Hello everyone, welcome to another monthly dividend income update.

We are doing these monthly dividend income updates to chronicle our financial independence journey. I believe these monthly updates demonstrate that it is possible to build up a sizable dividend portfolio which will allow us to one day live off dividends.

While living off dividends is our goal, it doesn’t mean we will not touch our principal. The idea is to utilize part-time work income and dividends during the first five years of our financial independence. It’s very possible that we can live off dividends completely and not touch our principal. However, I believe it’s important to slowly dip into our principal over time for estate planning reasons.

We don’t plan to stop working completely because the idea doesn’t sound very enticing to either one of us. We plan to keep ourselves occupied in some fashion. We plan to pass down some assets to our kids and their kids but at the same time create as many memory dividends as possible outlined in Die With Zero.

This is why total return is important. Dividend income isn’t “free” money – companies need to generate enough cash to pay dividends. The best scenario is for companies to pay dividends, continue to raise dividends each year, and have the share price appreciate over time.

For me, April was a busy travel month.

First I went to Taiwan, China, and Hong Kong. To maximize my time in the region, I had many internal & external meetings and work-related lunches & dinners. When I had free time in the evening, I walked around and explored.

Then one and a half weeks after my Asia trip, I hopped on an early flight to Newark. After visiting customers in New Jersey and the Long Island area, I flew down from LaGuardia Airport to Atlanta late Tuesday night. I visited customers in Atlanta all day Wednesday before getting on a flight back to Vancouver on Thursday morning. Since there were no direct flights from Atlanta, I had to connect via Montreal, so it took all day to get back to Vancouver.

And the travelling wasn’t done just yet! The week after my East Coast trip I got on another flight headed to Europe for another work trip visiting customers in different countries… (more on that in another post later).

Fortunately, whenever I was at home, I spent time with Mrs. T and both kids and enjoyed their company. We even went to Brickcan to check out some fantastic Lego custom-made sets.

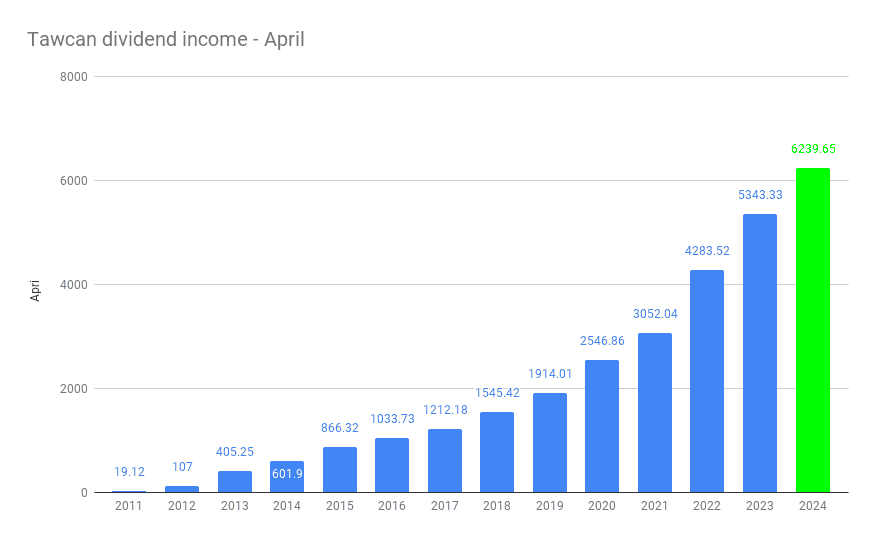

Dividend Income – April 2024

April is one of the strong months for us and we received dividends from the following companies:

- Alimentation Couche-Tard (ATD.TO)

- BCE Inc (BEC.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Capital Power Corp (CPX.TO)

- Granite REIT (GRT.UN)

- Coca-Cola (KO)

- PepsiCo (PEP)

- SmartCentres REIT (SRU.UN)

- Telus (T.TO)

- TD (TD.TO)

- TC Energy Corp (TRP.TO)

- VICI Properties (VICI)

- Wal-Mart (WMT)

- Invesco QQQ Nasdaq 100 index (QQQ)

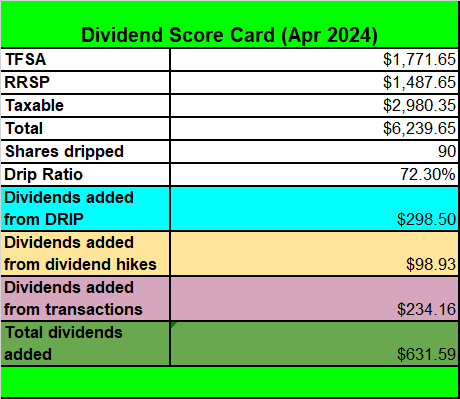

The 16 dividend pay cheques resulted in $6,239.65 of dividend income in April.

