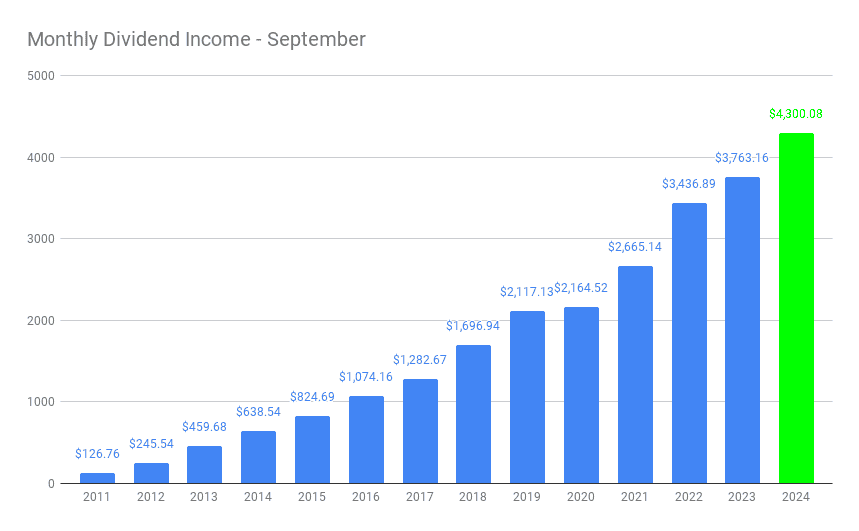

Dividend Income – September 2024

In September we received dividend pay cheques from the following companies:

- Alimentation Couche-Tard (ATD.TO)

- Brookfield Asset Management (BAM.TO)

- BlackRock (BLK)

- Brookfield Renewable Corp (BEPC.TO)

- Brookfield Corporation (BN.TO)

- Canadian National Railway (CNR.TO)

- Canadian Tire (CTC.A)

- Enbridge (ENB.TO)

- Fortis (FTS.TO)

- Alphabet (GOOGL)

- Granite REIT (GRT.UN)

- Hydro One (H.TO)

- Intact Financial (IFC.TO)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- PepsiCo (PEP)

- Qualcomm (QCOM)

- SmartCentres REIT (SRU.UN)

- Target (TGT)

- Visa (V)

- Waste Management (WMT)

- Walmart (WMT)

- Invesco NASDAQ 100 Index (QQQ)

The 23 dividend pay cheques added up to $4,300.08. Another very solid month for us in terms of dividend income. With a very busy September, it was nice to see our dividend portfolio working hard for us and generating money.

Comparing September 2023 and September 2024 dividend income, it was interesting to note that the dividend payers stayed more or less the same. We saw a YoY growth of 14.27%. Again, a very solid number considering we’re facing the law of big numbers. The dividend growth was contributed mostly by organic dividend growth and drip.

Dividend Hikes

We were fortunate to see a few dividend hikes in September.

- Emera (EMA.TO) raised its dividend payout by 1% to $0.725 per share

- Fortis (FTS.TO) raised its dividend payout by 4.2% to $0.615 per share

- VICI Properties (VICI) raised its dividend payout by 4.2% to $0.4325 per share

- McDonald’s (MCD) raised its dividend payout by 6% to $1.77 per share

These four dividend hikes increased our forward dividend income by $83.50. It’s not a lot of an increase but I’ll take an increase over no increase.

It is slightly concerning that Emera only raised the dividend payout by 1%. Does that mean the company isn’t doing as well and raising dividend payout simply to keep the dividend streak alive? This is something we’ll need to monitor closely moving forward.

Dividend Reinvestment Plans (DRIP)

For years, our strategy for growing our dividend income has been quite simple. We rely on the three key pillars:

- We purchase more shares with new contributions

- We let dividends grow via organic dividend growth (i.e. dividend hikes)

- We enroll in dividend reinstatement plans and drip more shares every month

As you can see from our 14.27% YoY growth between September 2023 and September 2024, this simple strategy works quite well.

