When it comes to Financial Independence Retirement Early (FIRE), there are lots of calculators & simulators on the internet to estimate when one can reach FIRE. As luck have it, I also created a calculator myself. Based on my Early Retirement Financial Independence spreadsheet calculator, we should be financially independent sometimes in our 40’s. That puts a timeline of roughly 6 – 16 years.

Recently I came across a really cool spreadsheet from Chris at KeepThrifty.com. Instead of estimating when one can reach FIRE, the spreadsheet calculates a completely different scenario.

He called it “Retirement Freedom.”

What does it mean?

If you never put another penny in your retirement accounts again, could you retire safely at age 65 if you stop contributing today?

Bang! That’s Retirement Freedom!

It’s like calculating whether you have sufficient safety net if you retire at the typical retirement age of 65.

If you are not retirement free yet, the spreadsheet can figure out how much longer and how much more money you need before you become retirement free. How cool is that?

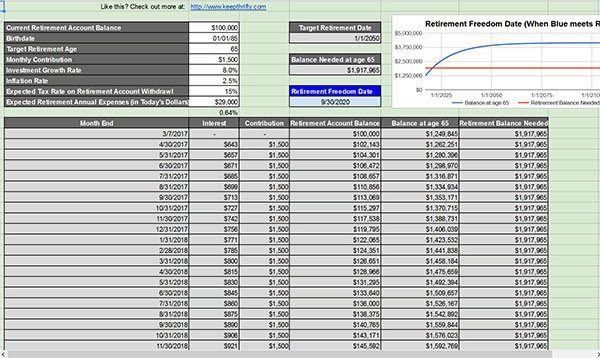

Retirement Free Excel Sheet

You can get a copy of the spreadsheet here. Once you have your own copy, you can play around with the numbers.

Where are we at?

Since I’m a HUGE Excel nerd, I went nuts with this amazing spreadsheet.

Just like any retirement spreadsheets, one of the important parameter is the Expected Retirement Annual Expenses (in today’s dollars). I decided to use $40,000 for this particular parameter per our financial independence assumptions.

The spreadsheet then calculated that the balance we need at age 65 is $2,500,955 based on the rate of return, inflation rate, and withdraw tax rate that I used.

For fun I created different scenarios to see where we stand when it comes to retirement free.

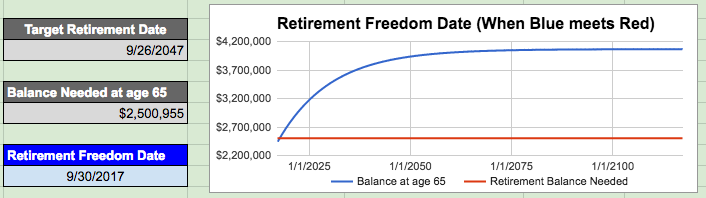

Scenario #1 – RRSP only

For the first scenario I only used our RRSP portfolio value.

If we were to contribute $1,000 each month, our retirement freedom date is end of Sept this year. Cool!

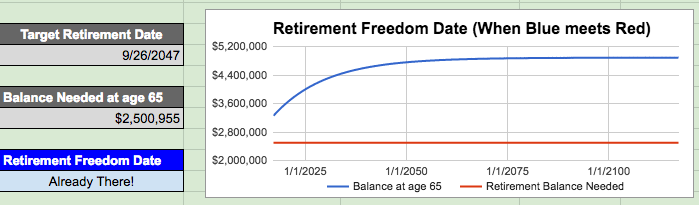

Scenario #2 – RRSP & TFSA

Scenario #1 is great and all. However, since I treat both RRSP and TFSA as retirement accounts, it makes more sense to do this calculation using the total portfolio value of our RRSP & TFSA. Again I used a monthly contribution of $1,000.

Booya! We are already retirement free!

Now… what if we don’t make any more contributions?

Wow that’s pretty cool and comforting to know that we have already hit Retirement Freedom with our RRSP & TFSA accounts. What’s even cooler is the fact we have about $750k of buffer, which is a lot if you ask me!

This means if we were to stop contributing to our RRSP and TFSA we would need to wait for about 31 years to retire. In my opinion, that’s way too long to wait. I want to travel and explore the world before I turn 65!

