Welcome to our latest monthly dividend income update.

For us, these regular monthly dividend income updates keep us accountable and demonstrate that it is possible to build up a sizable dividend portfolio over time. These updates are also a way for me to reflect and share my thoughts as a long term investor.

It has been an interesting ride since we started our financial independence journey in 2011. Whenever I go back and look at the old monthly dividend update posts, I would reconfirm this hybrid investing strategy and that sticking to it over the last 14 years has paid dividends…pun intended!

Drier weather in May meant that we spent more time outside – tending our backyard garden, going for local hikes, and taking the Cubs and Scouts on outdoor adventures.

Dividend Income – May 2025

In May, we received dividends from the following companies:

- Apple (AAPL)

- AbbVie (ABBV)

- Bank of Montreal (BMO.TO)

- Costco (COST)

- Emera (EMA)

- Granite REIT (GRT.UN)

- National Bank (NA.TO)

- Procter & Gamble (PG)

- Royal Bank (RY.TO)

- SmartCentres REIT (SRU.UN)

- Waste Connections (WCN.TO)

- Walmart (WMT)

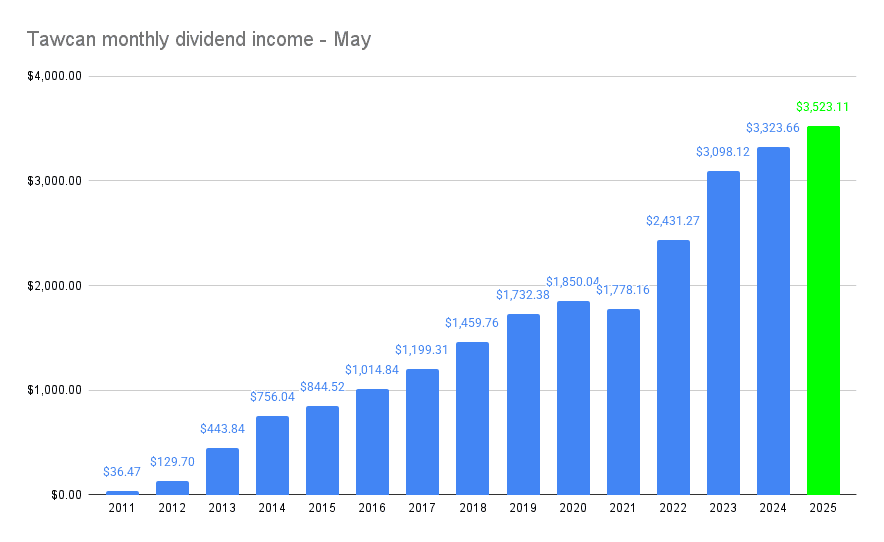

The 12 dividend payments added up to $3,523.11. Since May is one of the low dividend months, it was great to see the total number north of $3,500!

Compared to May 2024, we saw a YoY growth of 6%. This number is slightly lower than one quarter ago (February), which was 6.89% YoY growth.

It would be nice to see a bit higher YoY growth in these “weaker months.” But we need to keep in mind that not as many companies pay dividends in February, May, August, and November. Therefore, arbitrarily creating a “buying” rule simply to boost our monthly dividend income in these weaker months simply doesn’t make sense.

Dividend Hikes

May was a big month for us in terms of dividend hikes. We were very pleased to see so many companies raising their dividend payout.

- Hydro One (H.TO) raised its dividend payout by 6% to $0.3331 per share

- Telus (T.TO) raised its dividend payout by 3.5% to $0.4163 per share

- Bank of Nova Scotia (BNS.TO) raised its dividend payout by 3.8% to $1.10 per share

- Bank of Montreal (BMO.TO) raised its dividend payout by 2.5% to $1.63 per share

- National Bank (NA.TO) raised its dividend payout by 3.5% to $1.18 per share

- Royal Bank (RY.TO) raised its dividend payout by 4% to 1.54 per share

- Apple (AAPL) raised its dividend payout by 4% to $0.26 per share

- PepsiCo (PEP) raised its dividend payout by 5% to $1.4225 per share

It’s nice to always see Canadian banks raising their dividend payout. Since these Canadian banks have been paying uninterrupted dividends since the late 1800s and many of them have consistently raised their dividend payout, I do expect this trend to continue for a very long time.

These dividend hikes increased our forward annual dividend income by $663.80. At a 4% yield, that’s equivalent to investing over $16,500. That is why dividend hikes, or organic dividend growth, is so important!

Dividend Reinvestment Plans

We have been enrolled in dividend reinvestment plans (DRIPs) whenever we’re eligible. The idea is to drip shares whenever there’s a dividend payout and take advantage of dollar cost averaging.

