Happy New Year everyone! I hope everyone had a fantastic 2024 and enjoyed the holidays. I sure did.

The market was on fire in 2024 and we’ll have to wait and see whether we will see a repeat in 2025 or not. Since we are still in the accumulating phase, I’m secretly wishing for a bear market so we can purchase stocks and ETFs at a discount. (I won’t say that I’m unhappy about two consecutive years of markets being up more than 20%!)

Since August 2014, I have written a dividend income update every single month. This is my way to demonstrate that it is possible to build up a sizable investment portfolio over time as well as a way to keep myself accountable.

It’s hard to believe I have written 125 dividend income updates so far!

In typical fashion, work was quite busy in December and required me to pull multiple 12-hour days. I had to remind myself this was only temporary and that I would enjoy the 1.5 weeks off in the last part of December.

As in years past when we spent Christmas in Vancouver (we have been celebrating Christmas in Denmark every third year), we prepared for this magical holiday throughout December by finding a Christmas tree, decorating the tree, and making cookies and chocolate.

In mid-December, we had a seven-hour open house party with friends. Due to a powerful windstorm, the power went off that morning and we ended up having the open house party in the dark. Being resourceful, we scattered the living room, the dining room, and the kitchen with LED candles, regular candles, and camping LED lanterns for lighting.

Around 75 adults and kids were at the open house throughout the seven hours (not all at once fortunately). We even had the folks from the radio station Move 103.5 dropping by for their annual party-crashing event. Despite having no power at all, the open house party was a lot of fun with lots of memories.

Before the holidays, I caught up with long time university friends (one was visiting from Australia and stayed with us for one night). As we are all in our early 40s, we commented about each other’s grey hair (some of us are hiding it better than others).

We hosted Christmas dinner this year and had amazing food. Rather than giving each other gifts, we tried something different this year with the adults by playing the dice gift game. Basically, each adult would bring one or two presents. All the presents were put in the middle, whenever a six was rolled, the person could pick a gift. After the initial round, we’d play for a set time and this time people could steal gifts from each other. We then unwrapped the gifts and played another round. All the adults had fun and we agreed to do it again next time.

Meanwhile, the kids received gifts from their Santa wish list…

Overall, we had a nice and relaxing break over the holidays with a lot of hygge, good food, cookies, chocolate, and of course caffeinated drinks. What a great way to wrap up a great year.

Dividend Income – December 2024

In December we received dividend payments from the following companies:

- Alimentation Couche-Tard (ATD.TO)

- Brookfield Asset Management (BAM.TO)

- BlackRock (BLK)

- Brookfield Renewable Corp (BEPC.TO)

- Brookfield Corporation (BN.TO)

- Canadian National Railway (CNR.TO)

- Canadian Tire (CTC.A)

- Enbridge (ENB.TO)

- Fortis (FTS.TO)

- Google (GOOGL)

- Granite REIT (GRT.UN)

- Hydro One (H.TO)

- Intact Financial (IFC.TO)

- Coca-Cola (KO)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- Qualcomm (QCOM)

- SmartCentres REIT (SRU.UN)

- Target (TGT)

- Visa (V)

- Waste Connections (WCN.TO)

- Waste Management (WM)

- Invesco QQQM (QQQM)

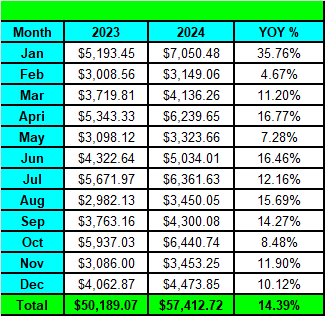

The 23 payments added up to $4,473.85. What a great way to wrap up the year!

Compared to December 2023 we saw a YoY growth of 10.12% which is a respectable number.

Dividend Hikes

December was a strong month when it came to dividend hikes. We saw the following companies raising their dividend payouts:

- Waste Management (WM) raised its dividend payout by 10% to $0.825 per share

- Enbridge (ENB.TO) raised its dividend payout by 3% to $0.9425 per share

- Royal Bank (RY.TO) raised its dividend payout by 4% to $1.48 per share

- National Bank (NA.TO) raised its dividend payout by 3.4% to $1.14 per share

- CIBC (CM.TO) raised its dividend payout by 7.9% to $0.97 per share

- Bank of Montreal (BMO.TO) raised its dividend payout by 2.58% to $1.59 per share

- TD (TD.TO) raised its dividend payout by 2.9% to $1.05 per share

These seven dividend hikes increased our annual dividend income by $1,913.00. Love it!