It was an excellent month and our April dividend income covered 100% of our total expenses. This is the second straight month that our dividend income covered more than 100% of our monthly expenses!

Compared to April 2023, we saw a YoY dividend growth of 16.77%. After four months, we are averaging 17.1% YoY dividend growth.

Last April, we received dividend payments from Algonquin Power & Utilities Corp (AQN.TO), Dream Industrial REIT (DIR.UN), RioCan REIT (REI.UN) totalling $448.75. We closed these positions last year and reinvested the money elsewhere. For example, we invested some of the money in Alimentation Couche-Tard.

Some of the 16.77% dividend growth came from organic dividend growth and DRIP but most of the growth came from adding new capital and purchasing more shares of TD, Telus, and BCE throughout 2023.

Dividend Hikes

The following companies announced dividend hikes in April:

- Procter & Gamble (PG) raised its dividend payout by 6.99% to $1.0065 per share

- Costco (COST) raised its dividend payout by 13.7% to $1.16 per share

- Johnson & Johnson (JNJ) raised its dividend payout by 4.2% to $1.24 per share

In addition to these dividend hikes, Alphabet (GOOG, GOOGL) announced the initiation of a cash dividend program, paying a dividend of $0.20 per share.

I was very pleased to see Alphabet starting to pay dividends. But that means the number of holdings in our dividend portfolio went from 44 to 45. (Note: GOOGL was in our “play non-dividend portfolio” so we didn’t count it as one of the dividend holdings)This makes my goal of reducing our holdings to 40 by the end of 2024 more challenging.

In case you’re wondering, we purchased Alphabet shares in 2011.

Then in late 2014, Google announced a 2 for 1 split. Two classes of shares were created – the voting class GOOGL shares and the non-voting class shares GOOG.

After receiving my shares of GOOG, I decided to sell them and only hold onto my GOOGL shares. In my mind, I thought it wasn’t worth holding onto no-voting shares. More importantly, for some stupid reasons, I thought Google had stopped growing and stopped innovating.

Boy, that was one heck of a mistake! (Having said that, I used the money from GOOG to buy Visa and Costco so I still did OK).

These announcements increased our forward annual dividend income by $98.93.

Dividend Reinvestment Plan (DRIP)

For the most part, once we initiate a position, we don’t pay very close attention to the day-to-day performance of the stock price. We focus on whether the company is growing its revenue and profitability. We also focus on whether people continue to use the company’s products. The more reliant people are on these products, the better.

When a position is initiated, we try to accumulate enough shares to enroll in synthetic DRIP (i.e. have enough dividends to buy a full share). Enrolling in DRIP enables us to put our dividend portfolio on autopilot and drip additional shares at every dividend payout, essentially dollar cost average through time.

In April we dripped the following shares:

- 14 shares of BCE

- 10 shares of Bank of Nova Scotia

- 13 shares of CIBC

- 1 share of Canadian Natural Resources

- 2 shares of Capital Power Corp

- 1 share of Coca-Cola

- 7 shares of SmartCentres REIT

- 13 shares of Telus

- 12 shares of TD

- 15 shares of TC Energy Corp

- 2 shares of VICI Properties

90 shares were added via DRIP and $4,512.7 was invested automatically without us having to lift a finger. This resulted in a DRIP ratio of 72.3% for April.

Thanks to DRIP, we added $298.50 toward our forward annual dividend income!

Stock Transactions

Our financial independence journey can be summed up in five simple words – earn, save, invest, and repeat.

In addition to my full-time job, we try to maximize our earning potential by generating side hustle incomes – Mrs. T’s doula service, my photography business, and this blog.

