I hope everyone is enjoying the last bit of summer (or winter if you’re in the Southern Hemisphere). Because we were in Denmark and Iceland for over 7 weeks starting at the end of April and had nice sunny and warm weather, it feels like we are having an extended summer this year.

While Vancouver has very long daylight hours during the summer months, both Denmark and Iceland have much longer daylight hours than Vancouver. So it was strange for us to be in Vancouver and experiencing “shorter” daylight hours.

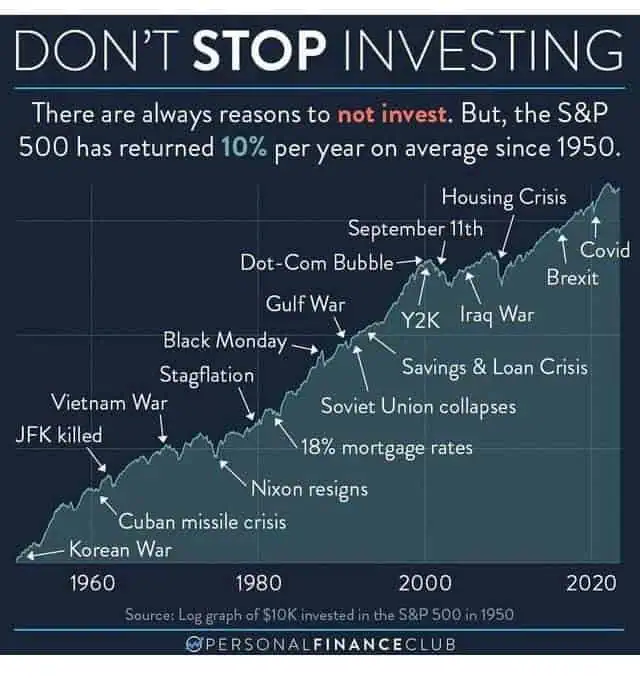

The stock market has been very volatile lately and people are freaking out about the massive daily slides. During my relatively short investing career (around 18 years), I have seen the market go up up up and down down down. One important lesson I’ve learned over the years – stay on course and stick with your investment strategy.

Don’t believe me? The chart below gives a very good visual representation of why it’s important to stay on course.

Remember, it’s time in the market, not timing the market!

In July, housework kept us quite occupied.

First, we got our house exterior painted by a local company. Although the cost was quite high (~$10k), our house desperately needed a fresh coat of paint. The original plan was to spray two coats of paint but that was changed because the wood panels were too dry. So the painters ended up painting the entire exterior of the house by hand to ensure a good amount of paint was applied. As a result, the paint job went from three days to five and a half days with three or four painters working about nine hours each day.

The house looks brand new after the paint job and we were very happy to get the house painted!

For the last year or so, both kids have been asking to have their own rooms instead of sharing a room. After much consideration, we repurposed the guest bedroom and gave both kids separate rooms. A bit of painting and decoration were involved to make sure the rooms were set up to both kids’ liking. It also meant we had to go to Ikea and buy over $350 worth of new furniture.

July was not too kind to our wallets, that’s for sure.

Long time readers will recall that we have a backyard garden so it shouldn’t come as a surprise that we spent a lot of time tending the garden throughout the month and enjoyed the fruits of our labours.

We are very fortunate to have my parents close by so they can look after the kids from time to time. So one Friday night in July, Mrs. T and I sent the kids for a sleepover at my parents’ house so we could have a much needed date night.

After rushing to Vancouver and navigating through Friday rush hour traffic, we had an awesome dinner at Minami, one of the top Japanese restaurants in Vancouver. After dinner, we enjoyed the Vancouver Symphony Orchestra playing the Pirates of the Caribbean (basically we watched the movie with the orchestra playing all the music live). We wrapped up the date with delicious ice cream at Mister Artisan Ice Cream. Considering we haven’t had a kids-free time in a very long time, the date night was much needed.

It’d be nice to have more date nights with Mrs. T… we just need to convince both kids to spend the night with my parents (they don’t like to be away from us for the night… a result of the pandemic we think…)

Dividend Income – July 2024

Anyway, back to the main topic of the blog post… dividend income report.

