Wow it’s hard to believe there are only two more months left before 2024 is over. Looking at the Archives page, it felt like it was only a few weeks ago when I interviewed Dividend Daddy and posted our Q&A.

For those of you who are new, we have been building our dividend portfolio since 2011 by investing in both individual dividend stocks and index ETFs. The goal is to become financially independent and live off dividends by 2025.

Yes, 2025 is just around the corner but we aren’t really in a rush to call ourselves financially independent yet (technically we can). We are enjoying the journey and learning to be open to different opportunities.

In case you’re curious, you can check out the stocks and ETFs we own here – Dividend Portfolio.

At the time of writing, we own 43 dividend stocks and 2 index ETFs. Since 28 of the 43 dividend stocks we own are Canadian companies, we utilize index ETFs for geographical and sector diversification.

October was a busy month for me. Thanks to travelling for work, I spent 12 days in Asia – seven days in Japan, and five days in Taiwan.

I have visited Japan many times in the past but it has been a while since my last visit. I visited Osaka and Kyoto in 2019 for a family trip. Before that was a work trip back in 2016.

While in Japan, I spent a lot of time on trains. During four full work days, I did day trips from Tokyo to the following places:

- Sendia (~1.5 hours by Shinkansen aka bullet train from Tokyo)

- Mizusawa (another hour north of Sendia by Shinkansen)

- Nagoya (~1 hours by Shinkansen from Tokyo)

- Yokohama (~30 minutes from Tokyo by commuter train)

While in Tokyo, I spent a lot of time walking, and riding the train and subway. At the end of the week, I spent a night in Osaka (~2.5 hours by Shinkansen from Tokyo) before heading back to Tokyo the next day.

I will probably go back to Japan in March or April next year. For that trip, it’d certainly be nice to spend more time in Tokyo and not have to visit so many cities.

Although there were a lot of work meetings and train rides, I did get to enjoy a lot of good food while in Japan. Food in Japan is amazing and this is one of the main reasons why I love going to Japan.

I was also fortunate to be able to spend an entire Saturday in Tokyo. Not wanting to spend more time on trains and subways, I walked as much as possible to explore the city and the surrounding areas. After walking over 37,000 steps, my feet were slightly sore the next day.

Since I had visited Taiwan regularly over the last few years, the only pictures I took there were food pictures.

At home, both kids learned about Italy for their home school monthly project. As part of the monthly project, Kid 1.0 learned how to make squid ink pasta and Kid 2.0 learned how to make biscotti.

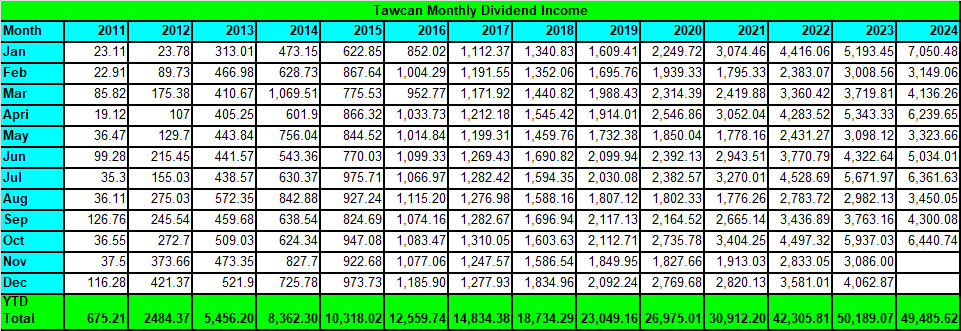

Dividend Income – October 2024

In October, we received payment from the following companies:

- BCE Inc (BCE.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Capital Power Corp (CPX.TO)

- Granite REIT (GRT.UN)

- Coca-Cola (KO.TO)

- SmartCentres REIT (SRU.UN)

- Telus (T.TO)

- TD (TD.TO)

- TC Energy Corp (TRP.TO)

- VICI Properties (VICI)