We try to be frugal on certain expenses like clothes, utilities, fuel, and dining out but spend money on things we value like food, trips, coffee, and chocolate. Whatever money is left over, we save for either big expenses like vacations (i.e. long term savings for spending) or invest into our investment portfolio.

Because our dividend portfolio generates a large amount of money each month and on average we reinvest about 55% of our dividend income via DRIP, cash accumulates in our investment accounts relatively quickly.

Thanks to cash accumulation in our investment accounts and our relatively high savings rate, we regularly invest new capital throughout the year.

Having said all that, we typically make most of our purchases in the first half of the year. In the second half of the year, we then go into saving mode and save money for TFSA and RRSP contributions for the following year.

With that in mind, in April we added new capital and purchased the following shares:

- 46 shares of TD

- 21 shares of Brookfield Asset Management

- 7 shares of Visa

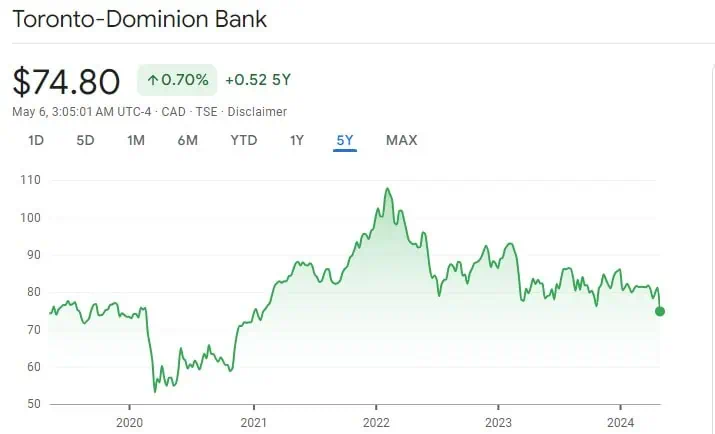

TD hasn’t done much in the last five years. Concerns with the US market and the Canadian housing market have dragged down the stock price. The drug money laundering allegations didn’t help with the share price.

However, at an initial yield of over 4.8% and a dividend history since the late 1800s, it is hard not to scoop up more TD shares, especially considering we are investing in TD for the long term.

Brookfield Asset Management and Visa are two financial juggernauts. Brookfield Asset Management has $900 billion assets under management; the Visa networks processed 212.6 billion transactions in 2023 and there are 4.3 billion Visa credit cards in the world.

These three transactions added $234.16 toward our forward annual dividend income.

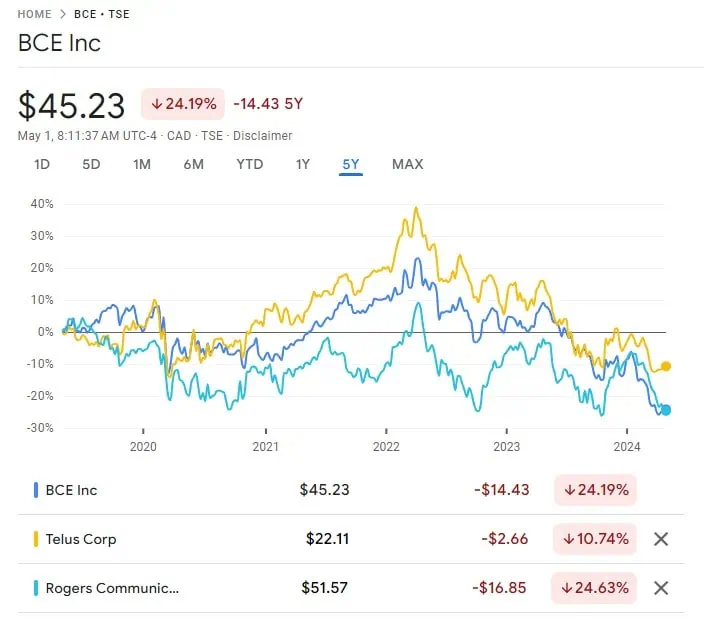

Some thoughts on BCE and Telus

All three Canadian telecommunication companies – BCE, Telus, and Rogers have seen better days from a share price point of view.

Due to the nature of the telecommunication business, all three companies have a lot of debt (long term debt: BCE at $23.07B, Telus at $17.03B, and Rogers at $29.45B). In the high interest rates environment, all three companies are paying a lot of interest on their long term debt. To make matters worse, the transition from 4G to 5G means telecoms must continue to invest money in new 5G infrastructures and build up the 5G stand alone networks across Canada.

