Can you believe that 2024 is already halfway over? What happened to the time?

I don’t know about you, as I get older, time seems to go by faster and faster. The reason seems to be how we perceive the world around us. When you are five years old, 1 year equals 20% of your life; When you are ten, 1 year is 10% of your life; When you are fifty, 1 year is only 2% of your life. So as we get older, each day, month, and year represents a smaller and smaller fraction of our lives. As a result, we perceive the year going by faster and faster.

Weird right?

For those of you who remember, we hopped on a plane and headed to Europe at the end of April. We then spent the entire month of May in Europe, visiting friends and family.

We had a lot of fun in Denmark and had a lot of family get-togethers and parties. Most of these get-togethers and parties are all-day events (the Danes know how to party!). They either start around lunchtime or early afternoon and then go till midnight or later. These get-togethers and parties meant a lot of food and drinks, and also a lot of signing (it’s a Scandinavian thing).

We spent over six weeks in Denmark for this trip, the longest Danish visit we have ever had. It was nice that I could work remotely from Denmark for most of that time.

We left Denmark in early June, took advantage of Iceland Air’s free stop, and spent seven nights in Iceland before returning to Vancouver.

Iceland was so stunning with fascinating landscapes. Below are a few pictures from our Iceland trip. I will have a proper trip report post later.

After over seven weeks away from home, we were happy to finally get back home and sleep in our own beds.

Because we were gone for more than seven weeks, our yard and backyard garden had turned into a massive jungle. This meant both Mrs. T and I spent a lot of time weeding and tending the yard.

Then at the end of June, I spent three days at a leadership training course in downtown Vancouver. This was the second face-to-face session for the leadership training (and the last one). It was great to see co-workers from all over the world again and it felt that all 16 of us really connected and we have become a close-knitted group.

Dividend Income – June 2024

Back to the dividend report…. In June we received dividends from the following companies:

- Brookfield Asset Management (BAM.TO)

- BlackRock (BLK)

- Brookfield Renewable Corp (BEPC.TO)

- Brookfield Corporation (BN.TO)

- Canadian National Railway (CNR.TO)

- Canadian Tire (CTC.A

- Enbridge (ENB.TO)

- Fortis (FTS.TO)

- Alphabet (GOOGL)

- Granite REIT (GRT.UN)

- Hydro One (H.TO)

- Intact Financial (IFC.TO)

- Johnson & Johnson (JNJ)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- PepsiCo (PEP)

- Qualcomm (QCOM)

- SmartCentres REIT (SRU.UN)

- Target (TGT)

- Visa (V)

- Waste Management (WM)

- iShares ex-Canada international ETF (XAW)

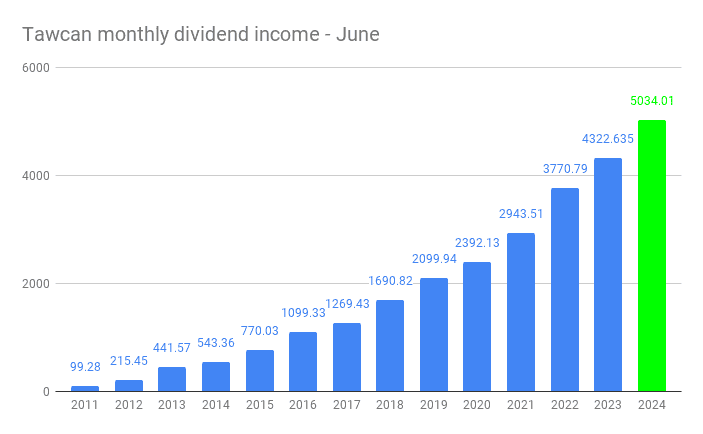

These 22 dividend payments totaled $5,034.01. I was very happy that this was our third month in 2024 with over $5,000 in dividend income.

Compared to the previous quarter (April), we saw a 21.7% growth. This was mostly from receiving XAW’s bi-annual distribution which bumped up June’s dividend total.

When we compare dividend income from June 2023, we saw a 16.46% YoY increase. This showed that we have been successful in growing our dividend income by adding new capital, growing dividends organically, and growing dividends via dividend reinvestment plans.

Dividend Hikes

Like previous years, June was a relatively quiet month in terms of dividend hikes. Throughout June, we checked to see if any companies raised dividend payouts. We ended June with Target being the only company that announced a dividend hike (a measly 1.8%).