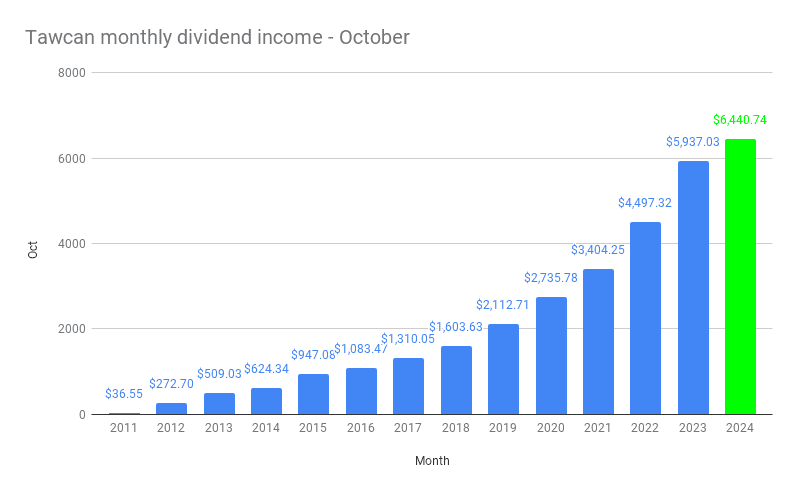

These 12 payments added up to $6,440.74. A very strong month with dividends over $6,000!

Compared to October 2023, we saw a YoY increase of 8.48%. This is the third lowest YoY increase so far this year. Despite purchasing some TD, Telus, TRP, WCN, and CNQ shares throughout 2024, most of the dividend growth from October was a result of organic dividend growth and DRIP.

If we look at the YoY increase average after 10 months, we’re at 14.97% which is quite respectable. It’d be nice to finish the year at above 15%.

Dividend Hikes

In October, the following companies announce dividend hikes:

- AbbVie (ABBV) raised its dividend payout by 5.8% to $1.64 per share

- Canadian Natural Resources (CNQ.TO) raised its dividend payout by 7% to $0.5625 per share

- Visa (V) raised its dividend payout by 13% to $0.59 per share

- Waste Connections (WCN.TO) raised its dividend payout by 10.5% to $0.315 per share

These four dividend hikes increased our forward annual dividend income by $127.96. I was very pleased to see a payout increase of more than 10% from both Visa and Waste Connections.

Canadian Natural Resources is sitting on a lot of cash right now so it will be interesting if the company decides to pay out a special dividend next year.

After 10 months, we increased our forward annual dividend income by $1,461.49 thanks to dividend hikes. At a 4% dividend yield, that’s equivalent to investing $36,537.25 of new capital. This is exactly why organic dividend growth is so important as your dividend portfolio and dividend income get larger.

Dividend Reinvestment Plans (DRIP)

Many readers know that DRIP is the second pillar of growing our dividend income. We try to enroll in DRIP whenever we are eligible.

With Questrade and TD, one must accumulate sufficient shares in order to drip at least one share. This is called a synthetic drip. For low yield stocks,- or ones with a high share price – it is often very difficult to accumulate enough shares to drip one share.

For example, with Apple yielding less than 0.5% and paying out $0.25 per share, that means you’d need at least 890 shares to drip one share of Apple at every quarter. At $223 per Apple share, you’d need $198,470 to do that. That’s a lot of money to invest in one single stock.

Fortunately, synthetic DRIP isn’t the only method anymore. With Wealthsimple Trade, you can enroll in fractional DRIPs, which allows investors to drip and accumulate shares regardless of how many shares they own.

This is one of the key reasons why I moved my RRSP and TFSA from Questrade and TD to Wealthsimple – to take advantage of fractional DRIP and drip some low yield stocks while we’re working towards our goal of living off dividends.

If you’re thinking of opening an account with Wealhsimple or transferring your existing account over to Wealthsimple, you can use my referral code or type in YDC3NA when you sign up. You’ll get a $25 reward for simply signing up.

Wealthsimple has a new promotion, which allows you to get an iPhone or a Mac laptop when you register and move $100,000 or more to Wealthsimple.

You need to register by December 13th to be eligible for the following:

- Transfer or deposit $100,000 or more within 30 days of registering

- Once you qualify you can choose an iPhone or a Mac starting January 15th

- Deposit $100,000 – $299,999 and you’ll get an iPhone 16 or a MacBook Air.

- Deposit $300,000 – $499,999 and you’ll get an iPhone 16 Pro or a MacBook Pro.

