We are hybrid investors. This means we invest in both individual dividend paying stocks and index ETFs. We are doing that because we want to construct our own ETF that can generate a steady dividend income; we utilize index ETFs to increase our overall asset and geographical diversification, since we can only hold a limited number of dividend paying stocks in our dividend portfolio.

With hybrid investing, we aim to capture the best of both investing strategies.

This is why I typically recommend new investors build up a sizable well-diversified portfolio by utilizing one of the all-in-one ETFs and then start buying dividend stocks if they want to.

Recently a reader reached out and asked the following question:

“You and your wife invest in index ETFs like XAW and QQQ. There are so many equity ETFs available in the market, are there any ETFs I should avoid? If so, why?”

When it comes to equity ETFs, there are many different types available – passive index ETFs, sector-specific ETFs, active ETFs, option ETFs, beta-specific ETFs, and the list goes on. It can be confusing and overwhelming to figure out which ETF to invest in, especially when you are a new investor.

Not all ETFs are created equal. Therefore, let’s examine which ETFs you should stay away from and not invest with your hard-earned cash.

ETFs I would recommend

Before answering the reader’s question, I would like to list ETFs that I recommend for any investors, newbie or reasoned.

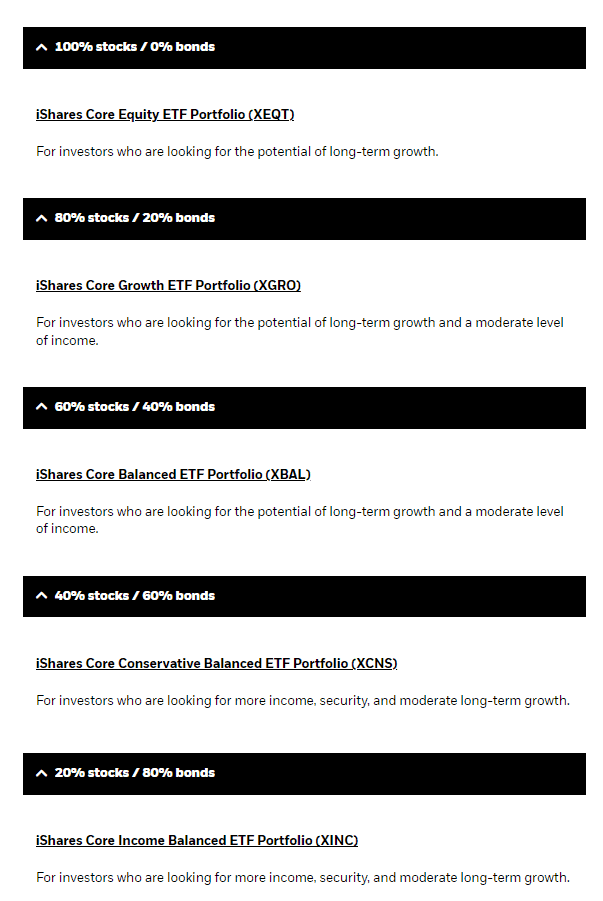

All-in-one ETFs

As mentioned in the introduction, I truly believe the all-in-one ETFs are great products. You can certainly build up an investment portfolio by buying only one of these ETFs. This is the case with Robb from Boomer and Echo.

I have so much conviction with these all-in-one ETFs that if we were new to investing and if we were to start over, I would 100% invest my money in one of the all-in-one ETFs.

Why do I like these all-in-one ETFs like VGRO, XGRO, VEQT, XEQT, and HEQT?

Simplicity.

Thanks to these all-in-one ETFs, you don’t have to rebalance, you don’t have to worry about diversification because they are asset and geographically diversified, and finally they are constructed per the already-determined asset & risk tolerance target.

Instead of worrying about all these investment details, you can focus on buying the ETF regularly and building up your investment portfolio.

Simplicity is one of the key reasons why we are utilizing XEQT for both kids’ RESP.

Dividend ETFs

Although we don’t currently invest in dividend ETFs, I have no issue with buying dividend ETFs to create a steady flow of dividend income.

However, do be mindful of how the different dividend ETFs are constructed. Some dividend ETFs are better than others. I have listed the top Canadian dividend ETFs and the top US dividend ETFs and provided my recommendations.

You want to invest in well diversified dividend ETFs with underlying holdings in different sectors. You also don’t want to have a dividend ETF that holds a lot of high yield high risk dividend paying stocks.

Best ETFs in Canada to invest in

All-in-one and dividend ETFs aren’t the only ETFs available on the market. There are a lot more different ETFs available. I would not hesitate to buy any of the best ETFs in Canada I have listed here.