Although BCE’s telecommunication revenue has been growing (albeit slowly), its media revenue has been declining. The declining media revenue has led to BCE selling off a lot of radio stations and cutting its media workforce.

On the other hand, Telus focuses on telecommunication but the Telus International spinoff has not done as well as anticipated, hurting Telus’ bottom line.

The biggest question for BCE and Telus shareholders – is the dividend safe?

Dan at Stocktrades recently made an excellent video on BCE:

Overall, I agree with Dan’s analysis. It is probably better for BCE to take the bandage off, cut the dividend, and ensure a healthy balance sheet (this is what 3M did recently and stopped its 6 decade dividend increase streak). The BCE board seems to want to continue its 15 year dividend streak. Rather than cutting dividends, BCE has been working to fix its balance sheet by corporate restructuring and selling off assets. For now, I think the dividend growth will slow down significantly over the next couple of years.

Does this mean we should get rid of BCE? I don’t think so. I put my trust in BCE that it will be able to navigate out of the tough waters and be OK long term.

Would I double down and buy more BCE shares? Since we added BCE shares throughout 2023, I plan to remain on the sidelines. We will continue to collect BCE dividends and drip additional BCE shares.

For now, I prefer Telus over BCE. Why? Mostly because Telus doesn’t have any media assets and focuses on high-margin businesses. Telus has additional assets like Telus Agriculture & Goods and Telus Health that could provide value to Telus shareholders. Given the Telus International spinoff hasn’t worked as well as anticipated, I believe Telus learned a few lessons before spinning off Telus Agriculture & Goods and Telus Health.

Would I buy more Telus shares? Yes. We are seriously considering adding more shares of Telus over the next few months because we believe Telus’ dividend is safe and the company should continue to grow long term.

Dividend Scorecard April 2024

Here’s our dividend scorecard for April 2024:

Overall I’m pleased with our April performance. We dripped 90 shares and added $631.59 toward our forward annual dividend income. At a 4% yield, that’s equivalent to adding $15,789.75 of new capital!!!

Looking ahead – what I’m thinking about

In February I wrote about five stocks we plan to purchase. Out of the five stocks mentioned, we have only purchased Visa so far. We have not bought any new shares of Fortis, Costco, Apple, and Enbridge mostly because there are more attractive stocks to purchase than these four.

I listed Fortis as one of the best Canadian stocks due to its proxy-like stable dividends so we may buy more Fortis shares to boost our dividend income.

Apple announced its 2Q 2024 results on May 2nd. The iPhone sales were down year over year, mostly due to slow down in China and people not upgrading phones as often as previously. However, the Services revenue continues to see very steady growth. Services revenues saw an all-time record of $23.9 billion, up 14 percent from $20.9 billion in the year-ago quarter. As we can see below, Services make up 26.3% of the Q2 revenue.

The new Apple silicons have boosted Mac sales to better than expected numbers at $7.5 billion compared to the same quarter last year at $7.17 billion. The biggest news was the monster $110 billion share buyback program (a modest dividend increase was welcomed too).

The share buyback program this size can only mean one thing – Apple believes its shares are undervalued. Does it make sense to buy more? Since Apple is one of our portfolio’s top five stocks and we have seen some sizable gains, we may dabble a few shares here and there. However, we don’t plan to buy a large number of Apple shares.

Costco’s share price keeps going up. I’d love to add more Costco shares but at the current valuation, it’s very difficult to justify adding more shares.

For Enbridge, we have been dripping 24 shares and adding about $90 toward our forward annual dividend income each quarter or almost 100 Enbridge shares and an increase of $360 in dividends annually. Adding more Enbridge shares with new capital simply may not make sense because it would further overweight our Enbridge position.

So what am I thinking about for the remainder of 2024?

As referenced earlier, we are considering adding more shares of Telus and taking advantage of the low share price. We are also considering adding more shares of Waste Connections, TD, Visa, and Alimentation Couche-Tard. I like the garbage business that Waste Connections is in. TD share price has struggled the last few years but long term I believe it will do just fine. Visa and Alimentation Couche-Tard are two stock stocks we would like to increase their weighting in our portfolio.

