I’m amazed that this blog has been around for more than ten years, especially knowing that many blogs either fade away or disappear completely after six months. For me, getting questions from readers and connecting with some of them in person has been a great attraction. Questions are always interesting to get as they reveal curiosity as well as often lead to many different kinds of important analysis.

Lately, I have been getting similar questions from different readers so I thought I’d write a post to cover three of the most common questions.

Common Question #1: Market all-time highs

Q: Are you worried about investing money into stocks & ETFs when the market is at all-time highs?

I understand why people are concerned with investing money into the equity market when the market is at all-time highs. It’s natural to think that if markets are at all-time highs, that there’s really only one way for them to go, and that’s the way investors don’t want. But let’s not forget the market has been hitting all-time highs multiple times.

I remember answering similar questions back in 2022, 2021, 2020, 2019, 2018…

Well, you get the picture. 🙂 It’s very much of a recurring pattern.

I get it. People get a bit squirmy when the market keeps going higher and higher. And we all realize there’s no guarantee that the market will keep climbing. The stock market is cyclical so even though we’re in a bull market, a bear market could be just around the corner. (The length of the average bear market is nine and a half months, while the length of the average bull market is two and a half years. That’s a fact worth remembering.)

Am I worried?

No.

Long time readers will remember I’m a huge advocate of time in the market and not timing the market.

So we will simply continue what we have been investing with our money:

Just. Keep. Investing.

Our investing strategy boils down to these four simple steps:

- Earn income

- Spend below our means

- Invest savings

- Increase our earning-saving gap

Rinse and repeat.

