As an engineer by education & training and an analytical person, it shouldn’t come as a surprise to readers that I ponder a lot. I like to think about something carefully before deciding or reaching a conclusion. Although this approach may not work in all situations, I enjoy being analytical on major life decisions.

The other day I woke up with this interesting idea in my head. The idea simply wouldn’t escape from my head and I ended up thinking about it for the entire day.

The interesting idea is simple: Should we go all in on QQQ with our RRSPs?

Since this is an interesting idea, I thought I’d turn it into a blog post, analyze the idea thoroughly, and hopefully come to a conclusion.

Things to consider

A few things before we dive into the analysis.

RRSP is a tax-deferred account. When you contribute to RRSP, you get a tax deduction for 100% of your contributions. If you contribute $10,000 to your RRSP, it will reduce your net income by $10,000, and potentially bring you down to the lower tax bracket.

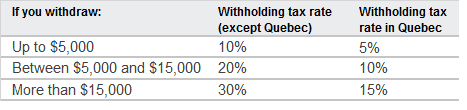

When you withdraw money from your RRSP, you will be subject to withholding tax. The amount of withholding tax is based on how much you take out.

The net amount after the RRSP withholding tax is then taxed at your marginal tax rate.

You also must convert an RRSP to a retirement income option such as an RRIF by the end of the year that you turn 71. Although there are no mandatory withdrawal requirements in the year you set up your RRIF, you must start withdrawing money the year after setting up your RRIF (effectively at age 72). Furthermore, there’s a minimum withdrawal rate for RRIF. The withdrawal rate increases as you age.

Note: You can convert your RRSP before age 71. If you do, there’s a minimum withdrawal rate starting at age 55.

Just like the RRSP, money withdrawn from an RRIF is taxed like working income, or at 100% of your marginal tax rate.

In other words, it doesn’t matter whether the money is from capital gains or dividend income, money withdrawn from an RRSP and an RRIF is taxed at 100% of your marginal tax rate. You don’t get any preferential dividend tax treatment like in non-registered accounts.

When we do start living off our investments (aka live off dividends), our withdrawal strategy is very similar to Mark from My Own Advisor – NRT. This means drawing down some non-registered (N) assets along with registered assets (R), leaving TFSAs (T) for as long as possible.

More details:

- N – Non-registered accounts – we most likely will work part-time to keep ourselves engaged and live off dividends to some degree from our non-registered accounts. The preferential dividend tax credits will come in handy.

- R – Registered accounts (RRSPs) – we plan to make some early withdrawals from our RRSPs slowly. We may collapse our RRSPs entirely before age 71. We may also convert our RRSPs to RRIFs. This is not entirely decided (if we do convert to RRIF’s, we want to make sure the dollar amount is relatively small). Early withdrawals will help us from having a large amount of money in our RRSPs and having a big tax hit when we start withdrawing. In other words, this will help smooth out our taxes.

- T – TFSAs – since any withdrawals from TFSAs are tax-free, we intend not to touch our TFSAs for as long as possible so they can compound over time.

Mark, along with Joe (former owner of Million Dollar Journey), ran an analysis for us many years ago via their Cashflows and Portfolios Retirement Projections to reinforce this withdrawal plan.

Note: if you’re interested in this retirement projections service, mention TAWCAN10 to Mark and Joe to get a 10% discount.

We may also do an RNT (Registered, Non-Registered, then TFSA) withdrawal strategy but will need to crunch some numbers. Whether it’s NRT or RNT, the important part is that we plan to slowly withdraw money from our RRSPs.

Current RRSP Holdings

Although RRSPs are best for holding US dividend stocks to avoid the 15% withholding tax, we hold US and Canadian dividend stocks and ETFs inside our RRSPs.

At the time of writing, we hold the following stocks and ETFs inside our RRSPs:

- Apple (AAPL)

- AbbVie (ABBV)

- Amazon (AMZN)

- Brookfield Renewable Corp (BEPC.TO)

- BlackRock (BLK)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Costco (COST)

- Emera (EMA.TO)

- Enbridge (ENB.TO)

- Alphabet Inc. (GOOGL)

- Hydro One (H.TO)

- Johnson & Johnson (JNJ)

- Coca-Cola (KO)

- McDonald’s (MCD)

- Pepsi Co (PEP)

- Procter & Gamble (PG)

- Qualcomm (QCOM)

- Invesco QQQ (QQQ)

- Royal Bank (RY.TO)

- Starbucks (SBUX)

- Telus (T.TO)

- Tesla (TSLA)

- TD (TD.TO)

- Target (TGT)

- TC Energy Corp (TRP.TO)

- Visa (V)

- Waste Management (WM)

- Walmart (WMT)

- iShares ex-Canada international ETF (XAW.TO)

Our RRSPs consist of 18 US dividend stocks, 10 Canadian dividend stocks, and 2 index ETFs.