In July we received dividends from the following companies:

- Alimentation Couche-Tard (ATD.TO)

- BCE Inc (BCE.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Capital Power Corp (CPX.TO)

- Granite REIT (GRT.UN)

- Coca-Cola (KO)

- SmartCentres REIT (SRU.UN)

- Telus (T.TO)

- TD (TD.TO)

- TC Energy Corp (TRP.TO)

- VICI Properties (VICI)

- Invesco QQQ ETF (QQQ)

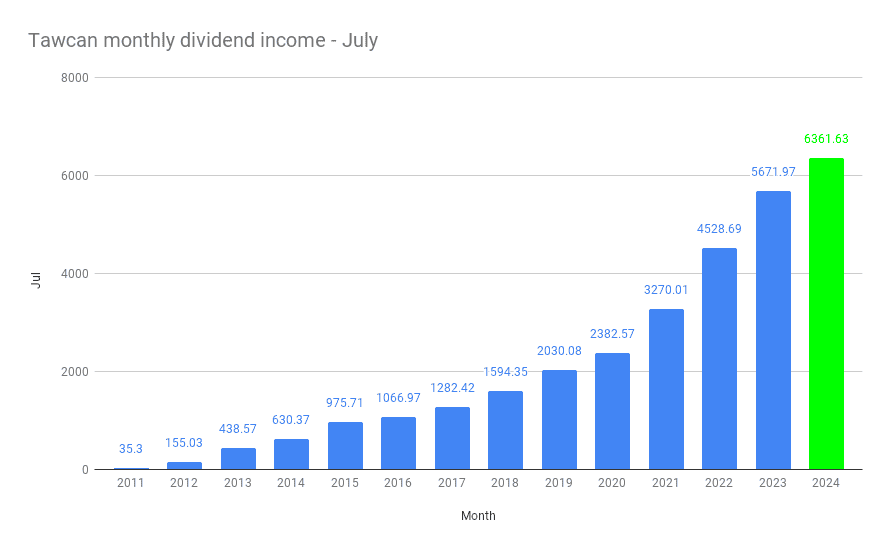

The 14 dividend paycheques added up to $6,361.63. Another month of over $6,000 in dividend income! It was nice to see that July’s dividend income was the second highest amount so far this year.

Compared to July 2023, we saw a YoY dividend growth of 12.16%. This is a respectable number knowing that we are facing the law of big numbers.

For July of 2024, we received dividends from Algonquin Power & Utilities, Dream Industrial REIT, and RioCan REIT. However, we closed all three positions and reinvested the money elsewhere. Most of the YoY dividend growth came from reinvesting money from stock sales or injections of new cash.

Dividend Hikes

For a while, it seemed that we wouldn’t see any dividend hikes in July. Then on the second last day of July, Capital Power announced a 6% dividend increase. This was a pleasant surprise.

The single dividend hike increased our forward dividend income by $6.09.

Not a huge amount of money but it’s better than nothing.

Dividend Reinvestment Plans (DRIP)

Currently, we use TD Direct Investing, Questrade, and Wealthsimple Trade for our dividend portfolio. For TD and Questrade, we enroll in synthetic DRIPs to buy one or more full shares with dividends received whenever we’re eligible. For Wealthsimple Trade, we turned on fractional DRIP so 100% of the dividends are reinvested immediately.

TD Direct Investing honours DRIP discounts so we can get a 2-5% discount on dripped share price depending on the stock. The only minor annoyance is that it’d often take one to two weeks for the dividends and DRIP to settle and show up in the account. Meanwhile, Questrade and Wealthsimple drip at market price so we don’t get DRIP discounts.

For now, we are dripping all of our dividends and reinvesting the leftover dividends. We probably will turn off drip a year or two before we plan to live off dividends. Turning off drip would allow us to build up our cash reserves. In many ways, this “cash reserve” could be considered as our emergency fund to give us a bit more margin of safety when we are relying on our portfolio to pay for living expenses.

In July we dripped the following shares:

- 22.338 shares of BCE

- 10.494 shares of Bank of Nova Scotia

- 12.397 shares of CIBC

- 2.308 shares of Capital Power Corp

- 0.481 shares of Granite REIT

- 7 shares of SmartCentres REIT

- 14.963 shares of Telus

- 14.369 shares of TD

- 13.186 shares of TC Energy Corp

- 2.723 shares of VICI Properties

A total of 100.259 shares was dripped with $5,159.51 out of the $6,361.63 reinvested right away, resulting in a DRIP ratio of 81.1%.