When we tally up all the dividend hikes for the entire 2024, we saw an increase in our annual dividend income of $3,511.07. At a 4% dividend yield, that’s equivalent to adding $87,776.75 of new capital. Pretty amazing stuff if you ask me.

Dividend Reinvestment Plans (DRIP)

We utilize DRIP to increase our forward annual dividend income. With Questrade and TD, we signed up for synthetic DRIP whenever we are eligible so we can drip at least one share at each dividend payout period. With Wealthsimple Trade, we enable fractional DRIP so all dividends are used to get additional shares.

- Sign up for Wealthsimple with my referral code or type in YDC3NA when you sign up. You’ll get a $25 reward for simply signing up.

- Sign up for Questrade with my referral code and receive $50.

In December we dripped the following shares:

- 1 share of Brookfield Asset Management

- 3 shares of Brookfield Renewable Corp

- 0.07 shares of BlackRock

- 0.268 shares of Canadian Tire

- 36.34 shares of Enbridge

- 3 shares of Fortis

- 0.08 shares of Alphabet

- 0.487 shares of Granite REIT

- 1.957 shares of Coca-Cola

- 0.21 shares of McDonald’s

- 9.1983 shares of Manulife Financial

- 0.097 shares of Qualcomm

- 0.078 shares of Invesco QQQ

- 6 shares of SmartCentres REIT

- 0.525 shares of Target

- 0.055 shares of Visa

- 0.165 shares of Waste Management

Thanks to DRIP we added 62.576 shares in December and added $190.17 toward our forward annual dividend income.

Wrapping up 2024, we added $2,617.28 to our forward annual dividend thanks to enrolling in DRIP. This is quite amazing if you consider it’d take $65,432 of fresh capital at a 4% dividend yield.

Stock Transactions

Unlike October and November, we had a few minor stock transactions in December.

First, we decided to do a small tax loss harvesting in my non-registered account by selling 153 shares of BCE. This is to offset part of the capital gains from the sale of my company’s restricted stock units (RSUs).

Given the unstable condition of BCE, it is also our way to reduce our exposure to BCE. We may slowly trim our BCE shares over time.

I also moved my portion of the money from my work’s group RRSP to my self-directed RRSP at Wealthsimple.

With the money from these two transactions, we then purchased the following:

- 152.8386 of iShares ex-Canada International ETF (XAW)

- 75.6416 of Brookfield Corporation (BN.TO)

We purchased more XAW to increase our international exposure. I believe XAW is a simple and cost-effective way to increase our dividend portfolio’s exposure outside of Canada. XAW trades in CAD so we don’t have to worry about currency exchange.

We also added some BN shares to increase our exposure to Brookfield Corporation. A lot of the top financial experts and hedge fund managers like Bill Ackman and Steve Cohen have been buying BN shares because they believe it is undervalued. I tend to agree with these experts. Although BN’s dividend yield is extremely low, the attraction lies in the potential total return. With Bruce Flatt in charge of the Brookfield empire, I am confident he and his team will continue to grow the empire, generate revenues, and increase the share price.

These transactions reduced our forward annual dividend by $23.70.

In addition to these transactions, we decided to switch from QQQ to QQQM to save us a little of in MER fees. I explained why QQQM is better compared to QQQ long term.

Dividend Scorecard – December 2024

Here’s our dividend scorecard for December:

Overall, a good way to end the year, especially considering we added over $2,000 in forward annual dividend in one month. I am not paying too much attention to the small forward dividend loss from transactions because we reduced a high-yield payer, BCE, and invested the money in XAW and BN which have lower yields.