This single dividend hike increased our forward annual dividend income by $5.04.

It’s a very small amount of money but it’s better than nothing. Furthermore, after adding $395.47 toward our forward annual dividend income in May via dividend hikes, it is somewhat expected to be a bit quieter the following month.

Dividend Reinvestment Plans (DRIP)

As mentioned last month, we transferred my self-directed TFSA with TD Direct Investing and my self-directed RRSP with Questrade to Wealthsimple Trade. We made these moves mostly to take advantage of Wealthsimple’s transfer bonus promotion (we received over $2,500 in bonus). But we also wanted to use Wealthsimple Trade to take advantage of the fractional DRIP feature to allow both accounts to compound every single quarter regardless of whether we receive enough dividends to DRIP a full share or not.

In case you’re thinking of opening an account with Wealhsimple or transferring your existing account over to Wealthsimple, you can use my referral code. You’ll get a $25 reward for simply signing up. If you become a Premium or Generation client within 30 days, you’ll get an additional $250 or $1,000 in rewards respectively.

In June we dripped the following shares:

- 1 share of Brookfield Asset Management

- 3.571 shares of Brookfield Renewable Corp

- 0.089 shares of BlackRock

- 43.012 shares of Enbridge

- 3 shares of Fortis

- 0.059 shares of Alphabet

- 0.518 shares of Granite REIT

- 1 share of Hydro One

- 1.91 shares of Coca-Cola

- 0.297 shares of McDonald

- 10.385 shares of Manulife

- 0.444 shares of PepsiCo

- 0.067 shares of Qualcomm

- 7 shares of SmartCentres REIT

- 0.42 shares of Target

- 0.056 shares of Visa

- 0.162 shares of Waste Management

- 17.076 shared of XAW

In total, 90.118 shares were dripped automatically and $4,272.84 out of the $5,034.01 was invested immediately or a DRIP ratio of 84.9%.

This DRIP ratio was the highest in 2024 so far, thanks to enabling fractional DRIP with Wealthsimple. I plan to move Mrs. T’s TFSA and possibly the non-registered account(s) to Wealthsimple when there’s another appealing promotion (The current 1% cash match promotion doesn’t interest me too much. And hopefully Wealthsimple can support self-managed spousal RRSP soon).

By reinvesting our dividends and purchasing shares right away, we added $238.80 toward our annual forward dividend.

Stock Transactions

Despite being away from home for almost half of June, we have been quite busy on the stock transaction front throughout June.

After reviewing and analyzing performance over the last few years, I closed out Johnson & Johnson and Starbucks.

Both JNJ and SBUX share prices have been a bit disappointing for the last five years as both companies faced many challenges. When I analyzed both stocks and the dividend yield, I figured our money could provide a better total return when invested elsewhere.

With the money from the sales of JNJ and Starbucks and some new capital, we added the following stocks:

- 48.502 shares of National Bank

- 135.126 shares of XAW

- 27.881 shares of GOOGL

- 21.817 shares of QQQ

We added more National Bank shares during the week that the acquisition of Canadian Western Bank was announced. National Bank’s share price dropped that week and we thought it provided an excellent opportunity for us to add more shares. I like how NA is acquiring CWB to accelerate growth in western Canada. Since the purchase, the share price has recovered a little bit. I have no doubt that National Bank will do just fine long term.

We added more XAW and QQQ because we want to increase our international exposure and asset diversification. XAW and QQQ both have seen decent performance over the last five years and I’m optimistic that both will continue to see solid performance in the future.

All these transactions added about $318.60 toward our forward annual dividend income.

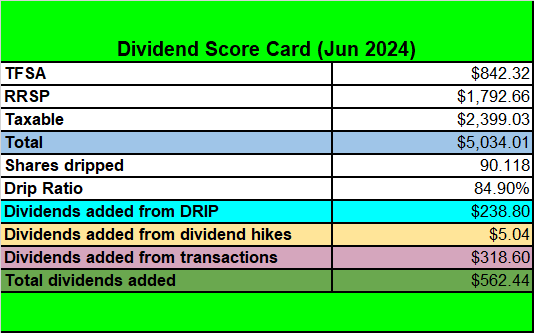

Dividend Score Card – June 2024

Here’s our dividend score card for June 2024. As mentioned, we had the highest DRIP ratio in 2024 so I was quite pleased.

Despite closing out JNJ and SBUX, we still managed to net $318.60 from all the dividend transactions. Amazing stuff!

