It’s a new month and that means it’s time for another monthly dividend income update.

For new readers to this site, I have been posting monthly dividend updates since starting this blog in July 2014. These monthly updates are useful because they help us chronicle our financial independence journey. They also help us demonstrate that it is possible to build up a sizable dividend portfolio over time. More importantly, these dividend updates also underscore the transparency that is all-important.

If you’re curious about our progress over the years, you can check out our dividends page.

Some readers have been asking about our yearly portfolio return. I previously shared the returns but decided to create a dedicated page. You can check it out here – yearly portfolio return.

I mentioned in the April dividend income update that April was a busy travel month for me – I went to Taiwan, China, Hong Kong, New York, New Jersey, and Atlanta. I then travelled to Europe at the end of April.

Fortunately, it was an extended stay in Europe.

Since Mrs. T and I started dating, got married, and had kids, we have been going back to Denmark every year and a half, alternating between summer and winter. We only broke this frequency due to the global pandemic a few years ago.

And because I have been working remotely since the beginning of the pandemic and my manager is very supportive of a flexible working schedule, working from Denmark instead of Vancouver wasn’t a concern at all.

We arrived in Denmark in late April and spent the entire month of May in the land of the Vikings, visiting Mrs. T’s family and friends. We also had lots of time to visit various places for educational purposes (for the kids).

Other than going to the museums, we also walked around town and checked out Frederiksberg Zoo.

Eating out in Denmark is quite expensive. Even a cup of latte is quite expensive (45 DKK / $9 CAD or more). Oddly enough, Ice cream is one of the few things in Denmark that is much more affordable than Vancouver.

Although I worked remotely while in Denmark, I managed to take a week off and spend it at the family’s summer house. We had warm and sunny weather that entire week. As luck would have it, it started pouring the next day.

Since we are big fans of LEGO, visiting Denmark meant a mandatory trip to Legoland in Billund.

Sadly, a small part of Legoland (Miniland) with replica of famous buildings burned down a few days after we visited.

My bonus-father-in-law used to teach at a farm trade school so he took both kids to the school to teach them a few things about farming.

Kid 1.0 & Kid 2.0 also attended a few meetings with the local Scouts group (FDF).

At the end of May, I also travelled all over France, Denmark, and Sweden for a work trip and visited European customers. I managed to get some time to walk around the different cities and check out the sights.

Dividend Income – May 2024

OK, enough pictures and let’s get back to the monthly dividend income report, shall we?

In May we received dividends from the following companies:

- Apple (AAPL)

- AbbVie (ABBV)

- Bank of Montreal (BMO.T)

- Costco (COST)

- Emera (EMA.TO)

- Granite REIT (GRT.UN)

- National Bank (NA.TO)

- Power Corp (POW.TO)

- Procter & Gamble (PG)

- Royal Bank (RY.TO)

- Starbucks (SBUX)

- SmartCentres REIT (SRU.UN)

- Waste Connections (WCN.TO)

- Wal-Mart (WMT)