2024 Stock Transactions Summary

We made many transactions throughout 2024 and I always share them on my monthly dividend income reports. Here’s a quick summary of our stock transactions:

Sold

- 46 shares of MRU in January (closed position)

- 125 shares of Suncor in January (closed position)

- 10 shares of Canadian Tire in March

- 50.3581 shares of Starbucks in June (closed position)

- 112.946 shares of Johnson & Johnson in June (closed position)

- 38 shares of Magna International in August (closed position)

- 153 shares of BCE in December

Purchased

- 70 shares of National Bank in January

- 93 shares of Alimentation Couche-Tard in January

- 30 shares of QQQ in January

- 130 shares of TC Energy Corp in March

- 128 shares of XAW in March

- 46 shares of TD in April

- 21 shares of Brookfield Asset Management in April

- 7 shares of Visa in April

- 26.585 shares of Waste Connections in May

- 75.146 shares of Telus in May

- 48.502 shares of National Bank in June

- 135.126 shares of XAW in June

- 27.881 shares of Alphabet in June

- 21.817 shares of QQQ in June

- 8 shares of Royal Bank in July

- 55 shares of Brookfield Asset Management in August

- 94.862 shares of Canadian National Resources in August

- 28.5496 shares of XAW in August

- 6.0079 shares of Waste Connections in August

- 92.6356 shares of Canadian National Resources in September

- 152.8386 shares of XAW in December

- 75.6416 shares of Brookfield Corporation in December

We closed 6 positions in total and added shares to our existing positions. The only new position we added was QQQ (or QQQM now we have swapped).

Is there a trend in all our transactions? I think so. We diversified by adding QQQ and XAW. We also tried to increase our portfolio exposure to some low yield stocks like Alimentation Couche-Tard, Brookfield Asset Management, Alphabet, Brookfield Corporation, and Waste Connections.

Total return matters so we want to keep this in mind whenever we purchase stocks and ETFs.

One key lesson learned? Do not focus too much on the initial yield. The higher the yield, the higher the risk. If a stock has a very high yield due to share price retreating over time, there’s probably a reason for that. If one decides to chase yield, understand the risk and be OK to face potential paper loss for the short to medium term.

2024 Organic Dividend Growth & DRIP

As our dividend income gets bigger, we need to rely on organic dividend growth (i.e. dividend hikes) and DRIP to grow our forward annual dividend.

In 2024 we added $6,128.35 in forward annual dividend thanks to organic dividend growth & DRIP.

I started tracking these two metrics more closely in 2022 and you can see our performance in the last three years.

| Year | DRIP$ | Organic dividend Growth $ | Total $ | % increase YoY |

| 2022 | $1,450.21 | $2,367.36 | $3,817.57 | N/A |

| 2023 | $2,104.99 | $2,401.14 | $4,596.13 | 20.4% |

| 2024 | $2,617.28 | $3,511.07 | $6,128.35 | 34.1% |

It’s pretty neat to see the total amount increasing year over year and the percentage increase has gotten bigger each year.

At a 4% yield, adding $6,128.35 in forward annual dividend is equivalent to adding $153,208.75 in fresh capital. This is an example of our money working hard for us so we don’t have to.

2024 Total Dividends

In 2024, we received a total of $57,412.72 in dividend income. It has been an incredible journey knowing that in 2020 we only received $26,975.01. In other words, in four years, we have more than doubled our dividend income!

Going from $50,189.07 to $57,412.72 meant a YoY increase of 14.39%. Although it’s below 15%, a higher than 10% YoY is very solid knowing that our dividend income is sizable already.