- Deposit $500,000+ and you’ll get an iPhone Pro Max or a MacBook Pro with M4 Pro.

It’s not as generous as the previous 1% match promotion but if you’re looking to get a new phone or laptop, it’s an offer you could take advantage of.

In October, we dripped the following shares:

- 22.252 shares of BCE

- 13.027 shares of Bank of Nova Scotia

- 11.05 shares of CIBC

- 1.999 shares of Canadian Natural Resources

- 1.921 shares of Capital Power Corp

- 1.696 shares of Coca-Cola

- 6 shares of SmartCentres REIT

- 29.775 shares of Telus

- 15.586 shares of TD

- 11.863 shares of TC Energy Corp

- 2.444 shares of VICI

Thanks to DRIP we added 117.613 new shares without paying any trading commissions. We also added $367.41 toward our forward annual dividend income. At a 4% yield, that’s equivalent to adding $9,185.30 of new capital.

Stock Transactions

We didn’t make any stock transactions in October. That was because we are saving money for next year’s TFSA contribution room. In addition, we are also saving money for RRSP too.

For November and December, I believe we will be relatively quiet on the stock transaction front. I wouldn’t say never though. If there’s a good buying opportunity, we could move the money saved up and take advantage of the situation.

After all, we could always save for TFSA throughout 2025 too. There’s no rule that we must max out our TFSAs on January 1st and use the money to buy stocks on the first day when the market opens in the new year.

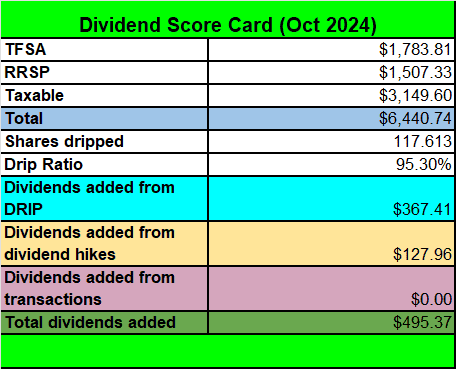

Dividend Score Card – October 2024

Here’s our dividend score card for October 2024.

51.1% of our October dividend income was either tax-free or tax-deferred. The remainder, $3,149.60, is taxable but it’s split about 48%-52% between me and Mrs T. By investing together and treating our investments as one big portfolio, we are income splitting and lowering our overall tax hit.

If you are married or have a common-law spouse, I believe it is a good idea to invest together and work toward financial independence in two-player mode rather than single-player mode.

Looking Ahead – A Few Thoughts

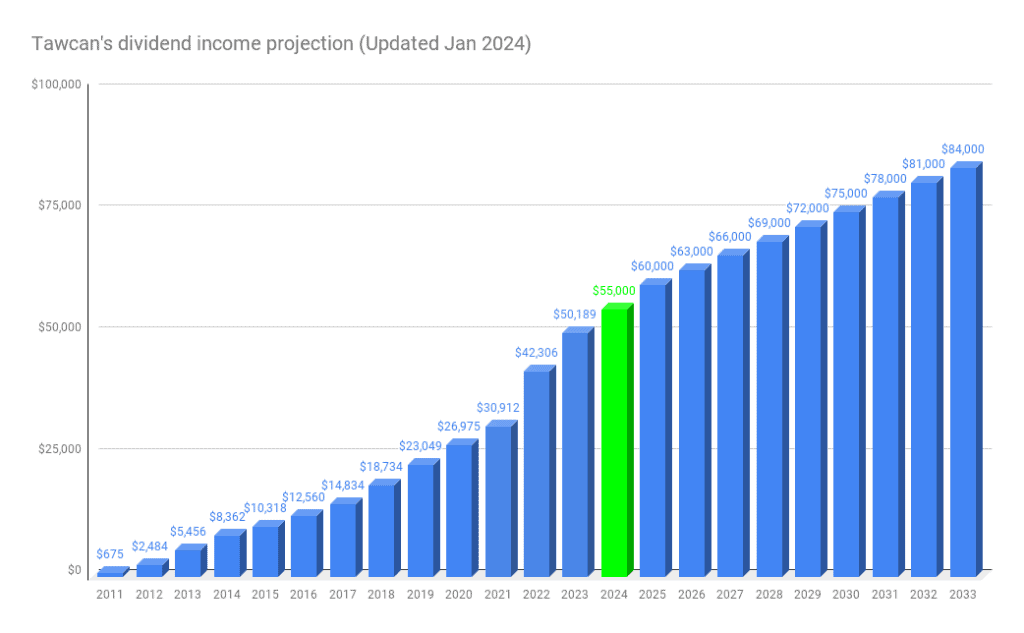

Our dividend income goal for 2024 is $55,000. With two months left, I think we can easily achieve this goal.