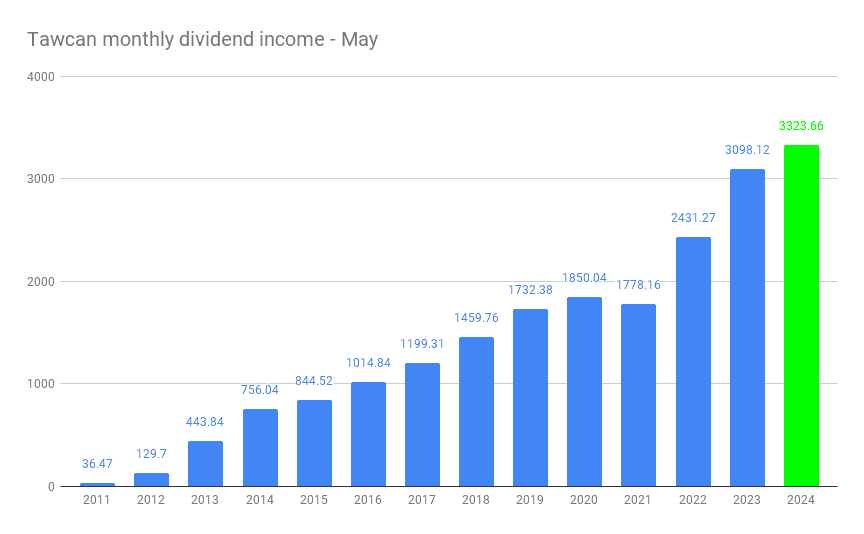

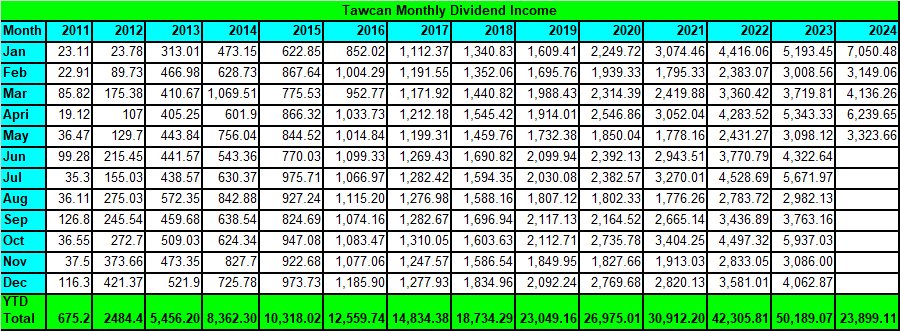

The paycheques from 14 companies added up to $3,323.66. Since February, May, August, and November are the weakest dividend months for us, we were quite pleased to see the May dividend income ending with over $3,000.

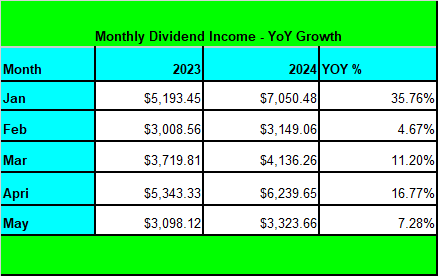

Compared to May 2023, we saw a YoY growth of 7.28%. This was the 2nd weakest YoY growth rate so far this year and corresponded to our weakest dividend months.

Most of the dividend income growth was due to organic dividend growth and DRIP. We typically don’t buy stocks based on when dividends are paid out. For us, buying based on when dividends are paid out only reduces the number of dividend stocks available to purchase and you may end up buying something not as desirable in the long run.

Dividend Hikes

Due to the law of big numbers, we have been focusing on adding dividend stocks that consistently grow dividend payout at a high rate rather than dividend stocks that have high initial yield.

In May the following companies announced dividend hikes:

- Apple (AAPL) raised its dividend payout by 4% to $0.25 per share

- Telus (T.TO) raised its dividend payout by 3.5% to $0.3891 per share

- Hydro One (H.TO) raised its dividend payout by 6% to $0.3142 per share

- Bank Montreal (BMO.TO) raised its dividend payout by 2.7% to $1.55 per share

- National Bank (NA.TO) raised its dividend payout by 4% to $1.10 per share

- Royal Bank (RY.TO) raised its dividend payout by 3% to $1.42 per share

These dividend hikes increased our forward annual dividend income by $395.47. At a 4% dividend yield that’s equivalent to adding $9,886.75 in new capital.

One of the disappointments for May was that the Bank of Nova Scotia skipped its traditional second-quarter dividend increase. Instead, BNS announced it would resume dividend growth in 2025. BNS came to this decision primarily because of weaker earnings caused by a rise in loan loss provisions. Considering BNS already has a very high initial yield of over 6.5%, I applauded BNS for making this tough decision. I’d rather BNS focus on getting its balance sheet in order instead of raising dividend payout.

On the other hand, I was surprised that Telus raised the dividend payout by 3.5%, in expectation of their previous guidance. Given that Telus has a high level of debt already and its share price has been hammered in the last few years, it would make more sense to stop raising its dividends and get its balance sheet in check. Interestingly, Telus CEO, Darren Entwistle, announced that he would receive salary in shares indefinitely. Entwistle’s move from cash salary to shares was interesting as it showed that the CEO is confident in Telus and aligns his interest with that of Telus shareholders.

Moving from TD Direct Investing & Questrade to Wealthsimple Trade

The big news for us in May was that I decided to move my self-directed TFSA with TD Direct Investing and my self-directed RRSP with Questrade to Wealthsimple Trade.

We have been using Wealthsimple Trade for kids’ investing portfolios and have been pretty happy with Wealthsimple Trade. So when I saw Wealthsimple Trade was running a transfer bonus promotion and I’d receive over $2,500 transfer bonus for transferring both of my accounts to Wealthsimple, it was very difficult to ignore (the promotion is closed but I wouldn’t be surprised if Wealthsimple started something similar again soon).

I also wanted to move both TFSA and RRSP to Wealthsimple to take advantage of the fractional DRIP. Other than maxing out my TFSA at the beginning of the year and using the new contribution to buy dividend stocks, I don’t make other transactions in my TFSA. Similarly, I have stopped contributing to my self-directed RRSP and focused on contributing to the spousal RRSP. Therefore, I’d only make a few transactions in my RRSP each year.