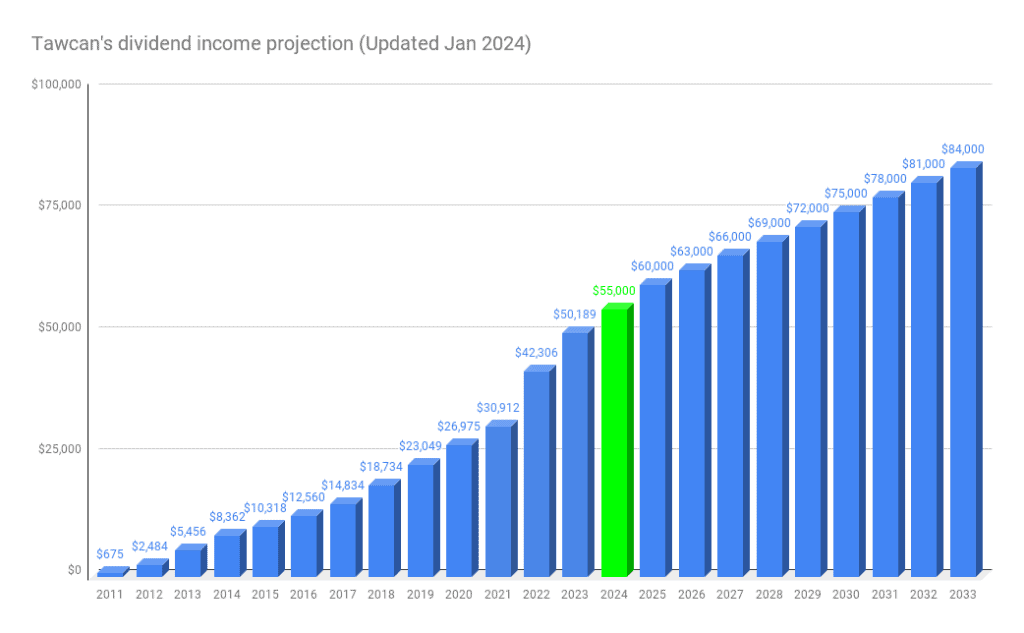

We successfully accomplished our goal of receiving $55,000 in dividend income so I am very pleased with our progress.

As you can see from the dividend income projection I did in January 2024, we are ahead of the projection.

2024 Dividend Income Breakdown

Long term readers may recall that our goal every year is to max out both TFSAs and RRSPs. Once both these registered accounts are maxed out, we then start investing in non-registered accounts. We focus on registered accounts first so most of our dividend income is either tax-free or tax-deferred. For non-registered accounts, we only invest in Canadian companies that pay eligible dividends to get the best tax treatment.

Our 2024 dividend income breakdown was as follows:

| Accounts | $ Amount | % |

| RRSP | $16,246.60 | 28.3% |

| TFSA | $14,207.36 | 24.7% |

| Non-registered | $26,958.76 | 47.0% |

Visual breakdown:

In other words, 53% of our dividend income was either tax-advantaged or tax-deferred. Only 47% of our dividend income was taxed.

But not all the non-registered dividend income was taxed under me. In fact, the non-registered dividend income is shared between Mrs. T and I at about a 35-65 breakdown. Since Canadian dividends have preferential treatment compared to regular income, they’re taxed at a lower rate than regular working income.

2024 Portfolio Return

In 2024 our portfolio, excluding new contributions, returned 30.4%. In comparison, the TSX had a +17.99% return, the S&P 500 had a +23.31 return, and the NASDAQ had a +28.64% return.

Needless to say, 2024 was amazing for the equity market.

We would have had a higher return if it wasn’t for the likes of BCE, TD, Canadian National Railway, McDonald’s, and Telus that dragged down the performance. On the other hand, we are fortunate to own the likes of Apple, QQQ/QQQM, Brookfield Asset Management, Brookfield Corporation, and CIBC which have outperformed the market.

You win some and you lose some!

Here’s our portfolio return since 2012.

| Portfolio return excluding contribution | TSX return | S&P 500 return | |

| 2012 | +8.67% | +4.0% | +13.41% |

| 2013 | +33.04% | +9.55% | +29.6% |

| 2014 | +24.08% | +7.42% | +11.39% |

| 2015 | -5.97% | -11.09% | -0.73% |

| 2016 | +19.62% | +17.51% | +9.54% |

| 2017 | +12.33% | +6.03% | +19.42% |

| 2018 | -2.38% | -11.64% | -6.24% |

| 2019 | +11.32% | +19.13% | +28.88% |

| 2020 | +3.2% | +2.17% | +16.26% |

| 2021 | +32.8% | +21.74% | +26.89% |

| 2022 | -5.4% | -8.66% | -19.44% |

| 2023 | +10.48% | +7.79% | +24.73% |

| 2024 | +30.4% | +17.99% | +23.31% |

| Averages | +13.25% | +6.30% | +13.62% |

Note, I took out the new contribution each year when calculating the annual return of our portfolio.

Financial Independence Journey Progress

In 2024 our dividend income was able to cover 127.9% of our Necessities.

Here’s our budget system in case you’re curious.

The budget system we use breaks down our after-tax income into six different accounts and allocates a certain percentage for each account. A few years ago we modified the accounts slightly and we now only have five accounts.

- Necessities

- Give

- Play

- Long Term Savings for Spending

- Financial Freedom Account

The Necessities account includes expenses like groceries, mortgage, property tax, household expenses, car insurance, car gas, utilities, and health expenses.