So what’s ahead for us for 2025?

Hitting $60,000 in dividend income should be doable. For now, I won’t change the dividend income projection for a few reasons.

First of all, as our dividend income gets bigger, it becomes increasingly more difficult to increase dividend income via fresh capital. For example, going from $1,000 to $2,000, a 100% YoY increase, will require $25,000 in new capital at a 4% dividend yield. Many people can save $25k a year for investment. On the other hand, going from $55,000 to $60,000, a 9% YoY increase, will require $125,000 in new capital at a 4% dividend yield. Not many people will have $125k sitting around for investment.

The law of the big numbers is very real!

Can we grow our dividend income by relying on organic dividend growth now that our dividend portfolio is sizable?

Yes, we can. But there’s no guarantee a dividend stock will continue to hike its dividend payout by 10% or more every single year. Typically higher yield stocks will have a lower dividend growth rate; lower yield stocks will have a higher growth rate. But that’s not a set rule. It is also unrealistic to assume a company will raise its dividend payout by over 15% indefinitely. At some point, the dividend growth rate will slow down.

Furthermore, as one’s portfolio becomes more diversified, the dividend payout increase for each stock effectively diminishes due to the diversified nature of the portfolio. For example, in a portfolio with five stocks, if one stock raises dividend payout by 25%, that effectively raises your forward annual dividend income by 5%. In a portfolio with 25 stocks, however, the 25% payout increase would only increase your forward annual dividend income by 1%.

One also cannot control whether a company decides to increase its dividend payout or not. We have no control over this parameter and therefore are at the mercy of the company.

This is why enrolling in DRIP, whether synthetic or fractional, can be helpful in boosting dividend income growth. DRIP allows one to increase forward annual dividend income drip by drip (pun intended!).

One important thing to keep in mind is that dividend income growth via DRIP and organic dividend growth don’t all come in January. They are usually spread across the entire year. Similarly, one typically doesn’t just inject all the capital in one big lump sum in January.

So growing dividend income by $5,000 in a year typically requires more than what the simple math tells you. Because for current year’s dividend income, the “growth” from fresh capital, dividend hikes, and DRIPs diminishes as the year goes by.

Another key reason why I don’t want to increase our annual dividend income goal is because I don’t want to chase high yield stocks for the sake of simply hitting our annual dividend income goal. We got caught years ago by investing in Inter Pipeline and Algonquin Power & Utilities Corp when we were too focused on the final numbers rather than the health of the dividend payments. I don’t want to repeat that!

My final point brings me to BCE – the current headache of our portfolio. Earlier this month, BCE annonced it’d pay $5 billion to purchase U.S. internet provider Ziply. The company would also pause dividend hikes in 2025. It also announced very poor quarterly results in November.

All these “bad” announcements hammered BCE’s share price in a very very bad way.

Honestly, I don’t really know what the BCE board was thinking about. First, the board decided to sell 37.5% minority stake in Maple Leaf Sports & Entertainment (MLSE) to Rogers Communications for $4.7 billion. The transaction is expected to close in mid-2025. To me, the MLSE is an appreciating asset that will bring in more revenues for BCE for years to come. So the decision to sell the MLSE stake to Rogers doesn’t make any sense to me. Then before the transaction is closed, BCE then turns around and spends more money to buy Ziply.

Perhaps there’s something I’m not seeing but these two decisions don’t make any sense to me. Yes, I understand that BCE wants to grow in the US but the two transactions just don’t seem to line up. As a shareholder, I’m really losing my confidence in the BCE board. BCE is really starting to smell and feel like a repeat of AQN.