In terms of dollar value, my RRSP makes up about 70% while Mrs. T’s RRSP (spousal RRSP) makes up about 30%. Ideally, it would be great if our RRSP breakdown were 50-50 (I’m ignoring my work’s RRSP so in reality the composition is more like a 25-75 split).

Because we started Mrs. T’s RRSP a few years later than mine it hasn’t had as much time to compound. Furthermore, I converted over $120,000 worth of CAD to USD in my RRSP when CAD was above parity. Over time, this gave my self-directed RRSP an automatic 30% performance boost.

In addition, because the exchange rate hasn’t been as attractive, the only US holdings Mrs. T has are Apple and QQQ. The rest of her RRSPs are all in Canadian dividend stocks.

We purchased QQQ earlier this year inside Mrs. T’s RRSP. Dollar-wise, it makes up a very small percentage of our combined RRSPs.

Some info on QQQ

For those readers who aren’t familiar with QQQ, it’s an ETF from Invesco. Since launching in 1999, the ETF has demonstrated a history of outperformance compared to the S&P 500.

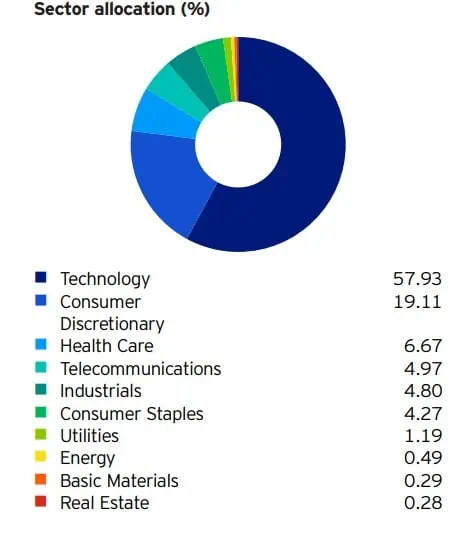

QQQ tracks the Nasdaq 100 Index. The fund is rebalanced quarterly and reconstituted annually. At the time of writing, QQQ holds 101 stocks with the top 10 holdings being Microsoft, Apple, Nvidia, Amazon, Meta, Broadcom, Alphabet Class A & C, Tesla, and Costco. The top 10 holdings make up 47.01% of the fund.

The top 11 – 20 holdings for QQQ are AMD, Netflix, PepsiCo, Adobe, Linde, Cisco, Qualcomm, T-Mobile US, Intuit, and Applied Materials. These holdings make up 15.71% of QQQ.

Due to the nature of the Nasdaq 100 Index, QQQ is heavily exposed to technology and consumer discretionary sectors.

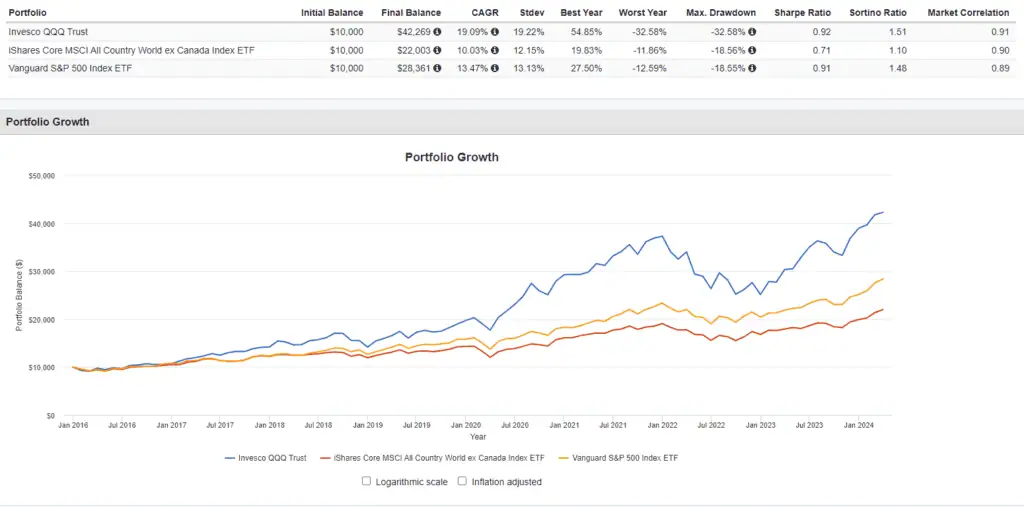

As you can see from below, it also outperformed XAW and VFV significantly. This is the key attraction of QQQ, as the fund has historically outperformed many major indices.