2024 Mid-Year Review

With 1H 2024 wrapped up, it’s the perfect time for a midyear review.

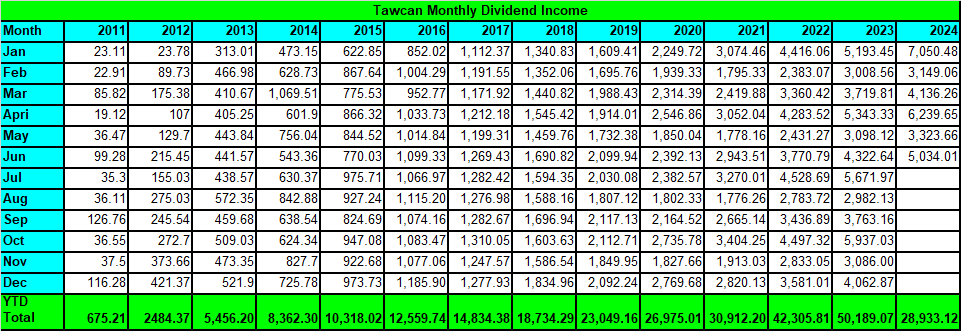

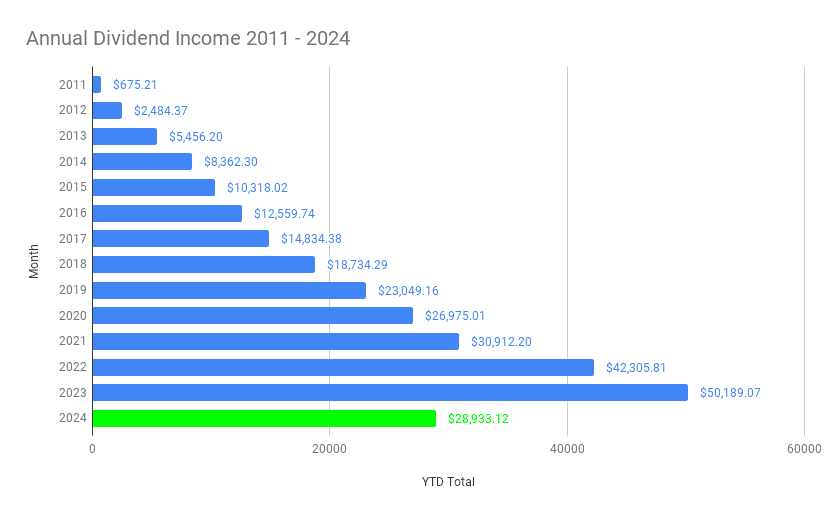

After six months, we received $28,933.12 in dividend income. Compared to the same period last year, we saw a growth of 17.2%.

Excluding new contributions, our dividend portfolio returned 9.12%. In comparison, VCN had a 6.69% return, XAW had a 15.25% return, and XEQT had a 12.6% return. When I reviewed our portfolio, I noticed that BMO, TD, BNS, CM, Telus, and BCE have dragged down our portfolio performance. Clearly, we need to focus more on total return. Hence we’ve been purchasing more low yield stocks that hopefully will generate a better total return and higher dividend growth.

Having said that, since stocks are typically cyclical, I believe these low performance stocks will turn around when interest rates start to go down again…

In the first half of 2024, we added $3,906.20 toward our forward dividend income from a combination of new capital, organic growth, and DRIP. The detailed breakdown:

- New capital: $1,500.32

- Organic growth: $1,243.94

- DRIP: $1,161.91

In case you’re wondering, we added just over $42,000 worth of new capital into our dividend portfolio in the first half of the year. Please note that not all that money was saved from this year alone. Some of the money, like this year’s TFSA and RRSP contributions, was saved from the second half of last year.

Regardless of when the money was saved, we still contributed a lot of money so far this year. We are very thankful of our relatively high savings rate.

Financial Independence Journey Progress

When we first started our financial independence journey, our goal was to live off dividends when we retire early. However, this goal has morphed over the years. Although we still plan to live off dividends in some form, we plan to supplement our dividend income with part time work and possibly sell some shares. The idea is to utilize our dividend income to provide flexibility – allow us to be picky on what kind of part time work we want to do.