More importantly, enrolling in DRIP increased our forward annual dividend by $460.88.

Stock Transactions

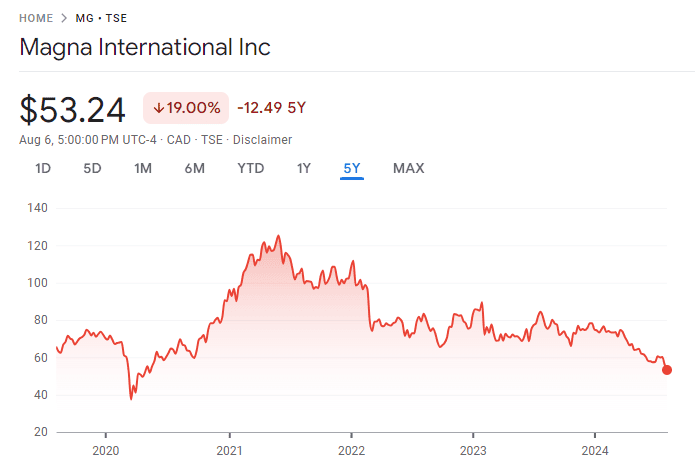

In keeping up with the idea of consolidating our dividend portfolio, we decided to close out our position in Magna International.

Magna International was the smallest position in our portfolio. Due to the Ukraine-Russia war, MG’s share price had taken a big hit.

In some ways, I regret not selling Magna International earlier around 2021 but hindsight is always 20/20. Magna had terrible second quarter results so I guess we dodged a bullet by closing out this position before the quarterly results.

With money from closing out MG, new capital, and money from dividends, we purchased the following shares:

- 8 shares of Royal Bank

- 55 shares of Brookfield Asset Management

We bought a few more shares of Royal Bank to bring it back up to be in the top five spot in our dividend portfolio. Another reason for buying more shares is to capture the August dividend payment before the ex-dividend date.

Brookfield Asset Management has been firing on all cylinders lately and we continue to like the company a lot. Since BAM is still a relatively small position in our portfolio, we bought more shares to increase the weighting slightly.

These three transactions netted $56.84 toward our forward annual dividend income.

Random Thoughts on the Market

As mentioned earlier, it’s important to take a step back and look at the big picture. This is especially true whenever there’s a market downturn that makes everyone a bit nervous.

Why is this an important lesson? Because when it comes to investing, time is an important and valuable ally. The longer you stay in the market, the higher chance you can ride out the volatility and end up on the positive side.

Here’s a great example I found…

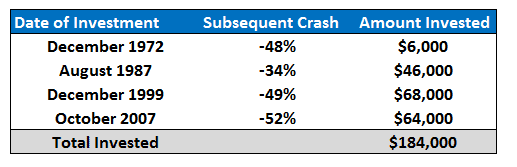

Imagine you are the world’s worst market timer and always invest in stocks or index ETFs at market peaks. Welcome to Bob (not me), the world’s worst market timer.

In 1970, Bob started saving $2,000 a year in his bank account earning 0% interest. Because Bob didn’t feel comfortable with investing money in the stock market regularly, he waited until December 1972 after the market had a huge run-up before investing his money in the S&P index fund.

Unfortunately, the market dropped nearly 50% in 1973-1974. Instead of existing and selling all of his shares, Bob stayed in the market and continued to save.

Although Bob continued to save money, he didn’t feel comfortable adding more shares of the index fund until August 1987 after another huge bull run. He added $46,000 worth of S&P index ETF. As his luck had it, his purchase was immediately followed by a 30% market crash.

Again Bob didn’t sell a single share and continued to save. After the crash in 1987, Bob didn’t invest new money in the market until the end of 1999. At the end of 1999, Bob added $68,000 to the S&P index ETF. Once again, the market crashed in December 1999 and didn’t recover until 2002.

Bob didn’t sell any shares and continued to save. He then made a final purchase of $65,000 in October 2007, just before the financial crisis.

After the financial crisis, Bob felt it was best to leave his savings in the bank, not touch his investments, and not buy more shares of the S&P index ETF.

Despite terrible timing, because Bob didn’t sell a single share and stayed in the market, he ended up with $1.1 million by the time he retired at the end of 2013.