Is it time for us to either reducing BCE shares or closing it completely? Either way, it will mean taking a big loss and a hit on dividend income.

I haven’t decided what to do yet because I don’t want to make any knee jerking decisions. Remember, investing on emotion can result in making really bad decisions. Having said that, Perhaps we may consider selling some BCE shares and reinvesting that money elsewhere. Sometimes, it’s better to take the loss and move on than hoping the company can turn things around…

Is the dividend income projection chart from above too conservative? Can we grow our dividend income a bit more from 2025 and beyond?

When I updated the projection in January 2024, I thought we’d start saving money for our cash reserves in those years instead of investing the bulk of the money toward our investment portfolio.

Because life is dynamic, that plan may change and I probably need to adjust the dividend income projection periodically.

So where are we on our quest for financial independence?

An annual dividend income of $60,000 is quite substantial whichever way you slice it. Can we live off on $60,000 dividend income only? For a family of four, we probably could, but I think our lifestyle may suffer. Due to inflation and kids getting older, our expenses have increased over the years. I don’t want to restrict ourselves by living off only on $60,000 and needing to cut a lot of expenses.

The solution might be working part time and generating income around $20,000 or so. We should be able to live pretty comfortably with an annual income between $80,000 to $90,000 without having to consider cutting expenses.

As mentioned above, we aren’t in any rush to “get there” per se. We plan to continue with our investing strategy and enjoy the financial independence journey.

Summary – Dividend Income October 2024 Update

I’m very pleased to see that we have received $49,485.62 in dividend income so far in 2024. By the end of November, we will end up with an amount that exceeds last year’s annual income.

Needless to say, we have come a long way from our less than $100 monthly dividend income in 2011. Our financial independence journey is a true testament that takes time and patience to build up a sizable investment portfolio. It is important to stay focused and execute your investing strategy, rather than switching strategies back and forth constantly.

To put things in perspective, $49,485.62 after 10 months is equivalent of:

- $162.25 per day or $6.76 per hour our dividend portfolio generates

- $1,124.67 per work week or $28.12 hourly wage

We feel blessed and very fortunate that our dividend portfolio is working hard for us so we don’t have to.

Earn, save, invest, grow your income and spending gap, and repeat. It doesn’t get simpler than that.

But simple doesn’t mean it’s easy!

Dear readers, how was your October dividend income?

Great stuff – congrats! BTW small nitpick – I believe you have a typo above – you wrote: After 10 months, we increased our forward annual dividend income by $1,461.49 thanks to dividend hikes. At a 4% dividend yield, that’s equivalent to investing $104,037.25 of new capital. Shouldn’t that read $4,161.49 instead of $1,461.49? At least that’s what the math would suggest. 😉

Thank you Mike. Yes that was a typo indeed. It should say $36,537.25, not $104,037.25. Thanks for pointing that out.

Hi,

Thank you for the great article. I am new to investing and I have a question for you. In the article, you mention the possibility of a special dividend from Canadian Natural Resources as they are sitting on a lot of cash. What does a special dividend entail? I have never heard of this before. And is it something every company does when they have a lot of cash on hand? I have some CNQ in my portfolio.

Thank you!

Hi Vicky,

Special dividend is non-recurring, “one-time” dividend distributed by a company to its shareholders. CNQ has done this in the past.

BCE just announced a 2% discount on DRIP shares.

Funny you wrote about BCE because I was going to ask your thoughts about it. I lost with AQN and I’m feeling the same way with BCE. I’m holding for now and hope I don’t regret it. I can live without the dividend increase but they need to right the ship. I thought they’d use the sale to pay off debt to reduce the interest payments. The US is a tough market to compete in because the telcos there are big players. They can play chicken until BCE loses. I’m holding for now but it’s a tough one to watch and wait.

It was a strange decision to buy Ziply, but I look at it as the only way for BCE to do well. Canada, with no population growth and lower immigration, has no growth in customers for BCE, or any of the telecoms. If they don’t buy customers, they’ll just meander and stay flat. Yes, it’s a risk, but it may well be one that lets them grow out of trouble.

Yes, BCE needs to steer the ship and instill some confidence with their shareholders.

I get the feeling that BCE is going to be another Nortel as they are the same family.