As you can see from above, $10,000 invested in QQQ in 2016 would result in over $42,000 in 2024 whereas the same amount invested in XAW and VFV would result in less than $30,000.

Cases for going all in on QQQ

Why would we consider going all in on QQQ?

Because QQQ has done very well historically compared to the major US and Canadian indices.

Per the chart above, QQQ had an annualized return of 19.09% since 2016. In the last 20 years, QQQ has had an annualized return of 14.03% and an annualized return of 18.12% in the last 10 years.

Assuming we invest $150,000 in QQQ and enjoy an annualized return of 15% for the next 10 years, we’d end up with $606,833.66, assuming no additional contributions. On the flip side, if we have the same money and have an annualized return of 10% (long term stock return), we’d end up with $389,061.37. This means investing in QQQ would result in more than $217.7k of difference in return on capital or 56%. This is a pretty significant difference.

Yes, historical returns don’t guarantee future returns. However, the high exposure to technology stocks should allow QQQ to continue the superior return for years to come.

Due to the fact that RRSP and RRIF withdrawals are taxed 100% at our marginal tax rate, it makes sense to attempt to maximize the total return inside of RRSPs/RRIFs instead of a mix of dividend income and capital return.

Cases against going all in on QQQ

The biggest case against going all in on QQQ? Our dividend income would take a big hit.

Our RRSPs contribute about 30% of our annual dividend income. With our 2024 target of $55,000, selling everything in our RRSPs and holding QQQ only would reduce our total dividend income to about $38,500 (ignoring QQQ distributions completely).

But focusing on dividend income alone is a bit silly when we should be considering total return and the total portfolio value.

Out of the 18 US stocks that we hold in our RRPS, QQQ holds 9 of them already. The stocks that QQQ doesn’t hold are:

- AbbVie

- Johnson & Johnson

- Coca-Cola

- McDonald’s

- Procter & Gamble

- Target

- Visa

- Waste Management

- Walmart

These 9 stocks make up about 25% of our RRSP in terms of dollar value. Since we purchased these stocks many years ago, they have all done very well, with a few of them being multi-baggers. I would hate to sell the likes of Visa and Waste Management.

Investing in QQQ does mean that when we start to live off our investment portfolio, rather than withdrawing mostly from dividends inside our RRSPs in the first few years (to increase our margin of safety), we’d need to sell QQQ shares and touch our principal.

If there are a few years of poor returns at the beginning of our retirement, this could cause a significant reduction in our portfolio value. Essentially, selling shares may not have as much margin of safety compared to relying on withdrawing dividends only.

Another case against going all in on QQQ is that QQQ is currently highly concentrated in technology stocks so it’s not all that diversified compared to other index ETFs like XAW. The latest AI hype has significantly bumped up the share price of many technology stocks. Would we see a Dot Com type of bubble in the future and hamper the return of QQQ? That’s certainly possible.