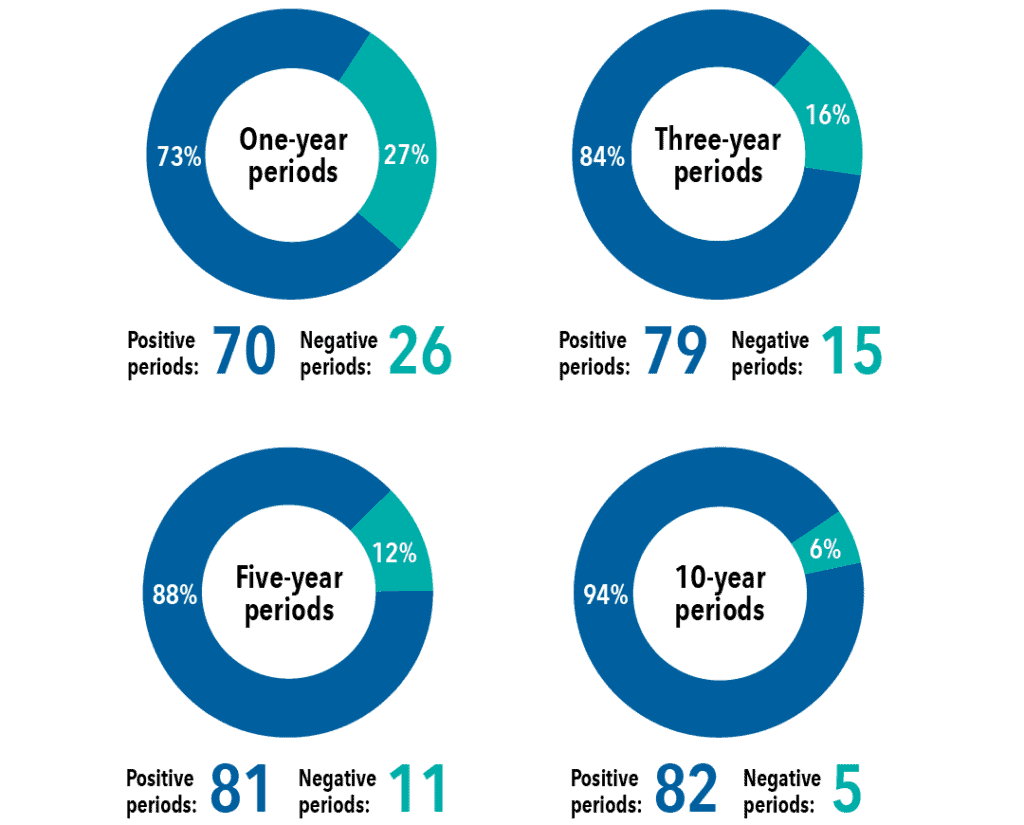

If you don’t believe me that time in the market is more important than timing the market, the smart folks at Capital Group also showed that time, not timing, is what matters.

The Capital Group pointed out that history has consistently shown that the longer the period, the greater the chance of a positive outcome.

Forget about option trading and speculating. For us, following the four simple steps and keeping it simple is the best strategy. This also allows us to remove our emotions from our investment strategy (at least as much as possible).

One important factor to remember about investing – investing and making profits is simple if you only look at things from the mathematical side. However, the difficulty of investing increases significantly when emotions are involved.

It’s easy to become a billionaire when you’re trading using paper money. When you are investing with your hard-earned money, emotions often take over and people make silly and highly questionable decisions.

It’s these stupid decisions that come back to haunt you!

Remember, we have no control over the equity market. There’s no way anyone can predict how long this bull market will last and there’s no way anyone can predict when the bear market will start and how long it will last.

I mean, did anyone predict the market drop back in 2020? And did anyone predict the quick recovery a few months later?

I don’t think so.

So rather than be scared about the market being at all-time highs and hiding your money under your mattress, allow me to repeat it again.

Just. Keep. Investing.

And keep it simple.

We have done so since our financial epiphany.

Do yourself a big favour and Ignore market performance and focus on your financial goals and milestones!

Common Question #2: Portfolio management

Q: I hold some of the same stocks in different accounts, should I treat and track the accounts individually?

Here in Canada, TFSA, RRSP, and non-registered are common accounts for individuals to have. Many readers hold the same stock in multiple accounts.

For example, one may have the following investment portfolio:

- TFSA: $70,000

- $10,000 worth of TD.TO

- $10,000 worth of CNR.TO

- $25,000 worth of TRP.TO

- RRSP: $75,000

- $10,000 worth FTS.TO

- $25,000 worth of TD.TO

- $25,000 worth of CNR.TO

- $15,000 worth of T.TO

- Non-registered: $50,000

- $20,000 worth of FTS.TO

- $15,000 worth of TD.TO

- $10,000 worth of T.TO

- $5,000 worth of TRP.TO

One then tracks these three different accounts individually via three separate spreadsheets. So in this example, the individual would tell me that they have 14.3% of TD in their TFSA and 30% of TD in their non-registered account.

But this becomes very confusing because it’s difficult to know the exact percentage of TD in your entire portfolio. It’s also very difficult to quickly figure out what’s the largest investment holding and its percentage.

Instead, I believe it’s much better – and more effective – to track all of your investment accounts in one master spreadsheet and track everything in one big portfolio.

Therefore, you are better off tracking all of your investment accounts. This is why I created the dividend portfolio spreadsheet template.

In the example above, I’d then track something like this.

| Accounts | Ticker | Total $ | Portfolio % |

| TFSA | CNR | $10,000 | 17.9% |

| RRSP | CNR | $25,000 | |

| RRSP | FTS | $10,000 | 15.4% |

| Non Reg | FTS | $20,000 | |

| RRSP | T | $15,000 | 12.8% |

| Non Reg | T | $10,000 | |

| TFSA | TD | $10,000 | 25.6% |

| RRSP | TD | $25,000 | |

| Non Reg | TD | $15,000 | |

| TFSA | TRP | $50,000 | 28.2% |

| Non Reg | TRP | $5,000 | |

| Total Portfolio Value | $195,000 |

Then it’s quite easy to see that TRP is the largest holding in this portfolio with TD being the second largest holding.