Looking at our dividend portfolio, I am always amazed at how many shares we have managed to drip over the years. For example, we have dripped over 100 shares of Bank of Nova Scotia in my RRSP, over 280 shares of Manulife in my TFSA, over 72 shares of Royal Bank in my RRSP, and over 68 shares of TD in Mrs. T’s non-registered account. I truly believe enrolling in DRIP is one of the best ways to put your investments on autopilot and avoid the day-to-day emotional roller coaster caused by market volatility. (and drips dramatically prove the positive snowball effect of compound interest.)

- Sign up for Wealthsimple with my referral code or type in YDC3NA when you sign up. You’ll get a $25 reward for simply signing up.

- Sign up for Questrade with my referral code. You’ll get a $50 reward for opening an account.

In May, we dripped the following shares:

- 0.391 shares of Apple

- 0.683 shares of AbbVie

- 3 shares of Bank of Montreal

- 0.047 shares of Costco

- 2.931 shares of Emera

- 0.55 shares of Granite REIT

- 6.762 shares of National Bank

- 0.614 shares of Procter & Gamble

- 4.306 shares of Royal Bank

- 0.161 shares of Walmart

- 0.081 shares of Waste Connections

In total, 25.526 shares were dripped and $2,772.15 out of the $3,523.11 was reinvested automatically for a DRIP ratio of 78.7%.

Thanks to DRIP, we increased our forward annual dividend by $107.45.

Stock Transactions

We had a busy month back in April, when we deployed slightly over $10,000 of new capital. Compared to April, May was a much quieter month. Despite the market going higher and higher, we ignored the market performance and continued to add new capital to our dividend portfolio regularly. This strategy has done well for us over the years so we have no plan to deviate from it anytime soon.

We added the following stocks throughout May:

- 117.102 shares of Canadian Natural Resources (CNQ.TO)

- 5 shares of iShares ex-Canada International ETF (XAW)

- 2 shares of Royal Bank (RY.TO)

A total of just over $5,400 was deployed. The 5 shares of XAW and 2 shares of Royal Bank were purchased during down days using cash sitting in our account (since both Questrade and Wealthsimple offer free trades nowadays, we were able to do small orders without getting penalized by the trading commissions).

We bought more Canadian Natural Resources shares to mostly take advantage of the depressed share price. CNQ share price has tumbled quite a bit in the last 12 months but I believe long term the share price will recover and go higher. At an initial yield of more than 5.5%, I think CNQ is extremely attractive for dividend investors.

These transactions added $291.13 toward our forward annual dividend income.

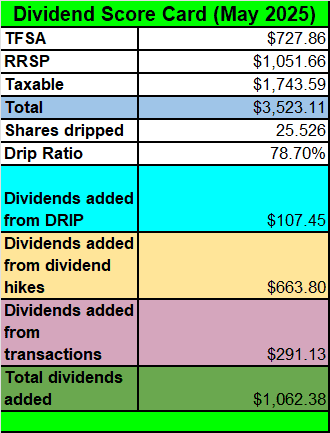

Dividend Scorecard

Here’s our dividend scorecard for May:

A very solid month overall. I was very pleased to add over $1,000 toward our forward annual dividend. Over the years, after maxing out our RRSPs and TFSAs, we have been adding new capital to non-registered accounts. In recent months, we have been receiving a higher dividend amount from non-registered accounts than RRSPs and TFSAs – a sign that our hard work is paying off!

Why is this important? Because eligible dividend income from Canadian companies is extremely tax-efficient. In fact, you can pay $0 in income tax if you receive $57,375 or less in dividend income and have no other income (note, this is for BC, the actual numbers in other provinces may be slightly different). When we are living off dividends, we want to fund our expenses from non-registered accounts as much as possible.

Some random thoughts on the market & our portfolio

For the most part, the market has recovered from Liberation Day. The 90-day tariff pause has calmed the market. But what’s going to happen in July? Will we get more market volatility?

One thing I know is that the market doesn’t like uncertainty. If there are uncertainties in the upcoming months, I am sure the market will go back to being very volatile again. However, a volatile market is actually quite beneficial for people who are in the accumulating stage, because they can buy stocks and ETFs at a discounted price!

Looking back, I’m glad that we were able to buy shares of National Bank and Capital Power Corp in March and April at under $120 and $49 respectively. As a long term investor, it’s important to ignore the noise and take a very long term view. For example, when TD went down below $75 due to the money laundering scandal, did anyone have the foresight that the TD share price would recover in less than a year and get above $90? At the time, most people were predicting that TD’s share price would stay flat and suffer for an extended period of time. But when TD made some significant leadership changes,cleaned up their balance sheet, and promised to buy back shares, the share price popped.

Sometimes it is necessary to find diamonds in the rough and take these opportunistic bets. Some may not work out, but some will. Your betting percentage increases greatly when you “bet” on solid companies that have demonstrated long term profitability.