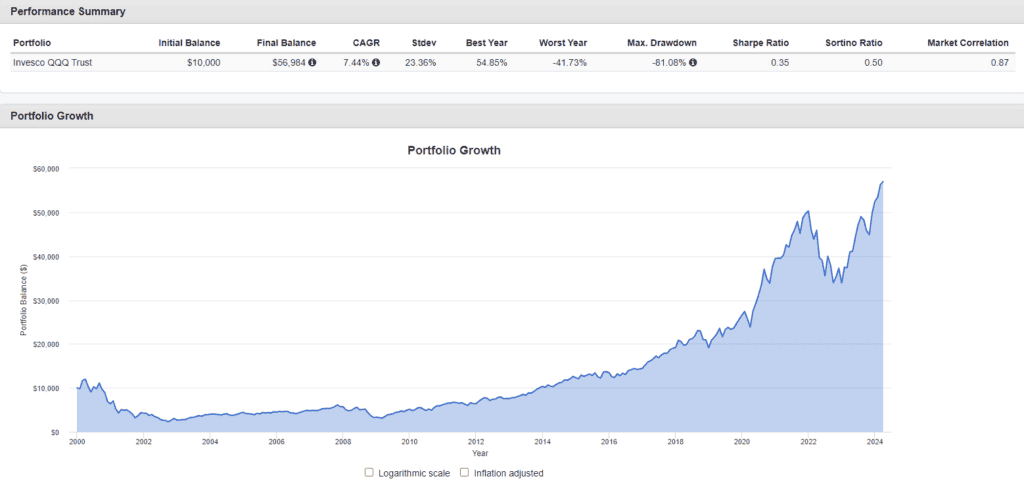

s you can see from the chart above, QQQ didn’t recover from the Dot Com bubble for about 14 years. This is a risk we would take on if we were to go all in on QQQ.

Potential Alternatives than going all in on QQQ

Instead of going all in on QQQ, there are some potential alternatives.

First, we can simply add more QQQ shares in the next few years to have QQQ make up a larger percentage of our dividend portfolio. This is already our plan of record but we stay focused on this goal instead of purchasing more dividend paying stocks in our RRSPs.

Second, since we hold QQQ inside of Mrs. T’s RRSP and she holds mostly Canadian dividend stocks in her RRSP, we can consider closing out these positions and using the money to buy QQQ shares.

If we were to do that, we’d only lose about 12% of our forward annual dividend income, going from $55,000 to $48,400. Assuming QQQ continues the superior performance over other indices, holding only QQQ and Apple in Mrs. T’s RRSP and continuing to contribute to her RRSP only may mean that we have a higher chance of ending up with a 50-50 RRSP split down the road.

Some additional logistics to consider

The second option mentioned above is quite intriguing. But there are some logistics to consider if we were to forward with this option.

The first thing to consider is that we’d need to sell all 9 stock holdings in Mrs. T’s RRSP. At $4.95 per trade at Questrade, this would cost us $44.55. Not a significant amount of money but it would be cheaper if we were to transfer her RRSP to Wealthsimple.

Second, we’d need to convert CAD to USD and take a hit on the exchange rate. Utilizing Norbert’s Gambit would allow us to save on the additional current exchange fees. The alternative solution would be to journal as many of the holdings to the US exchange, close the positions, and end up with USD.

Another option is to consider the Canadian equivalents, like XQQ, ZQQ, HXQ, or ZNQ to avoid currency conversion. As many of you know, I’m all for simplicity and straightforwardness, so it makes sense to hold the original ETF QQQ instead of other alternatives.

Conclusion – Should we go all in on QQQ?

So, have I reached a decision after all the considerations?

I’ll admit, the second option mentioned (holding only QQQ in Mrs. T’s RRSP) is very intriguing to me. But I am going to sleep on it for a bit and discuss the idea with Mrs. T before making any major decisions. In the meantime, we will continue to add more QQQ shares in Mrs. T’s RRSP so QQQ makes up a bigger percentage of our dividend portfolio.

Readers, what would you do? Would you go all in on QQQ?

Hi Bob,

I’m just transferring an old work RRSP that was in mutual funds with RBC to self directed with Wealthsimple (on pension at current job). It’s only about $6000 and I was thinking about just buying an ETF like ZGRO. I won’t contribute to it until I max my TFSA which is a long way off. Good idea?

QQQ finally correcting , looks like will be a time to buy soon!

Looks like it.

Better to buy QQQM instead of QQQ because it’s the same fund company and it’s a lower MER. The volumes on QQQM are plenty too so no worries about spreads. Canadian version QQC is a CAD option that just holds the US version.

Thanks for the tips, will take a look.

For US dollars, buy QQQ. For canadian dollars, buy QQC (unhedged Nasdaq-100) from invesco. Half the MER of XQQ, it literaly holds QQQM (Invesco’s version of QQQ). No need to bother with the currency conversion, with Wealthsimple you have access to fractionnal shares and with Questrade since it’s an ETF buying is free. Voilà!

Thanks for these tips.

This whole article is talking about chasing past returns while mentioning it’s historically possible to underperform for 14 years if the timing is off. I agree with the first comment if you’re in retirement or lose to it I’d be more focused on diversification even if you’ll always be unhappy something is underperforming.

The other thing to mention your comment about your stocks doing so well that you’d hate to sell it- the correct mentality would be ignoring their past performance and looking into if they are the best choice for your returns in the future. For Visa for example, seeing if that was successful in the past is still true today- that requires looking at proposed regulation now and non the future, looking at start up contenders etc. I’m not saying Visa is bad to hold just don’t get blind sided by past performance and focus on the next 20 years will it continue to outperform.