Enabling fractional DRIP in TFSA and RRSP will allow both accounts to continue to compound slightly more via DRIP.

At the time of writing, the in-kind transfers have been completed but further residual sweeps still need to be performed. So far, I have been extremely pleased with Wealthsimple Trade. I plan to write about my transferring experience in another blog post later.

Since the transfer bonus would count toward RRSP and TFSA contributions if it was deposited in these accounts, I decided to open a non-registered account with Wealthsimple Trade to avoid any potential headaches.

We may consider moving Mrs. T’s TFSA and non-registered account from Questrade to Wealthsimple Trade to take advantage of the transfer bonus and the fractional DRIP. Transferring a non-registered account is a little bit more complicated since we need to make sure the book share (i.e. adjusted cost basis) calculations are done correctly or we’d end up with potential tax consequences.

Wealthsimple has my vote of confidence. In case you’re thinking of opening an account with Wealhsimple or transferring your existing account over to Wealthsimple, you can use my referral code. You’ll get a $25 reward for simply signing up. If you become a Premium or Generation client within 30 days, you’ll get an additional $250 or $1,000 in rewards respectively.

Stock Transactions

In addition to transferring my TFSA and RRSP to Wealthsimple, we have been very busy on the buying front. We purchased the following shares throughout May:

- 26.585 shares of Waste Connections

- 81.695 shares of Telus

Over $7,500 of new capital was deployed in May. Some of that money was from the Wealthsimple transfer bonus and some was from residual cash from dividend payouts.

These transactions added $157.56 toward our annual dividend income.

As you can see from the factional share purchases, we took advantage of Wealthsimple’s fractional purchase feature right away.

Dividend Reinvestment Plan (DRIP)

Enrolling in dividend reinvestment plans allows us to put our dividend portfolio on autopilot and drip additional shares at every dividend payout. This is an excellent way to dollar average through time.

By transferring my TFSA and RRSP to Wealthsimple and enrolling in fractional DRIP, we no longer have to accumulate enough shares to ensure that we have enough dividends to buy a full share. This is especially great for stocks that we don’t own enough shares to buy a full share, like Apple, Costco, and Waste Management.

This is one of the reasons why we may consider transferring Mrs. T’s accounts in-kind to Wealthsimple later on.

In May we dripped the following shares:

- 0.417 shares of Apple

- 3 shares of Bank of Montreal

- 3 shares of Emera

- 4 shares of National Bank

- 5 shares of Royal Bank

- 0.358 shares of Starbucks

- 7 shares of SmartCentres REIT

- 0.046 share of Waste Connection

- 0.211 shares of Wal-Mart

We dripped 23.032 shares in total. $2,192.56 out of the $ 3,323.66 dividends received was invested right away, resulting in a DRIP ratio of 65.97%. We anticipate the DRIP ratio to increase slowly over time as we drip more fractional shares.

Thanks to DRIP we increased our forward annual dividend income by $87.62.

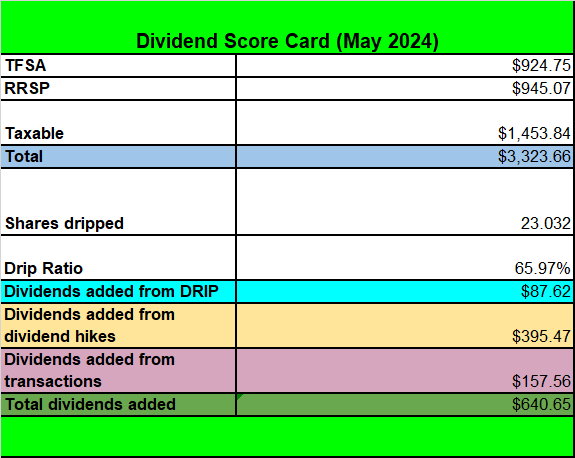

Dividend Score Card – May 2024

Here’s our dividend score card for May 2024

Overall, a very solid month especially adding almost $650 in forward annual dividend income.

Summary – Dividend Income May 2024 Update

After five months, we have received a total of $23,899.11 in dividend income.

It’s really neat to see that we already exceeded the annual total dividend income from 2019 and we are only five months down. Needless to say, we have come a long way in our dividend investing journey, especially in the last five years or so.

To put things into perspective, $23,899.11 after five months is equivalent of:

- Earning $157.23 per day or $6.55 per hour regardless of what we’re doing

- $1086.32 weekly salary or $27.16 in hourly wage

Considering BC’s minimum wage is $17.50 per hour, our dividend portfolio is now generating more money than an entry-level job!