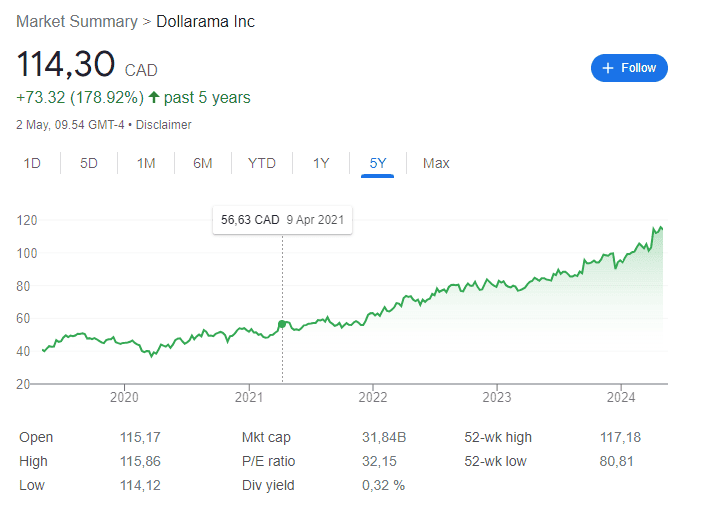

Possibly ignored by many traditional dividend investors due to the low yield, Dollarama looks interesting to me. Dollarama has a 13 year dividend increase streak with a 10 year annualized dividend growth rate of 11.7%. Not to mention the stock price has appreciated significantly over the last five years.

On the flip side, we are still considering closing out Magna International and Canadian Tire and reinvest the money elsewhere.

Summary – Dividend Income April 2024 Update

Phew, this monthly dividend income update turned out much longer than I anticipated!

To summarize, after four months we have received $20,575.45 in dividends.

To put things into perspective, this is equal to:

- $28.58 per hour working salary after 18 working weeks

- $170.05 per day or $7.08 per hour even when we’re sleeping!

When I calculated these equivalents, I am ignoring taxes for dividends in our non-registered accounts as well as taxes on any RRSP withdrawals. Why? Because it’s simply too complicated to calculate the tax rate now. I plan to take taxes into consideration when we are actually withdrawing from our accounts and utilizing our portfolio to pay for our expenses.

For now, we will continue to focus on the simple things – earn, save, invest, and repeat.

Hello Bob! Thanks for the great blog!

Looking back to your early years of investing, do you think you have done better in terms of overall return with higher paying yield stocks like ENB and BNS. Or lower yield stocks like ATD?

Hi Patrick,

Thank you. Definitely would have gotten a better return in early years. When we started we had a lot of REITs and income trusts that didn’t do much in terms of capital appreciation. Having said that we also got in early on many stocks like Apple, Waste Management, and Intact Financial that have provided multi bagger returns.

Yeah, you rock. Very nice dividends.im not a dividend investor byt live your blod posts.ive been reading for a while. I think the advantage you have with your dividend strategy vs etf with dividends automatically reinvested (like hxt or hxs) is, you can actually see when your dividends surpass your expenses. This would give me clarity when i can retire rather than doing th e complicated math.

Anyway, What are you doing with the kids resp strategy? Ive read that when interest rates on mortgages are so high, it’s smarter to just pay down the house. Would love to know your strategy.

Thanks Jonathan. For kids RESP we invest 100% in XEQT due to its simplicity.