Again, the beauty of these ETFs lies in their simplicity.

Which ETFs should I be avoiding?

To answer the reader’s question – are there ETFs I would not touch with a ten-foot pole?

Unfortunately, quite a few come to mind.

#1 Covered-call ETFs

I would not invest my hard-earned money in the high-yield covered call ETFs like ZWC, FLI, and TXF.

Why do I not like them? Because you cannot arbitrarily increase yields without taking on additional risks. Despite what these covered call ETFs say on their websites, utilizing covered calls to increase yield does introduce more risks. In general, you’re better off holding the underlying stocks. That way, you don’t miss out on the potential upside and also avoid the added option risks.

For me, I don’t think the additional risks are worth it. Furthermore, since total return is what matters, these covered-call ETFs have not performed well compared to the passive broad market index ETFs over the long term.

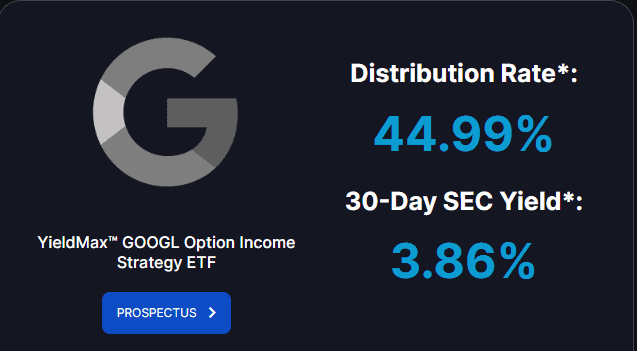

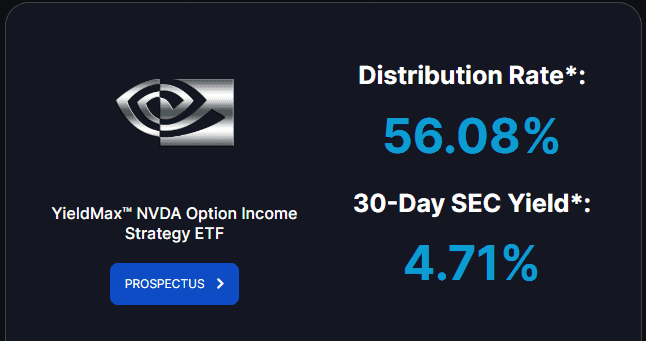

#2 YieldMax ETFs

Sigh…where do I start with these YieldMax ETFs?

Am I allowed to declare that these YieldMax ETFs are crap?

There, I said it!

It’s easy to get attached to these YieldMax ETFs because of the extremely high distribution rate.

YieldMax ETFs generate monthly income by utilizing options-based strategies on one or more underlying securities. Furthermore, the YieldMax ETFs do not invest directly in the underlying stock or ETF.

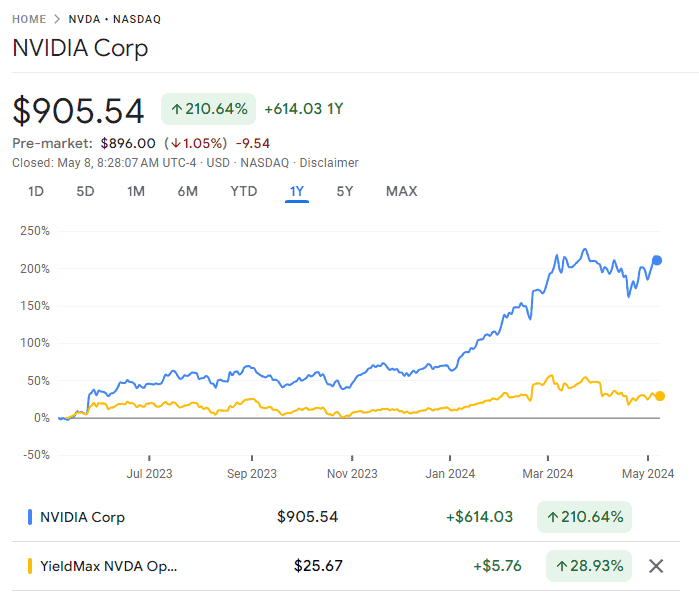

But if you compare the total return with the “parent” stocks, these YieldMax ETFs have performed extremely poorly.

Even with the extremely high yield, your overall return still lags behind the parent stocks. In addition, the yield for each YieldMax ETF varies month to month due to the underlying option strategies.

One way to look at it is that you’re essentially “investing” in these YieldMax ETFs and then get your money back in the form of distributions. You’re not really making any money!