Since day 1 of our investing journey, our goal has always been trying to accumulate sufficient shares so we can drip at least 1 share at every dividend distribution. However, because enrolling in synthetic drip (i.e. DRIP one or more full shares) typically takes quite a bit of capital, some investors may overlook DRIP.

With the advance of discount brokers, synthetic drip no longer is the only option in town. Because Wealthsimple Trade allows for fractional DRIPs, we can drip regardless of how many shares we own and take advantage of the power of compounding.

In case you’re thinking of opening an account with Wealhsimple or transferring your existing account over to Wealthsimple, you can use my referral code. You’ll get a $25 reward for simply signing up.

In September, we dripped the following shares:

- 3 shares of Brookfield Asset Management

- 3.37 shares of Brookfield Renewable Corp

- 0.077 shares of BlackRock

- 0.271 shares of Canadian Tire

- 40.669 shares of Enbridge

- 3 shares of Fortis

- 0.1 shares of Alphabet

- 0.685 shares of Granite REIT

- 0.258 shares of McDonald’s

- 9.765 shares of Manulife Financial

- 0.432 shares of PepsiCo

- 0.084 shares of Qualcomm

- 0.079 of QQQ

- 6 shares of SmartCentres REIT

- 0.487 shares of Target

- 0.054 shares of Visa

- 0.165 shares of Waste Management

- 0.178 shares of Walmart

Thanks to enrolling in DRIP, we automatically added 68.674 shares without paying any trading commissions. More importantly, we added $205.66 toward our forward annual dividend income.

Stock Transactions

The market was somewhat volatile throughout September which meant buying opportunities.

When I looked at Canadian Natural Resources, I noticed the stock has been trading close to the 52 week low. Seeing this as an opportunity to add more CNQ shares and increase the weighting in our dividend portfolio slightly, we added 92.6356 shares of CNQ.

By a complete coincidence, this was the second straight month that we added more CNQ shares.

This transaction added $194.53 toward our forward annual dividend income.

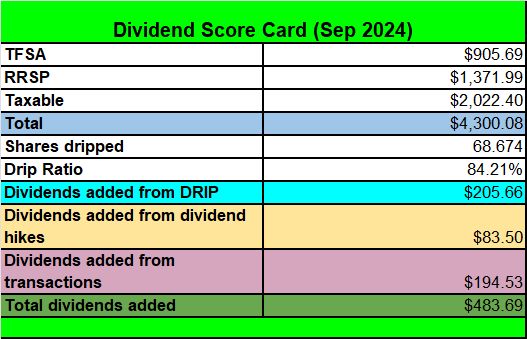

Dividend Score Card – September 2024

Here’s our dividend score card for September 2024.

We successfully added $483.69 toward our forward annual dividend income, which I am very pleased with.

Q4 2024 thoughts

For the remainder of the year (i.e. Q4), the focus is saving up $14,000 for next year’s TFSA contributions. It would also be nice to save a bit more so we can set aside money for RRSP contributions.

Because we are busy saving money, we probably won’t be purchasing any stocks. However, if the market was to go for a deep nose dive, we wouldn’t hesitate to take the opportunity to buy more stocks. After all, we don’t necessarily have to max out our TFSA contributions on January 1st, we could always save later and max out TFSA contributions throughout 2025.

I have been doing DIY investing for over a decade. One thing I have learned is that we cannot control the market. The market will do whatever it wants to do and can go for wild swings in the short term. We simply cannot control whether it’s a bull market or a bear market.

But there’s one thing we can control – our savings rate and how much new money we invest into the stock market.

Spending less than you earn and widening the income and expense gap is the key.

As Londoners would say “Mind the gap!”

Stop worrying about the day-to-day market changes – there’s absolutely nothing you can do about them. So why waste your time worrying?

Rather than wasting your time worrying about the market and your daily portfolio value change…

- Focus on increasing your savings rate

- Focus on investing more new cash in your portfolio

- Focus on time in the market

- Focus on the magic of compounding

- Focus on your long term goals

As I mentioned at the beginning of the post – keep it simple!