Here’s the total amount that Bob invested starting in 1972:

Because Bob stayed invested in the market for over 40 years, didn’t sell a single share, and let his money compound over time, he ended up with $1.1 million when he retired

Could Bob end up with more money? Sure thing! If Bob had periodically invested his money throughout the years, he’d end up with $2.5 million instead.

Lessons learned here?

- I can’t stress this enough. Time in the market is your biggest ally. You can buy stocks or ETFs with terrible timing but if you can ride it out over decades, you will almost always end up with some gains at the end

- Dollar cost averaging is extremely powerful. Contributing regularly would result in more than $1.4 million for Bob.

- The market will go up and the market will go down. However, over the long term, the market has a tendency to go up. Saving your money regularly, investing regularly, taking advantage of compounding, and thinking long term will help you to build wealth.

This is why it’s extremely important to invest with money you don’t need for at least the next three to five years. Because that way you won’t be forced to sell at the worst possible time. Can you imagine investing with your house down payment only to have to sell in mid-March 2020 when the market is at the bottom of the pandemic downturn?

Investing is all about looking at the long term and letting your money compound. Although many people think dividends are irrelevant, I truly believe receiving regular dividend payments helps with the investment psyche tremendously – having steady dividend pay cheques prevents you from focusing on your portfolio value and prevents you from wanting to sell your investments whenever there’s a market downturn.

Yes, I do check our portfolio regularly but I sleep well at night knowing that our portfolio will continue to grow over the long term. The market will be volatile in the short term and it’s not possible to avoid these 10%, 15%, 20%, or even 25% swings. It’s important to stick with your investment strategy and focus on the long term results.

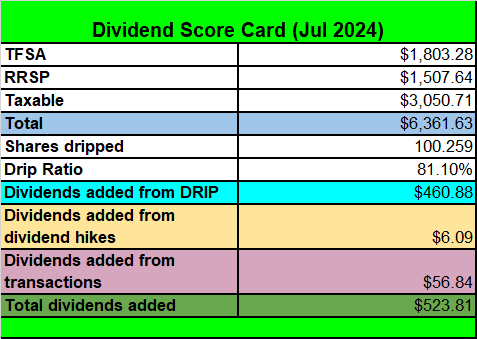

Dividend Score Card – July 2024

Here’s our dividend score card for July 2024.

Overall I think we did relatively well, especially with adding over $460 of forward annual dividend income from DRIP.

Summary – Dividend Income July 2024 Update

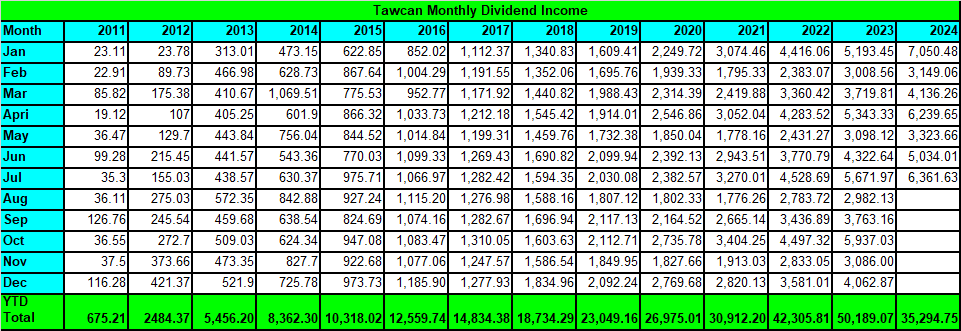

After seven months we have collected a total of $35,294.75 in dividends.

It’s pretty amazing that we are probably two months away from passing our 2022 annual dividend income total. Compounding is really an amazing thing.

To put things in perspective, $35,294.75 is equivalent of:

- Earning $165.70 per day or $6.90 per hour, regardless of what we’re doing

- $1,138.54 per working week or $28.46 per hour after 31 working weeks.

Considering that BC’s minimum wage is $17.40 per hour, if you work at a minimum-wage job for 40 hours a week, after 52 weeks you’d earn a total of $36,192. It’s pretty amazing to know that our dividend portfolio is now generating at a faster pace than a minimum wage job. Mrs. T and I are extremely thankful and grateful that we started our financial independence journey back in 2011 and started taking serious charge of our finances.

Happy investing everyone!