To make matters worse, you are paying a high management fee to YieldMax.

No, thank you!

Note: While Hamilton Yield Max ETFs aren’t as extreme as YieldMax ETFs, they are similar in the sense both companies use option strategies to increase yield. Stay away from Hamilton Yield Max ETF too!

#3 BMO Equal Weight Banks Index ETF (ZEB) and CI Canadian Banks Covered Call Income Class ETF (CIC)

I don’t understand an equal-weight Canadian bank ETF like ZEB. Why pay an MER to these fund companies every year when you can simply construct your own by buying these banks yourself?

CIC is an equal-weight Canadian bank ETF like ZEB but then CIC goes one step further by using covered calls on these banks to create additional yield. Didn’t I just say that I don’t like these covered call ETFs?

No thanks.

Again, for cost and simplicity’s sake, you’re better off buying the Canadian bank stocks on your own.

#4 High MER sector-specific ETFs

There are many sector-specific ETFs available in the market. I have nothing against them especially if you want to utilize these ETFs to increase your portfolio exposure to a specific sector.

But watch out for the high MER! For example, comparing top Canadian REIT ETFs, PHR has a very high MER. You’re better off owning VRE and paying an MER that’s almost 50% less than PHR.

Similarly, if you would like to invest in a Canadian commodity ETF like the BetaPro Crude Oil ETF HOU, the BMO Equal Weight Oil & Gas index ETF ZEO, or the iShares TSX Capped Energy Index ETF XEQ, avoid the ETF with a high MER.

#5 Anything ETFs that says “leveraged”

As mentioned, not all ETFs are created equal. In the market, some ETFs use leverage to create more returns. For example, some ETFs are 2x or 3x leveraged bull or 2x or 3x leveraged bear.

When the market is going in the right direction as these leveraged ETFs, you can make a lot of money. But when the market is not, you can lose a lot of money. Leveraged ETFs aren’t for the faint of heart.

I don’t care how enticing these ETFs look, stay away from them!

Technically split-share corporates or split corp for short aren’t considered ETFs but since they trade on the stock market like any other stocks and ETFs, I decided to include them on this list.

Since these split-shares are highly leveraged and designed from the ground up to provide investors with income, they are typically very risky. If you look at the share price performance of these split-share corporations, you’ll notice that you end up losing your capital in the long run.

Just like the YieldMax ETFs, you’re essentially “investing” money to pay yourself with your own money (basically like an annuity but poorly constructed).

In other words, don’t get blind-sighted by the high yield these split-share corporations promise.

Summary – Are there ETFs you should be avoiding?

Are there ETFs you should be avoiding?

Absolutely! Not all ETFs are constructed equally so it’s important to examine how these ETFs are structured.

In summary, ETFs that use cover calls, leverage, and other methods to increase distribution yield and potential return are not worth investing in.

When it comes to ETFs, it is best to look for simplicity. If it takes more than a minute to understand the ETF strategy and the underlying holdings, you are better off staying away and investing your money elsewhere.

Hi Bob,

Thanks for the informative assessment, what do you think of the ETF XEG and XQQ? I got in while they were lower, but should I sell them to get the all in one ETFs instead?

Thank you.

Depends on how much you have for XEG and XQQ. You can always keep holding them and build up the portfolio by adding one of the all in one ETFs in combination.

It will be interesting and appreciated if one of you knowledgeable chaps could come up on this blog with a table of % performance & %MER for each of the financial-base ETFs mentioned in your replies: HCAL, CEW, ZEB… This could give us all a better appreciation of the real returns. For ex, I don’t mind paying a 2%MER on a financial ETF if it returns twice as much as the others…

I looked at CDN-banking ETFs that have been around since minimum of Jan 2021 (3 years performance) – there are newer ETFs available but for comparison sake, they were excluded because they don’t have a matching time record.

I also included VCN as a Canadian index for reference for the same period. Keep in mind 3 years is a very short time period but these are fairly new ETFs as a class in general.

Annual Return MER

VCN 11.95 0.05

ZWB 8.82 0.71

ZEB 12.63 0.28

HCAL 12.80 0.65

CIC 9.58 0.81

CEW 13.69 0.61

RBNK 11.24 0.32

Jan ’21 – Aug 24

*portfolio visualizer – includes dividends for returns.

Thanks for the info on Cdn Bank ETFs performance and MER. You mention HCAL has a MER of 0.65 while my fund facts doc shows 2.16%, a far cry from 0.61%.

Q. Which other Cdn Bank ETF would you be inclined to purchase based on the info you shown and the other info, quantitative and qualitative?