Hi Doug,

Yes, all valid points. Like I said, it was simply an interesting question that I was wondering and thought I’d turn it into a blog post and see what readers think. As you can see from all the comments, lots of good discussions. Agree with you that you should focus more on future outlook rather than looking at the past performance.

I have a large percentage of US equity exposure with a hefty amount of home bias. I have some QQC that I started buying early this year. I bought quite a bit of TXF near the bottom in 2022. I believe as some posters are saying that it is not the best time to buy QQQ, but I will continue to buy QQC in small amounts over a long period of time so I don’t care about the timing so much. My biggest fear about all US stocks and stocks in general is the potential downfall of US democracy. How would Amazon stock fare if it was a Chinese company? Probably about as well as Alibaba.

This woudn’t be the time that I’d go all in on QQQ. I like to buy things that are typically out of favor. Today, I think that might be small cap stocks (at least in the US – I don’t know about Canada) and energy stocks. I think energy is an underrated AI play anyway.

I did buy some QQQ a couple of years ago when tech was out of favor using the same logic as above.

Long-term I’m a fan of QQQ and in retirement accounts, it certainly makes sense as it is a long-term thing. I’m just concerned that it’s similar to the dot-com bubble. Even if it doesn’t drop a lot like in 2001, maybe most of the gains are baked for the next few years and it doesn’t do anything.

I’d be curious what the 10-year and 20-year returns were in 2022 before the latest run. I wonder if QQQ beat other indexes by that much back then.

Agree, probably not the best time to go in on QQQ when it’s at all time high. But it does make a good discussion. 🙂

I’m nearing retirement and decided to buy some JEPQ which is based on the Nasdaq-100 as well but uses options to generate a high-yield. This way, I can still get some of the upside of the index without having to sell the capital. It is likely that QQQ would outperform it, especially in the good years (recent history, for example), but having a nearly 9% yield is great for a cashflow portfolio.

Please be very careful. The underperformance in utilizing options is significant. For example, QQQ for 2023 return was 54.73% and JEPQ is 36.28%. The inefficiency in selling options leads to significant underperformance all for the convenience of yield. Remember, performance factors the yield reinvested (which isn’t what you want to do here), so the return is even worse. The more volatile the ups or downs, the less efficient these options become. I would recommend just selling as needed or placing a portion of the cash you need in the short term (1-3 years) in cash equivalent while investing the rest in pure index.

I’d be very careful with any of these high yield ETFs/stocks. Make sure you limit your exposure.

Hi Bob:

QQQ does indeed look like a very interesting ETF investment – albeit primarily for future potential capital gains. Thanks for making your readers aware of QQQ.

But I really can’t see any advantage to holding QQQ in a registered account versus a non-registered account … it’s all capital gain no matter where you hold it and it’s all non-taxable until you “realize” (sell) it. It doesn’t matter what type of account QQQ is held in – the end result is the same. The difference comes when you eventually sell (and at some point you must) – then you’ll be much better off tax-wise holding QQQ in a non-registered account. I’ll use max Ontario tax rates for my following numbers example. Assuming you can keep under the new $250K capital gains threshold, you would pay 26.5% tax on capital gains derived from a non-registered account – 35% on amounts over $250K. For RRSP/RRIF accounts you would be taxed to the max – as you stated, there are no tax advantages for withdrawals which are all treated as pension income and fully taxable. Take your capital gains out of a registered account (excluding TFSA) and you will pay 53% tax. This makes the RRSP/RRIF approach sound like an overall long-term losing proposition to me.

That’s why I stressed in the interview we did several years back that one is actually better off tax-wise seeking capital gains in a non-registered account. Yes – you do get the immediate tax refund for RRSP contributions … but it’s usually given at a much lower tax rate than the tax rate will be 25-30 years down the road when you try to take your money out of a RRIF – and believe me … it’s not pretty. And over the years, governments always seem to raise tax rates (e.g. we’ve just seen that with the new capital gains revisions) – so who knows what the tax rates will be 30 plus years from now? – but we all know for certain, they won’t be lower!!