Good move on AQN – I was holding on to a bit hoping they’d come around and then boom – another dividend cut and the stock dropped even more. Painful!

Agreed that AQN has been extremely painful. It was difficult to take the loss but sometimes it is necessary to just take the loss and move on.

Good morning. Are you at all nervous about turning off your DRIPs 1-2 years prior to retirement?

I ask because I’m about 2 years away from retiring. I’ve been using DRIPs for 30 years, so the idea of turning off the DRIP feature and simply accumulating my dividends rather than having them automatically re-invested is causing me some cognitive discomfort. Truth be told, the idea makes my stomach queasy. Even though I know it’s a rational move and that building up a buffer is a sensible course of action, I still have a significant feeling of apprehension that my dividends will be “stagnating” in my account, that they would be “being eaten up by inflation”, and that I’d be making a mistake by not re-investing them.

Do you ever have these feelings? (Or do any of your readers?) If so, then what tips, advice, and/or self-talk have helped you to overcome these feelings?

Thanks in advance!

so Close to your retirement, you would be shifting to a heavy mix of bonds vs stocks anyway, so dont think foregoing dividend reinvestment for a couple of years to buy insurance against volatility and market downturns is really bad in the grand scheme of things

Hi Blue Lobster,

No I’m not worried about that at all. We will eventually turn off DRIP and build up our cash reserves. I totally understand why you’d have some concerns though. 🙂

Theres one thing I wanted to call out that media and corporations generally tend to underplay and dismiss is the risks associated with the Stock market. Time in the market works ONLY when you carefully review the investment and make decisions based on data related to the Company/Sector business, financial performance, competitive differentiator, innovation and so on. Often MOST of the people tend to take financial and investment decisions based on media hype which will set you up for failure.

People tend to say Stock markets always go up over time which is true but REMEMBER, its the Stock indexes which keep going up all the time because the indexes flush out losers and replace them with winners. So Yes, obviously the Stock market ie the indexes will ALWAYS go up BUT individual stocks can and will fail. You need to avoid being swept away by hype and DONT EVER think you are going to get rich overnight. Investment takes time, patience and careful review to choose the right investments. Otherwise as they say “a fool and his money are soon parted”

And one final thing please diversify your investments. Dont have all your eggs in the Stock market.

Good luck!!

Yes diversification is important.

The house and garden look great!

Love to see how the monthly dividend income bar graph shows so well your progress since 2011.

Thank you Pierre.

Hey, love your Dividend journey. I really enjoy reading your blog about investing. I just open my FHSA and was wondering if you have any recommended ETF I should invest for my FHSA. I’m looking to buy my first home in 3 years. I was thinking about puting 50% Cash.to and 50% VFV. Any suggestions will be great!

Hi Tommy,

If you’re thinking of buying your first home in 3 years, I’d not put too much money in equity. Probably want to look something like VBAL or XBAL where you have a higher percentage in bonds.

HI, are you willing to share where you reinvested after selling Algonquin, Dream Industrial REIT, and RioCan REIT ? Thanks.

We have shared in the different monthly dividend reports. Quite a list of different stocks we bought but basically stocks like TD, XAW, ATD, RY, ENB, and TRP.

Wait, did I miss something. Why did you dispose of RioCan REIT? Did you write an article I missed about it? If so, can you please provide the link that will explain, thanks Bob!

We closed out RioCan last year. Please see post here – https://tawcan.com/dividend-income-july-2023-update/

Love the volatility. I am a timer in the market as it’s rewarding to get a bargain .

Also I have lots of cash in MM ETF’s.

Thanks to this site I was made aware of QQC.

So the week of 6 Aug I loaded up on QQC and got into BNS . Also for C$ I’ve been getting more CNR, CP, BMO and BN.

US$ side also getting more tech with QQQ, MSFT, DIA etf.

Looking for more corrections in September/Oct with the US election and proposals from Kamala to massively increase capital gains taxes and other taxes. Likely a lot of capital gains selling if she wins.

But who knows , usually the opposite happens of my predictions!

It should be interesting heading up to the US election. Volatility is good for folks building their portfolio.

Amazing dividends. The YoY growth is great.

Enjoy your time in Denmark and Iceland. It’s great that you can take a long vacation like that.

Thank you Joe. Denmark & Iceland were excellent.