Thanks and cheers

Avoid Hamilton Cdn Bank ETF: Once you buy into it, you shockingly learn that its MER is 2.16% like a fully active mgt fund, but it’s only a risky managed ETF.

Pat of The Successful Investor Pat dislikes the firm’s use of leverage and its mean reversion strategy as he prefers to evaluate stocks based on their fundamentals. This means that even though he likes most Canadian bank stocks, this firm’s strategy isn’t a good fit for long-term gains. He suggests instead to invest in 2-3 of the Big-6 Banks.

Interesting point about the high MER, good to know. Thanks.

While I generally agree with your sentiment about avoiding high yield ETFs, there is a flaw with your presented data.

Google & Yahoo finance don’t include dividend distributions in their performance % (I mostly believe). Using another source, when I looked at Nvidia (Jun 23 – Jun 24 to match your screenshots), I get Nvidia at 198%, Yieldmax NVDA at 124%. Still backs what you’re saying, but the gap is smaller than presented.

Right, Google & Yahoo don’t include dividend distributions in the performance but you’re better off just holding the real stock rather than the Yieldmax ETFs.

I prefer bonds for the time being, when interest rates are expected to go down for the next 1 og 2 years at least.

Bonds vs. equities, that will depend on your age and your risk tolerance. 🙂

As a novice investor 3 y ago, ZEB had its appeal –

Cost per unit was low, attainable with limited funds;

Covered the major Cdn banks, an important component of the TSX;

Shares of individual banks were and still are costly, even more so currently;

There was/is a reasonable dividend of > 4%.

I have not sold the ZEB units since purchasing them, but have also added shares of 4 of the majors to my portfolio.

As a new investor with limited funds, ZEB made sense at the time as a means of acquiring a foothold in the Cdn banking sector. An index fund would have also held them but as a diluted component.

That’s a fair comment, thanks for the feedback.

Would you recommend CEW to get exposure to the major banks and insurers? Thanks!

Hi Charlie,

Given CEW only holds 10 stocks and use an equal weight approach, my view is you might as well hold these stocks on your own instead of paying the MER each year. You can only select which of the 10 to hold and which ones not to hold.

I agree the leveraged ETF has higher distribution and price drop. Will it be a benefit that we call claim for capital loss?

If you invest in non-registered account, yes you can claim for capital loss.

Writing covered calls actually reduces risk in a portfolio but also reduces returns compared to the same portfolio of just holding the same stocks. That’s the math of it.

If you already own the holding, yes it may reduce the risk. However, I’d argue investing in covered call ETFs and use them to build your entire portfolio is a risky business.

A very good comprehensive list for ETFs and tells you dos and dont’s but I am sure you will have some Passive investors coming after you about covered call ETFs 🙂

Haha, we’ll see what happens. 🙂

For the most part, I agree with the overall sentiment here. However, I do think there are one or two attractive ETFs out there that would hit your “naughty list” 😉

I also own a fair bit of ENS, which is a split share fund. It is only invested in Enbridge. On a five year basis it has out performed ENB, but in shorter time frames, it has not. The down side of ENS is it’s unlikely they’ll raise their distribution so once I retire and turn off the DRIP I will not see any growth in the income. (However, I expect to be in a position to be able to re-invest some of my distributions in retirement, so I could choose to do it here, if I like).

I have been eying HDIV – a CC / leveraged ETF. It’s a wrapper ETF that holds several other ETFs in proportions that amount to roughly 64% Canada and 36% US. Since 2021 it has out-performed compared to 64% XIC (or XIU) and 36% VFV. Yes, it’s high fee, but that’s exceptional performance. Unlike ENS, HDIV has a track record of raising the distribution, so I like that part of it as well.

I think in accumulation mode these investment vehicles should be used sparingly, if at all, but I think there can be a place for the better performing ones in a decumulation portfolio. Yes, there’s a chance one will under-perform, but for some investors, the ease of generating income from these holdings can be attractive.

I myself am considering HDIV, given it’s performance to date, but I want to see what happens over the next quarter or so.

Hi James,

Fair enough. I would never consider building a portfolio with the ETFs on the “naughty list.” Now, if you have a very diversified investing portfolio and you want to set aside say 5% of the money and invest in more risky stuff (we do that with ours) and invest the 5% with some of these higher risk ETFs, that’s fine. Because you’re limiting your potential loss. But if you have majority of your portfolio on say the Yieldmax I think that’s a very bad idea.

HDIV seems to be outperforming XEQT and other recommended ETFs on a total return basis.