In the spreadsheet template, you’ll notice that I track the US stocks in USD. For the portfolio value, I then convert the US stocks into CAD equivalent using the daily exchange rate. I believe this is the easiest way to track US stocks but if you have other thoughts, I’d love to hear from you.

Common Question #3: Enroll in DRIP

Q: I have shares in TFSA and non-registered but not enough to enroll in DRIP. What options do I have?

I have mentioned a few times that DRIP is one of the three pillars to grow our dividend income (the other two pillars being new capital and organic dividend growth). Therefore, our investing strategy is to enroll in DRIP whenever we’re eligible.

There are two types of DRIP – synthetic DRIP and full DRIP.

Synthetic DRIP is typically offered by discount brokers where one or more (full) shares can be dripped at each dividend payout; you’d need to receive enough dividends to drip at least one share to enroll in synthetic DRIP. Some brokers, like TD Direct Investing, also honour the company DRIP discount so you could potentially save up to 5% on the DRIP price.

Historically, full DRIP is offered by company transfer agents like ComputerShare and Equiniti Trust Co. Once you set up an account with the transfer agent, you can drip fractional shares.

Years ago, the only discount broker that supported full DRIP was ShareOwner. In 2015 Wealthsimple acquired ShareOwner and wound down ShareOwner operation at the end of 2020.

Nowadays, Wealthsimple Trade is the only Canadian discount broker that offers fractional DRIP. Like full DRIP, fractional DRIP allows you to automatically add fractional shares regardless of how much dividends you receive at each payout. No other Canadian discount brokers support fractional DRIP.

- Sign up for Wealthsimple with my referral code or type in YDC3NA when you sign up. You’ll get a $25 reward for simply signing up.

To answer the reader’s question about options to enroll in DRIP…

Option 1: You can transfer your stock in-kind out of TFSA and into your non-registered to have enough shares to enroll in synthetic DRIP. If you withdraw money from TFSA, you gain that amount of contribution room the year after your withdrawal.

Although I have not made any in-kind transfers out of TFSA before, I think this option is quite beneficial, because you increase contribution room the following year. So this could be a very effective strategy every November and December.

This option caused tax implications because you will receive more dividends in your non-registered account. You would also need to track the adjusted cost basis (ACB) for tax purposes.

Option 2: If you have enough TFSA contribution room, you can transfer your stock in-kind from non-registered to your TFSA. When you do that, you essentially “sold” your stock in non-registered and you’d need to declare either a capital gain or a capital loss. Once you have enough shares in your TFSA account, you can enroll in synthetic DRIP.

Option 3: transfer both your TFSA and non-registered accounts in-kind from your discount broker to Wealthsimple Trade and then enable fractional DRIP.

The same can be said for RRSP/RRIF too but there are a bit more tax implications if you withdraw from RRSP into either a TFSA or a non-registered account (it’d be considered as an RRSP withdrawal and you need to declare the withdrawal as income).

In this example, the easiest way to enroll in DRIP, I believe, is option 3. The next best method is option 1 (because you create additional TFSA contribution room for next year, a good financial strategy to use at the end of the year). Option 2 is the least preferred option because you would trigger either a capital gain or a capital loss. Having said that, if you have any TFSA contribution rooms left, option 2 may be an excellent way to max out your TFSA.

This is why personal finance is so interesting, there’s no right or wrong answer. The decisions one makes are very personal!

Summary – Answering 3 Common Investment Related Questions from Readers

I hope this post has been useful for readers. If you have any questions, feel free to comment below or send me an email. I’m always happy to answer questions and connect with readers. Who knows, maybe I’ll create more of these common question posts in the future.

One note: you should not transfer in-kind from a non-registered account to a TFSA if you have capital losses as they will not count due to the superficial loss rules. Just something ti keep in mind!

Good point, thanks for pointing that out.