The Give account includes expenses like gifts and charitable donations.

The Play account includes expenses like eating out, wellness (like massages, pedicure, facial, etc), movies & entertainment, hobbies, and skiing.

The Long Term Savings for Spendings account is an account that we put money aside for spending later. For example, vacations, kids’ RESPs, large purchases, and business expenses.

Financial Freedom Account is used to pay ourselves first. Money set aside for FFA is used for investing and growing our nest eggs.

It was really nice to see that our 2024 dividend income covered more than 100% of our Necessities. Since the Necessities account doesn’t include other extra expenses, we aren’t quite ready to live off dividends yet…. But we are getting closer and closer to this goal!

Summary & Looking ahead

It’s pretty amazing how much progress we have made since our financial epiphany in 2011 and we started focusing on dividend growth investing. Not only did we accomplish our goal of receiving $55,000 in dividend income in 2024, we exceeded the amount by 4.39%.

Amazing stuff!

At $57,412.72, our 2024 dividend income was equivalent to:

- $156.86 per day or $6.54 per jour

- $1,104.09 per working week or $27.60 per hour

We are very grateful to have started taking charge of our investments in 2011 and that our dividend portfolio is now generating enough money that’s above BC’s minimum wage.

Rome wasn’t built in one day, and neither should your investment portfolio. Brick by brick. Patience will pay off in the long run.

How was your December 2024 dividend income? How much dividend income did you receive for 2024?

Hey Bob! Been a while, hope this comment finds you well.

I noticed that you reduced your BCE position and mentioned that you might reduce more later. I understand that you used it to offset other capital gains, but I’m debating about buying more BCE now that it’s “on sale”.

The way I see it, all telecoms have gotten hammered, not just Bell, granted not as much as Bell, but my thoughts are, its a Canadian staple stock, I can’t see that company going out of business and I’m pondering whether keeping it or even adding to my position might pay off way later down the road (ie. as in years from now) ?

Wondering your thoughts.

Yes, all telecom have gotten hammered but BCE’s balance sheet is not looking great. There’s a good chance for BCE to cut its dividends later this year or early next year.

Hey Bob, a request if possible. There are so many of us which include many Canadian PF bloggers on BlueSky now. Could you add a social sharing link to your blog so I can share your posts there, thanks.

Love the open house Christmas come and go party idea, that looks like it was a wonderful time.

Let me look into that. Unfortunately someone took my name on Bluesky so I can’t sign myself up as Tawcan.

Wow, what amazing progress Tawcan! You had a giant jump in dividends in 2022 – is that from a very large influx of fresh cash?

Yes we bought a lot of stocks during COVID time.

HelloTawcan, thank you for this detailed report and analysis.

Questions for you: a) In the “annual performance since 2012”, does the portfolio return include dividends, commissions, and currency exchange?; b) Does the TSX return include dividends?; and c) Does the S&P return include dividends and consider currency exchange?

Thanks very much.

Tsx and S&p returns do not include dividends.If you include dividends then you’ll see about 2-3% additional return.

Our portfolio return includes everything.

Three years since thinking of dividends

All annual numbers

2022 – $1,195

2023 – $3,384

2024 – $5,260 (very similar to your first three years actually lol)

It seems so far away from the ~$50K I would need to meet my minimum expenses (esp if I factor in inflation), but like you said, brick by brick in 10~15 years I’ll get there

It takes time to build up a dividend portfolio, be patient.

What an inspiration! Keep it going!! Question- why not buy into an ETF like VDY and spare some risk instead of individual stocks?

Fingers crossed I can keep investing like I’ve been and double my divs by YE. So far I should be around $4K in divs – hoping for more!

Thank you. Do we own ETFs like XAW and QQQM for diversification purposes. No dividend ETFs so it’s easier to predict dividends.

Great progress! Looking forward to 2025 blogs.

Happy New Year

Happy new year to you too.

Honest question from an amateur just a few years into the FIRE.

Is it wise to DRIP a share that you bought super low but has increased by triple digits?

There’s nothing wrong with averaging up. If the stock continues to do well over time, it’s nice to drip additional shares and ride it upwards.

Great end to a solid year! Congratulations! 🙂

I received $15,183.44 in dividends for 2024. Getting there brick by brick!

Thank you. Congrats on a solid year!