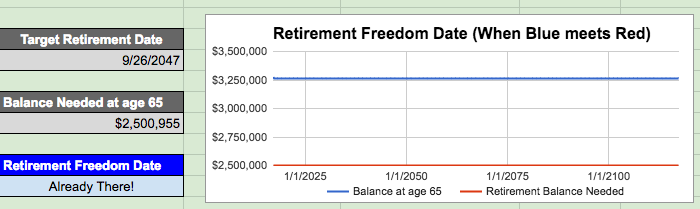

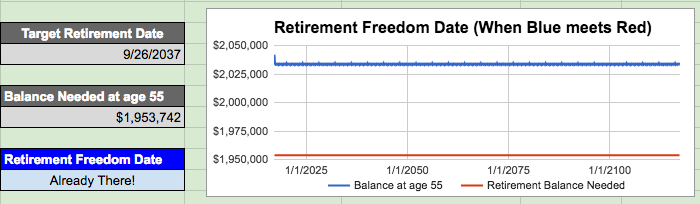

Scenario #3 – All Investment Accounts

I know Chris created the spreadsheet to calculate “retirement” accounts only. But what if we include all of our investment accounts and see what target retirement age we can hit if we don’t contribute any more money moving forward?

We end up with a retirement freedom age of 55! Wow that’s pretty damn amazing!

I showed this cool spreadsheet to Mrs. T and she was just as excited as I was. Call me lucky but I think it’s ultra cool to have a partner who is on the same wavelength as me when it comes to our goal of becoming financial independent.

So dear readers, please play around with the spreadsheet and see where you stand. Have you already hit Retirement Freedom? If not, when will you get there? I would love to hear your results.

Thanks for spreadsheet. Curious, what did you use for the expected tax rate? Should we use the marginal rate for our province of residence?

I used 15% I think. Use whatever lowest tax rate, assuming you are in that bracket in retirement.

Thanks for the spreadsheet. Fun to look at those numbers. Now, if only I could guarantee myself 8%…

Awesome spreadsheet! It tells me that I’ve got 11 more years to go (Nov 2028) before I’m there. Seems like a long ways ahead, but we are looking forward to it.

Thanks for sharing.

Thanks, 11 more years is pretty good. Good job!

Interesting spreadsheet Bob. I’m a little confused why anyone would want to stop contributing to retirement accounts while they’re still working to age 65 (or 55 for that matter). Why would you want to do that?

I guess you wouldn’t want to do that. The spreadsheet simply calculates whether you have sufficient money in your retirement accounts today if you were to retire at age 65.

One way you may not want to contribute more to retirement accounts is that you want to be tax efficient in retirement. For Canadians, you need to convert RRSP by 71 and if you convert it to RRIF there’s a mandatory withdrawal amount each year. You lose some flexibility that way.

Thanks for the shout out Bob. Awesome to see that you’re already there and that you’ve even got enough to be retired at 55 if you stopped today! Killing it!

Thanks for the awesome spreadsheet.

Cool spread sheet. What did you use as the expected annual investment return in your RRSP and TFSA? Retirement freedom is an interesting concept. I’ve technically hit retirement freedom as well, assuming I make on average 5% return above the inflation rate each year. 🙂

I just used the default parameters, I think 8% with 2.5% inflation rate.

Congrats on hitting retirement freedom!

I will have to look at this. From what you describe it seems to be a big nest egg retirement model rather than a cashflow model. We have a little more complicated solution with real estate and a looming government pension. However, we also have those retirement accounts. We might be up there with just those retirement accounts as we tend to have maxed them out for 15-ish years.

I wrote about an article about a similar concept to this that you might be interested in. The idea was creating a financially independent baby. Essentially how much money would you need to put aside to pay for the biggest life events of that baby.

http://www.lazymanandmoney.com/the-financially-independent-baby/

Yes it’s based on net egg retirement model but it’s a good thing to check. I guess it’s more complicated indeed if you’re using real estate as retirement fund too. This spreadsheet just uses retirement accounts.

Interesting article, that’s why we created a baby dividend portfolio a couple years ago.

https://tawcan.com/creating-legacy-dividend-portfolio-kids/

I got the chance to play with this. Even with only the retirement accounts we are in crazy good shape.

The defaults were pretty good, even the $29,000 expenses… especially with the mortgage paid off in ~10 years.

I had to keep on reducing things like contributing $0 and the age to retire to find a solution where we couldn’t retire. Looks like we’d have 7 years (age 48) if we did nothing on just the nest egg model.

I was surprised it was that early.

Looks like pretty good results for your guys. Good job!