Also, I know it’s something we don’t like to think about when we’re young, but remember the saying about the “certainty of death and taxes”. The newly introduced capital gains tax expansion is in effect a disguised (hidden) death/wealth/estate tax increase on capital gains inherent in one’s estate that exceed $250K. The Feds know this and see it as a long-term source of additional tax revenue … a sly tax increase on their part that is designed to catch people unawares. And the tax increase also applies to RRSP/RRIF holdings which become fully taxable upon death (or death of the surviving spouse). Again, the estate tax rates would be lower on capital gains held outside of a registered account (26% under $250K rising to 35% on amounts over $250K versus 53% for RRSP/RRIf pension income).

So the question … what to do?? Thanks for the tip about QQQ – I’m not a big ETF investor and so wasn’t aware of this one … but it does look interesting and I’m going to look into picking up a few shares myself. But I don’t think one should go “all-in” with QQQ as suggested in your article. Remember that one of the keys to successful investing is diversification – don’t lose sight of that key aspect – and the “all-in” approach is gambling – going for the “big win” – it’s not diversification. As I said, QQQ does indeed look like a high-performance worthwhile investment – but I would still treat it like any other dividend stock holding – one must be mindful not to drift away from one’s established sound investing approach. I think one could definitely buy some QQQ shares and possibly build up a balanced position(s) in all of your accounts where it would be tax-efficient – but possibly excluding RRSPs.

I classify investing in RRSPs at a young age and continuing to do so over the years as being the single biggest investment mistake I’ve ever made. RRSPs are great for the financial institution that accepts your annual contributions and holds your $$$ for the next 50 years plus – but for the tax-aware investor … an RRSP is not such a great deal at all. This fact may not be evident in one’s younger years while one enjoys the annual tax deductions, but the tax drawbacks will become very apparent when one starts to withdraw funds from an RRSP/RRIF.

Kindest regards,

Reader B (aka Blucat)

July 15, 2024

Hi Reader B,

Thank you for chiming in on this interesting idea. You raised a very good point on the $250k capital gain. Yes, RRSP withdrawals are taxed at your marginal tax rate so there’s some benefit to invest QQQ in a non-registered account. Even if you invest in the TFSA, you’re paying taxes with the initial money already. Regardless, the CRA will get their money one way or another.

I definitely agree with you that we shouldn’t go all in with QQQ and look for diversification. It was an interesting idea that I was pondering about and wanted to turn it into a blog post. I thought it’d create some interesting discussions with readers too. 🙂

Why not go all QQQ in TFSA instead?

QQQ pays little dividends, so you will not lose much in terms of the foreign tax credit

That’s definitely a valid point, just have to convert CAD to USD. Already have some USD in RRSP so it’s easier. 🙂

How about XQQ in CAD?

That’s certainly an option as well.

I have QQQ in Corporate brokerage account.

Going into QQQ at all time highs?? It’s like any other stock at ATH.

I wish I had gone 100% in with Nividia, BRK, SPY!!

Diversify, diversify, diversify.

Who knows what QQQ will do in future.

I’d rather have a steady 3-5% a year growth in a diversified portfolio than all assets in one.

Who knows, interest rates could remain high or the current high tax and spenders with increasing tax plans on stocks could remain in government in Canada/US next year and tank the stock market

Yea we have some QQQ now. Definitely hard to buy more when it’s at all time high. 🙂

I would say that it would make sense to go all QQQ if you have a long time before needing the funds. If I am not mistaken, let’s say you happen to have bought the QQQ in 2000, it would’ve taken more than a decade to go back in the green. With no DCA, it would’ve taken exactly 16 years before going back into the green…that’s if your timing was poor.

Naturally over the long run, I do believe the QQQ’s will out perform the SP500, but I would only say yes to you if you have more than 20 years before touching that money if I were in your shoes(Not financial advise 😛 ). Less than that, naturally there will be risks associated with it and it will all depends if both of you can sleep well at night. With your nest egg in the TFSA, I suspect you can delay more than 20 years before your RRSP withdrawal if the worst scenario like the lost decade does happen starting tomorrow.

It’s definitely not an easy thing to answer as it all depends on your risk tolerance.

Yup, you’d need a long time line to take advantage of the overall higher growth from QQQ. But short term wise QQQ can be quite volatile as you pointed out.

It’s not an easy thing to answer for sure, hence for me saying this is an interesting idea. 🙂

Interesting post and notion Bob. Given that you’re already in the retirement risk zone, I’d suggest you should be going the other way – protecting your assets for spending – and that includes share harvesting.

Perhaps the TFSA would be an area to go for growth on a steroids bet, given that the account might not be touched for a decade or two, or three?

Hi Dale,

Like I said, it was an interesting idea to ponder about. Good point about using TFSA instead.