YouTube has two interesting videos On Nortel . Both very interesting to watch

The biscotti look scrumptious!

They were pretty good. Need to ask Kid 2.0 to make more. 🙂

Good afternoon,

I agree that food in Japan is wonderful. My experience of Japan is not as extensive as yours, a group of twenty of us travelled to Japan in 2019 for two weeks hiking. The experience will always remain with I and my wise.

Now, like you I am a dividend investor. I learned about it in 1990’s from Tom Connolly. I am much older then you and our portfolio generates a healthy six figures.

I need your opinion about US dividend stock. I have some US dollars and wish to invest it to generate US dollars.

Thank you.

Glad to hear that you enjoyed Japan too!

Congrats on having a portfolio generating six figures. That’s amazing!

In terms of US dividend stocks, they typically have lower yields than Canadian stocks. I’d look at stocks like Apple, Visa, MasterCard, Costco, and Google. Hope this helps.

The BCE price drop and frozen dividend rate for 2025 is certainly disappointing.

But … there’s always a “but” … BCE stock is now yielding 10.6%. Buying Bell now at this dividend rate more than offsets for the possibility that the dividend could be frozen for the next 7-8 years!! Once a stock yield gets up in the stratosphere then many companies opt for cutting the dividend to bring the yield down to levels more in line with similar sector stocks. True …. many companies will do that … but somehow I don’t think Bell (the mother of all dividend paying stocks) would actually cut their dividend. The stock price would be decimated – it would probably fall to under $20. BCE is so widely held – an actual dividend cut would definitely be noticed for exactly what it is – less dividend income – not a yield reduction – people won’t be fooled. Pension funds and other institutional investors rely on this income to pay pensions, etc.. A cut would be very harmful. All credibility in BCE stock as a safe, long-term investment would be completely destroyed. I don’t think an actual cut is going to happen – the dividend might be frozen again for 2026 or a token increase offered. BCE would have to be in pretty horrendous shape for a cut to happen.

Plus, BCE still has many assets. And who knows, perhaps the buy of the USA Ziply Fibre will work out – surely BCE financial experts are not completely stupid – they must have found something compelling about the purchase and feel they can make it work. Obviously, they may also feel like other companies do (and the CPP) that investing in Canada is no longer a road to profitability – the USA has better opportunities – and the Trump presidency may also help if he reduces corporate taxes. If things get really bad, and this would be a clue of an impending dividend cut, BCE is likely to first suspend it’s DRIP program – issuing new shares from treasury at such low prices (as BCE is at now) is not fair to existing shareholders as it creates dilution and with more shares being issued also comes the obligation for BCE to pay out even more in dividends.

I’d sit tight with BCE holdings – if you need a capital loss for tax purposes – sell – and then buy BCE back. All is not lost – that capital loss is a valuable tax asset in itself.

Hi Reader B,

Good to hear from you. Very valid analysis. I think the biggest worry most people have is whether BCE will turn into AQN version 2.0. I don’t think so because the two companies are in completely different sectors.

You sure hope the BCE experts know what they’re doing with the UA Ziply purchase… selling MLSE then spend that money (and a bit more) to buy Ziply seems kind of odd. But BCE has been analyzing this purchase for over 2 years, so we probably should give them the benefit of the doubt?

You do raise a very good point about pension funds invested in BCE due to dividends. A cut would be devastating for sure.

I’m thinking this will be my strategy; sell my BCE in my non-reg account to crystallize the loss and park it while I decide to repurchase after 30 days. As for our registered accounts I’m likely to so something similar. Thanks for the input.

I sold some of my BCE last month at a loss, but ever the optimist, I held on to a little. Now I wish I had sold it all, as the price has plummeted even more. I used the money to buy a new front door, so feel I got something out of the deal.

Yes, the price keeps getting lower and lower. It’s tough. 🙁

How did you drip VICI? I have it sitting in RBC RRSP (work), and I have enough to drop a share but I was informed VICI does not have a DRIP and checked their website too.

DRIP through Wealthsimple (factional drip). We were dripping (sythentic drip) via Questrade before. It’s possible through your discount broker.

Best to dump BCE, not worth the headache.

That’s a fair comment. Something we’re considering but selling it at 52 week low and taking a loss may not make sense at this point.