Hi Tawcan, I think all 3 Canadian telecoms are heavily buried in debts. I don’t think Telus is better than any of the two although I heard multiples times from other financail blogger saying Telus is better shape than BCE or Roers is the best of all etc. If you look at Telus spending plan for the next 4 years and you would be shocked as where and how those money are coming from. $16 billions to be invested in Alberta, $17 billions to be invested in BC. Nevertheless, the CEO of telus also assure us that he would receive his pay cheque in Telus shares for the foreseable future. BCE CEO is telling us that the dividend is paying out of 70% of the cash flow. All these number don’t make much sense at all to me. Serving a population of just under $40 million in the 2nd largest country in the world, the Canadian government wants more competition to co-exist to bring down the price. Again where is the money coming from to expand the 5g network. USA has 10 x more population , but there is only 3 national carriers (T, VZ, TMUS) vs 4 (Rogers, BCE, Telus , Freedom/Quebecor) in Canada. China has 1.4 billions populations and they only have 3 national Carrier. I think the Canadian telecom are basically doing the same thing as most Canadians do and simply live on debts. In Vancouver, Toroonto, just housing along will suck up 90% or even over 100% of the cash flow of most families. I have no clue wha the Canadian government is doing honestly ? Do they really know what they are doing? They are killing the telecoms so they would bail them out at one point to save hundreds thousands of jobs and families out there. They just thought they were all crown corporations to begin with at one point before they were privatized. As matter of fact, Sastel is still crown corporations. If Telus or BCE cut dividend , it would impact so many people and mutual funds out there. In my utmost and honest opinion, I think they all should cut their dividend but in fact Telus just raised the dividends again by 3+%. Where are the logics? I don’t get it. The balance sheet, income statement and cash flow statement all don’t make any sense. I own all 3 of them and reason I own them is their juicy cash flow and ultility like business. Are they all hoping or begging that the interest rate would come down rapidly like many other Canadians who are struggled with their mortgage payment.

Hi Dan,

Some fair comments. US has more major cities compared to Canada so for telecom, it’d take a lot more money to invest and set up the infrastructures in comparison to a handful of major cities. But you’re right, it will be interesting to see what happens to Canadian telecom moving forward.

If I may, for the benefit of the group, if you would like to take a look at the list of Canadian dividend payers and see how they are taxed in a non-registered/cash trading account, I’ve done the research: https://canadianmoneytalk.ca/list-of-canadian-eligible-dividend-payers/

Whether the distributions are taxed as interest, foreign income, capital gains, Canadian Eligible Dividends or return of capital, makes a significant difference in taxation in a non-registered account.

I am interest to understand total return on your portfolio versus S&P 500 and TSX. Focusing on dividend as a strategy is interesting and you may be missing out on stock growth versus high dividend yield that rarely appreciated and often depreciate. I like your strategy for someone who is nearing retirement with your stock selection. IMO you would have the best of both worlds by focusing on index investing when in your 20-40’s then branch out into high yield dividend stocks in your 50’s and beyond to maximize your total portfolio return. Your missing out if your only strategy is dividends. Also diversification is key outside of stocks. RE, art, farmland, business investment, start up organizations and Bitcoin as serious investments to consider to minimize exposure to the stock market.

I am not sure about Tawcan’t total return. My own example I calculate my networth every year and my current structure is 65% dividend stock, 35% in sp500 (sp 500 etf is all i have ), 5% in cash equivalent. My total return works out to be about 15.5% annualized over the last 10 yrs vs 12.191% for sp500 with dividend reinvested. The data is pulled from dqydi.com There is no one strategy for sure win at the end of the financial journey. What works for one might not work for the other. Some people are doing just fine with 6-8% compound return. The key to success is starting early and using time and power of compound to build your wealth over time. The beauty of dividend stocks is it provide you stable and predictable income while you can solely rely on 4% rule (25x your annual expense) if you are only invested in ETF tied to the bench mark. I started my investing journey since 1999. I had been through multiple recessions and lost decade (2000-2009) where sp500 basically running flat without any gain. If you only count on 4% rule when the market is in multi-year decline, you would be in hell lot of financial trouble. Would this happen ? I can assure you it would but we don’t know when. A lot of times, people only think of return before the risks. The rate of return only matters only if your bottom line (cash flow) is growing at healthy clip.

Hi Troy,

You can see our returns over the years here – https://tawcan.com/dividend-income-december-2023-update-2023-summary/

I should probably create a page so it’s easier for readers to find.

Your comments are fair, that’s why we do invest in both dividend stocks and index ETFs.

Just to clarify you own BAM not BN?

Excellent work on the blog!

We own both BAM and BN.

Speaking of Brookfield, is there an advantage to owning BEP.UN vs BEPC?

BEPC has a corporation structure so it’s more friendly in a non-registered account. So BEPC provides a bit more flexibility compared to BEP.UN.

Thanks once again for the inspiration!

Thank you Kris. Appreciate it.

Great month! Enjoy your time at home. It sounds like a lot of travel.

Dividend income looks awesome.

Thanks Joe. It was a lot of travelling for sure.

That is some nice dividend income! And over $20K for the year is very impressive! Congrats! 🙂

Thank you My Dividend Dynasty. 🙂