As in previous years, we added quite a bit of fresh capital in the first half of the year. As we get into the second half of the year, I anticipate that we will move into savings mode and start saving money for next year’s TFSA rooms. Throughout June, we plan to buy more XAW shares before the ex-dividend date so we can collect the semi-annual distribution at the end of June. Other than purchasing more XAW, we don’t plan to do anything else, unless opportunities come up in the form of extreme market volatility.

One thing we have been working on in the past few years is to reduce the number of holdings in our dividend portfolio. We closed out Canadian Tire earlier this year and unfortunately, the stock price has shot up since. But that’s alright. It’s not something we could have predicted and since our Canadian Tire position was relatively small, the share price pop wouldn’t have made much difference in the grand scheme of things anyway (we did OK anyway by using the money from Canadian Tire to buy TD shares). Anyway, at the time of writing, we hold 42 individual dividend stocks. The plan is to continue to reduce that number and hopefully we end the year at around 35 (it’s a tall task!). Since positions like Qualcomm, South Bow, VICI Properties, Granite REIT, and Hydro One are relatively small in our portfolio (they each make up less than 0.5% of our portfolio). Thus, it might be worthwhile to close out these positions and reinvest the money elsewhere. The tricky part is deciding when to sell…

Summary – Dividend Income May 2025 Update

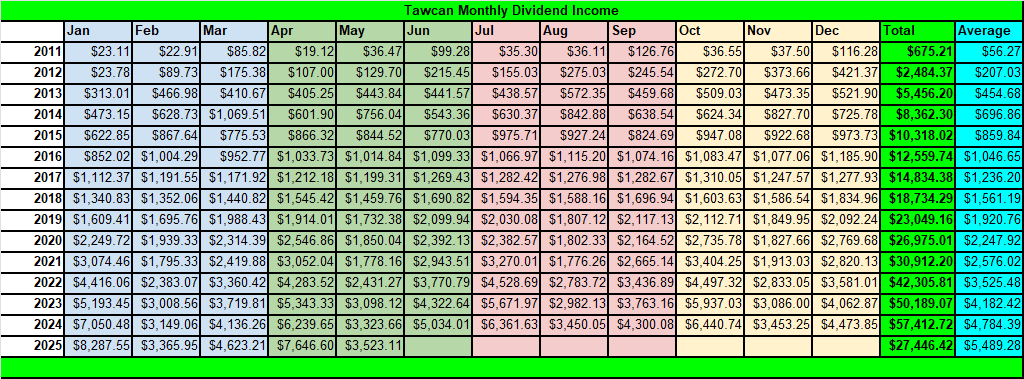

After five months of 2025, we have received $27,446.42 in dividend income or a monthly average of $5,489.28 per month. At $27,446.42, we have already exceeded the total dividend income we received in 2020! It’s quite amazing how much progress we have made, especially in the last five years!

As usual, to put things in perspective, $27,446.42 after five months is equivalent to:

- $181.76 per day or $7.57 per hour that our dividend portfolio generates, regardless of what we’re doing

- $1,247.56 per week of $31.89 per hour after 22 working weeks

Based on our current dividend income projection, I am quite confident that we will not only beat our $60,000 dividend income goal for this year but exceed it by a wide margin!

It’s great that our money is working hard for us. Despite doing well financially, we don’t feel the need to show off. You won’t see us driving fancy cars, wearing fancy clothes and jewelry, or designer bags. Mrs. T and I continue to teach both kids that we need to remain humble and treat everyone the same way, regardless of their social status. Be kind, be a valuable member of the community, be a role model whenever you can, and always treat others as how you want to be treated.

Dear readers, how was your May dividend income?

Hi Bob,

This is the first time I’ve commented since I started following you in 2017. Your work inspired me to forge my own path and move on from a financial advisor who didn’t pay much attention to me. That year I earned $1,100 in dividends. By the end of 2025 I’m expecting to hit or exceed $40,000 in dividends. Keep up the good work. I appreciate the content you publish weekly.

Best,

CW

Hi CW,

That’s amazing! Thank you for following along since 2017, I really appreciate it!

Have you thought of replacing REITs and others u mentioned above with stocks such as CCL, NTR and SJ? I personally like Hydro one so will be keeping it unless you can share a good reason to sell. Thanks

We used to own NTR but closed it many years ago. No plan to add more positions at this point.

Congrats on a great month!

Thank you, a weaker month but still a good one regardless.

Hi Bob,

Looks like you’ll end the first half of the year with over 32000. Considering you are benefiting from dividends reinvestment, fresh capital and organic growth, you’ll probably end the year over 65000.

Thanks Alex, we’ll have to wait and see what the final amount is. 🙂