Summary – Dividend Income September 2024 Update

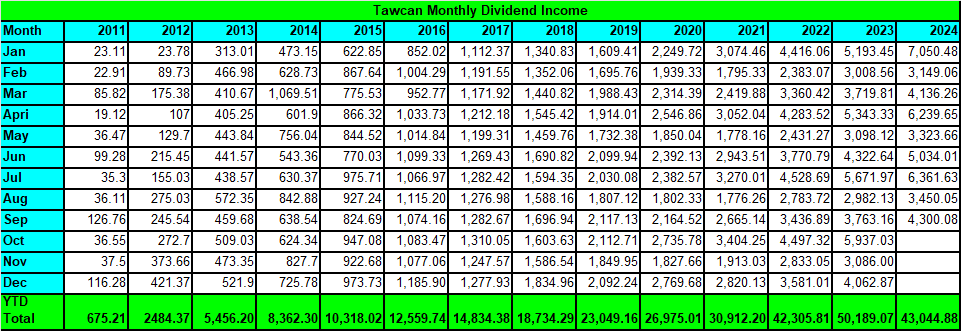

After nine months, we have received $43,044.88 in dividend income.

To put things in perspective, $43,044.88 is equivalent of:

- $157.10 per day or $6.55 per hour we’re earning

- $1,076.12 per week or $26.90 hourly wage after 40 working weeks.

Years ago when I had my first part-time job working at a local computer company, I was earning $10 per hour. When I graduated from university and started working at my full time job, I was earning about $24 per hour. It’s pretty amazing to see that our dividend portfolio has become a money generating machine, working hard for us so we don’t have to.

We are super grateful that we’re doing well financially. Therefore we try to help others in need by donating money monthly and volunteering our time. We’d encourage you to do the same if you possible.

How was your September dividend income?

I just want to say thanks! I’ve learned so much from you! =)

You’re very welcome.

Hi Bob,

Regarding Emera they indicated in their previous quarterly release that they were intentionally reducing their dividend growth to focus more on growth (reading between the lines debt reduction). Their September increase was at the bottom of their revised dividend growth guidance but given the shape the stock price is in it doesn’t have me worried.

Focus on more growth is a good idea. We’ll have to see what happens with Emera moving forward. Lower interest rates should help them.

Hi Bob,

I’d like to hear your opinion on this situation; I’m not sure if you’ve experienced it yourself. Let’s say your investment’s market value has increased by 50%, but you’re still receiving 4% based on the original capital value. In that case, would you sell your investment and reinvest in another one that also pays 4%, thereby increasing your dividend income? For example, if you invested $100K and the market value is now $150K, but you’re still receiving 4% dividends on the $100K, would you sell that stock and buy another one paying 4% to boost your dividends by 50%?

I wouldn’t. In your example you’re looking at yield on cost. That’s not the same as current yield.

If you only look at yield to determine whether you sell or not, then you’d never get any multi-baggers. Total return matters.

That’s awesome! Mind the Gap indeed.

Thank you!

Just curious do you have mortgage? Because you mentioned saving for TFSA but you didn’t mention saving for lump sum

Thanks

We’re just saving for the TFSA. Not doing lump sum.

I’m just at the beginning of my financial savings journey at the age of 35. A little late to the party but was putting money into GICs for years as the thought of losing my hard earned money outweighed possible gains through the stock market. I’ve since pivoted earlier this year to redeploy funds into the stock market and find your story absolutely inspiring!

Just curious, why invest into individual stocks rather than a blend of stocks and etfs (like VDY, Xdiv, etc?

We do invest in a combination of individual dividend stocks and ETFs – you can see our portfolio here https://tawcan.com/dividends/

Also, I don’t think you started too late. Better starting now than never. 🙂

You’re the man! I look forward to reading more and browsing. You’re an inspiration, my good sir! Keep it up 🙂

Juicy. So juicy!

Thank you Dividend Daddy.

Solid and fun month! Congrats on over $4K! I must say, I have never eaten beaver tail lol. Was it good? 🙂

Thank you, beaver tail was good.