The $28,933.12 dividend income in the first half of 2024 was able to cover over 152.7% of our necessities spending. Necessities spending includes core spending like food, insurance, utilities, property taxes, clothing, car, etc. Necessities do not include things like eating out, charitable donations, vacations, gifts, and entertainment.

It was comforting to see that our dividend income could cover our necessities comfortably. However, our dividend income did not cover 100% of our total spending due to some big expenses we had throughout the first half of 2024.

Due to two growing kids and us wanting to spend more money to create memory dividends, I have come to accept that our dividend income will not cover our total spending for the next little while.

But that’s totally OK. The memories and experiences we gained from our travels and eating healthier are way more beneficial than penny-pinching and not enjoying our lives.

Summary – Dividend Income June 2024 Update

We have made significant progress with our dividend income in the last ten years, especially the last five years. It’s really amazing to see our progress visually.

With 2024 only halfway over, we already exceeded the total annual dividend income from 2020, which is absolutely mindblowing.

To put things in perspective, $28,933.12 is equivalent of:

- Earning $158.97 per day or $6.62 per hour

- $1,112.81 per working week or $27.82 per hour after 26 working weeks.

We are very thankful that we’re doing very well financially and having a relatively high savings rate. We continue to donate money to local charities each month and volunteer in the community regularly. I also believe it is important to continue sharing our FI journey here and all the things we have learned along the way so others don’t make the same mistakes as we have.

Thank you everyone for continuing to support this blog. I really appreciate it.

Happy investing everyone!

I appreciate you sharing your journey with us. As a Canadian, that worked part time with a family most of my life, I have discovered my CPP will be quite small when I do retire. Is this a concern for you and your wife when you do choose to retire or move to part time work?

Hi Tara,

We have always considered CPP and OAS as extra gravy and not included in our retirement calculations. Hope this helps.

“Although we still plan to live off dividends in some form, we plan to supplement our dividend income with part time work and possibly sell some shares. The idea is to utilize our dividend income to provide flexibility – allow us to be picky on what kind of part time work we want to do.”

Have you firmed up any plans on when you’re planning to pull the plug on full-time work and go part-time?

(Congrats on all your continued success!)

That’s a good question, haven’t decided yet. Will see how things unfold. 🙂

Hi, could you elaborate a bit more on your experience using WEalth Simple vs Questrade. I quite like Questrade but dont like their high transaction fees ($5). I also use Interactive brokers. What are the Pros of Cons of using Questrade Vs. Wealth Simple.

I would like to move to IB or Wealth Simple, but am also hesitant on putting all my investments with one broker. It would be great if you can do a comparison of all the Stock brokers in Canada

I like both Questrade and Wealthsimple, they each have their advantages and disadvantages.

Wealthsimple is good if you are contributing regularly with a small amount of money and you want to buy/drip fractional shares.

Questrade has advantages when it comes to dual listed stocks, exchanging between USD/CAD, and better research tools.

If you are concerned about Questrade’s transaction fees ($5 isn’t that high honestly), then Wealthsimple is an excellent choice. Would always appreciate if you use my referral code. 🙂

Hope this helps.

I recently moved all funds to WealthSimple from Questrade. I actually prefer QT as a trading platform but WS is fine. I never really used the research tools but the interface is better.

I wanted the free 1% match on my transfer which is quite a chunk on a 7-figure portfolio. So I’ll wait a year and collect my 1% then likely move my RRSP and LIRA back to QT for one main reason, Nordbert’s gambit. Exchanging money on WS is too costly and my retirement accounts will hold a fair bit of USD.

My TFSA, non-reg, and chequing account I will likely leave with WS as they will mostly hold dividend paying Canadian assets. I’m getting a great interest rate on cash in my chequing and no-fee trades in the investment accounts, it’s a good platform.

Hi Tawcan,

I recently came across your blog and found your ETF investing guide incredibly helpful and informative. As a new investor working on building my TFSA portfolio, I’m considering the following allocation: 45% XEQT, 30% VFV, 20% XEI, and 5% ZRE.

I’d love to hear your thoughts on this approach.

Thanks!

Hi Ryan,

Thank you. Is there a reason why you picked 4 different ETFs instead of just relying on XEQT? There are a bit of overlap between these ETFs.

Hi Tawcan,

Sorry for the late response. I thought by investing in 4 ETF I would be diversifying my Portfolio. The XEQT would be a Universal ETF where it have global exposure, VFV follow the S&P 500 in the US, XEI will be good for dividend, and ZRE will be good exposure to the Real Estate in Canada. Do you think this is a good idea or should I just invest solely on XEQT?