We continue to feel blessed and appreciative that we started our investing journey so many years ago after our financial epiphany. We also recognize that we are in a very privileged position to be able to earn, save, and invest each month and not live paycheque to paycheque. This is why one of my missions for this blog is to provide support and guidance to all my readers. If you have any questions, feel free to ask in the comment section or email me.

Happy investing everyone!

Hi Bob,

I am very doubtful that Telus would be able to recover their share price. The company keeps issuing new shares to fund their dividend and this concerns me, as I am new investor of Telus and just added my positions recently due to attrative share price and juicy yield. But in the long term, i don’t know if I would regret it and better keep my money in other low yield high div growth stock. What do you think about Telus’s future?

I don’t really want to give a bold statement about Telus. I do see them recover once interest rates go down a bit and they finish deploying their 5G network. But yes, other low yield high div growth stocks might be a solid idea since total return is important.

Hello Tawcan,

Thanks for this update on you and your family’s recent travels to Denmark, and other countries in Europe. I really enjoyed all the pictures, and the descriptions of the events!

Thanks also for an update on the dividends. Clearly your dividend strategy is doing very well.

This week’s article also described the switch of some of your accounts to Wealthsimple Trade. This was very enlightening. Question for you: Are you being compensated by Wealthsimple for promoting Wealthsimple? This would be other than the payments they are providing to move accounts over from a different brokerage, and the payments when other people open accounts using your referral code.

If you are receiving compensation, even non-monetary compensation, to be honest with your readers this compensation should be disclosed. Disclosure increases your credibility.

Please let us know. Thanks!

Hi Daniel,

You’re very welcome, glad you enjoyed all the pictures.

I am no way compensated by Wealthsimple for promoting Wealthsimple. I have no association with Wealthsimple. If I were to receive compensation from Wealthsimple, I would definitely provided a disclosure. I hope that clears up.

Thanks Bob. I appreciate this!

Dan

You’re very welcome. Good point you raised. Transparency is important.

Just moved to wealth simple as well. Just wondering how often do they do the “sweeps” do you need to request it or it’s automatic?

How long after transferring your accounts into you started to get the 0.5% monthly payments?

I did request WS to do a sweep but looks like they did it automatically a few times.

Sorry, what did you mean by the 0.5% monthly payments?

The 0.5% match promotion.

Maybe it’s different than the current promotion.

The Current promo they will pay out monthly over 1 year so 12 times.

How long did you wait before requesting a sweep?

I requested a sweep about 2 weeks after the transfer was completed and I noticed that dividends were being deposited in my old accounts.

Do you have any limitation in the choice of stocks you can buy (CAD or US) with Wealthsimple?

Their DRIP with fractional shares is quite nice.

For dual listed stocks (like RY and TD), you can only trade the TSX ones. That’s the only limitation I’ve encountered.

Yea, I love Weatlhsimple. I did the transfer from Questrade to WS in January and have no regrets. The only downside is that there’s no Norbert’s Gambit, but other than that, the rest totally destroys Questrade out of the water.

Agree that no Norbert’s Gambit is inconvenient.

Great trip. So Denmark never adopted the Euro? I wonder why being such a small economy?

Lots of memories for the kids. Do they have EU passports? I made sure my daughter got her EU passport through Ireland as my dad was from Ireland. Last year we spent a month on the family farm in Ireland and she loved the cows and animals. We plan to go back frequently.

I’ll have to check out wealthsimple as RBC website is so dated with fees

Thanks! Finland is the only Scandinavian country that adopted the Euro.

Yup the kids have Danish passport. I’m the only one that doesn’t have an EU passport unfortunately.

Hi Bob,

Looks like a fantastic trip to Europe.

Thanks for sharing.

I transferred some funds as well to Wealthsimple and got an iPhone.

I sold it and reinvested in my accounts.

I am impressed with WealthSimple. The response time is a little slower but when you get to the premium level things get better. You can also earn extra income from lending your stock out, which is cool. No extra work and a little extra income.

I look forward to what else they can come up with.

You’re very welcome. Good move on getting a new iPhone from Wealthsimple. So far I’m very impressed with Wealthsimple as well.

just looking into WS, from Questrade. Mike mentioned, “You can also earn extra income from lending your stock out, which is cool. No extra work and a little extra income.”

Now I am wondering, what is the downside to it? Taxes etc ? Interesting to know a bit more about this….

We have stock lending turned off by default. You can see more info here:

https://www.wealthsimple.com/en-ca/learn/what-is-securities-lending

https://help.wealthsimple.com/hc/en-ca/articles/9509140050587-Participate-in-Stock-Lending

Hope this helps.