I love your blog and have been reading for many years, but have never commented until today! I use Questrade for my trading and last time I logged in they had a new popup – Fractional shares are here! I was so excited thinking it was a fractional DRIP, but after chatting with them they said they are working on rolling it out to DRIPs as quickly as possible (no ETA) – but it is coming. At the beginning of the year I had been seriously looking at moving my accounts to Wealthsimple due to the 0$ trades and the fractional DRIP (and the tempting promotion). I guess a lot of people were moving their money for them to introduce both these items. 🙂

Thank you St8cey for following and reading the blog for so long. Yes, very excited that Questrade is finally catching up to Wealthsimple in terms of these key features. I think fractional shares are only for US stocks & ETFs for now but the feature will be available to Canadian stocks & ETFS soon.

It’s good to have competition and we the consumers are benefiting. 🙂

One correction regarding option 2. One cannot transfer in-kind shares that have a capital loss from a non-registered account into a TFSA or other registered account and claim a capital loss in the non-registered account. To claim the loss, one must sell the shares in the non-registered account, transfer the proceeds to the registered account and if desired, then repurchase the same shares.

On the other hand one is required by CRA to claim a capital gain when transferring in-kind shares that have gained in value from a non-registered account to a registered account.

CRA rules sometimes seem not to make sense.

Thanks for pointing this out.

Well, the rule that you have to claim the capital gain before transferring in-kind shares that have gained value to a registered account does make sense because then you could transfer ‘all’ the winners from Non registered to registered and avoid paying capital gains on it. ‘Death and Taxes’

One thing I would suggest is not to use WealthSimple for Spousal RRSP accounts or any other accounts where you cant hold USD. Their FX fees and the rates are very steep. Morever, you cant hold USD in Spousal RRSP accounts so you have to pay FX fees and currency exchange fees each time you buy/sell any stock. Other than that, WS is very good for holding Canadian stocks.

When we moved from Questrade to Wealthsimple, we moved USD as well and with the free US account, we haven’t paid anything to Wealthsimple in terms of FX fees. It’s really not as a big deal out people make it out to be IMO.

You cant have a USD account for Self Directed RRSP accounts. So you cant hold USD in your account for Self Directed RRSP accounts. So each time you purchase/sell a USD stock, you have to pay the 1.5% fee plus FX Conversion fees (which I have compared with IB is higher). This adds up to a lot of fees.

I have a LIRA account with WS. This account lets me hold USD. Plus having a certain account value you get to have a USD account for free. Otherwise its like $10 per month.

So in general WS is perfect for dealing with Canadian stocks, but for other types, please read the fine print and be fully aware of the FX conversion fees and Currency exchange rates etc.,

I have a self directed RRSP with Wealthsimple and have been able to buy/sell USD stocks and leave the money in USD. This is because I have the USD accounts option enabled (once that’s enabled you . And because I’m a Generation client, the USD account is available for free rather than $10/month.

More info here – https://help.wealthsimple.com/hc/en-ca/articles/4414660979355-Upgrade-to-USD-accounts

The 1.5% currency conversion fee is not different than how much Questrade charges. Yes with Questrade you can save the conversion fee by using Norbert’s Gambit but now Questrade charges $10 per Norbert’s Gambit.

Yes, there are limitations to WS, but there are also limitations to Questrade and other online brokers too. What I was trying to get to is that too many people get fixated on WS’ “currency conversion fee.”

Self Directed SPOUSAL RRSP cant have a USD account. A regular RRSP account can have USD account.

Not having a USD account for a Self directed Spousal RRSP would be a huge deal because you pay FX fees each time you buy and sell a US stock.

Just want everyone to be aware of this as it adds up significant costs if you plan to deal with US stocks in a SELF Directed SPOUSAL RRSP.

Ahh, I wasn’t aware of that for self directed spousal RRSP. Definitely a limitation.

Awesome. Nice one!

Thank you.