Hi Ryan,

You can certainly go with 4 of these ETFs, my only concern is there are a bit of overlapping between the different ETFs. I’d have no problem going with XEQT only but if you want to have a bit more focus in S&P 500 and dividends, your method is good too. If I had to be picky, I’d probably drop ZRE and go with 3 ETFs only.

Hi Tawcan,

Thank you for the feedback and for pointing out the overlap. If I decide to go with just XEQT, what other investment options would you recommend to diversify my portfolio further?

I think you can go with XEQT and VFV and leave it at that. If you want to go with dividends, I’d build up your portfolio first, then buy individual dividend stocks. Generally speaking I don’t like dividend ETFs.

I enjoyed reading about your trip and your investments…what a way to mix it up! I am a newbie to dividends and I am very reluctant to purchase still, for fear of a poor investment and being an uneducated investor. I wonder, in order to make that much on dividends what would the initial investment be approximately? I just don’t know where to start. I have tried to dabble in penny stocks on the TD trade as well and have done horribly. I would love to take a class or have someone I can trust to guide me.

Hi Cynthia,

Thank you. If you’re new and are hesitant about investing, I’d suggest buying one of the all-in-one ETFs (https://tawcan.com/all-in-one-etfs-canada/) to get started. I’d not dabble in penny stocks at all.

I do offer coaching service (https://tawcan.com/coaching/) for all levels of investors.

Congrats on another solid month of results, but I disagreed with your move to sell JNJ and SBUX. I think what you are doing is still timing the market and I have leant this big mistake over my 25 yrs of investing journey. If I have never sold one shares of any companies that I bought over the years including the losers, my result would be so much better. Not sure if you know the facts there were more than dozens of companies with AAA credit ratings 20 yrs ago now it is only down to 2 with that solid credit rating. They are MSFT and JNJ. The whole pharmaceutical sector isn’t doing too well if you look at many out there like PFE , BMY, GSK, or even ABBV or MERK. I think it is the whole sector weakness and overtime health care is still solid defensive sectors that provide steady and growing stream of cash flow. If you look at BCE, another major laggard, is still outperforming QQQ from 2000 to 2024 (now). You just need to understand the facts that dividend counts 40-50% of your return, especially growing dividend which are put back into DRIP.

Thank you for your input, definitely something to think about when you look at investments with a longer timeline.

Im all-in on dividend investing. That said the recent growth has been startling. Had I sold-in-May-and-gone-away I would have missed an incredible recent surge. The growth blows away the dividends.

My point is I think a better approach, for me, would have been a more balanced portfolio of growth oriented shares/etf’s and dividend investments

That said, Im thankful for the long term benefits of my investments and wont be changing strategies now.

Total return is definitely important. 🙂

Any issues with the schools and taking the kids out for 2 months? Did they do homework or have assignments?

We took our daughter out for travel but for maximum of 3 weeks.

Travel deals are always better outside the summer season

We were home schooling both kids the last school year so it wasn’t an issue at all.

Thank you so much! I just started my investing from last month. I have been reading your posts which is very helpful to gather knowledge and guidance.

You’re very welcome.

I track my expenses on a yearly basis, to ensure that spending is less than income. What I wonder about is the value of tracking the yearly increase of spending, to predict a more realistic outcome?

I think tracking expenses is important so you can develop a trend. Obviously some categories may increase over the years, especially when you have kids. 🙂

What type of promotion would you hope for vs a 1% match? That is a nice chunk of free money.

I too am interested in knowing what he’d favour over the current 1% offer. I’m just about ready to pull the trigger of moving our Margin and TFSA’s over to WealthSimple.

Yes the 1% match is nice but I don’t like it because:

1. The money gets deposited into the Cash account over 12 months

2. The interest earned is taxed at 100% of your marginal tax rate

I’d rather get the money deposited in the investment account and can use it immediately. But maybe that’s just me. 🙂

Don’t get me wrong, I was looking at the 1% offer for Mrs. T’s accounts but just have been hesitant due to the reasons above.

I don’t think there is any tax on the bonus. If you leave it in the cash account you will pay on the interest though.

I simply transfer the money into my non-reg investment as soon as the bonus hits my account.

That’s what I meant… tax on the interest.

That’s a good point about moving money into your investment account right away. Hmmm something to look into for sure. Thanks for pointing it out.