Another year almost in the books means that a new year is almost around the corner and the new TFSA contribution room will be available for all eligible Canadians. In 2025, the contribution limit will stay at $7,000. In other words, between Mrs. T and I, we can contribute up to $14,000.

TFSA started in 2009 and it is arguably the best “retirement” – or investment – account that the Canadian government has ever created. The yearly contribution room is small compared to the RRSP but things do add up over the years. In addition, the TFSA is totally “tax free” whereas the RRSP is only tax deferred.

If you’ve been eligible to contribute to a TFSA since 2009, it means that you have an accumulative TFSA total of $102,000 available. At a 4% dividend yield, you can generate $4,080 in tax free dividend income each year.

More importantly, that $102,000 can grow inside of your TFSA tax free! If you allow your money to compound inside of your TFSA over the years, you should see a sizable number. And the beauty is that when you withdraw money from your TFSA, you don’t have to worry about income tax (unlile a RRSP/RRIF). Let’s not forget that dividends inside of the TFSA are tax free too.

That’s why I said TFSA is the best retirement account for Canadians.

If you’re not familiar with the TFSA, you may want to take a look at the millennial’s ultimate TFSA guide.

Currently, we only hold Canadian dividend stocks inside our TFSA. Yes, the math showed that it made more sense to invest in US dividend stocks and ETFs in TFSA, but we want to keep things as simple as possible and avoid any currency conversions and 15% dividend withholding tax on US dividend stocks and ETFs.

Typically we’d transfer money for the new TFSA contributions on January 1st and then buy stocks the first day that the market opens in the new year.

Which Canadian dividend stocks are we considering for our TFSAs in 2025?

Consideration #1: Waste Connections

We currently hold Waste Connections in our taxable accounts. Since Waste Connections’ share price has appreciated over the years, it may make sense to hold new shares inside a TFSA to avoid capital gains when we do sell these new shares.

Why purchase more Waste Connections

Per Benjamin Franklin, nothing is certain except death and taxes. I’d argue there’s one more certainty in life – garbage. No matter how hard we try to reduce and eliminate garbage, we will produce some level – arguably, an ever-increasing one – of garbage regardless.

This is where Waste Connections come in.

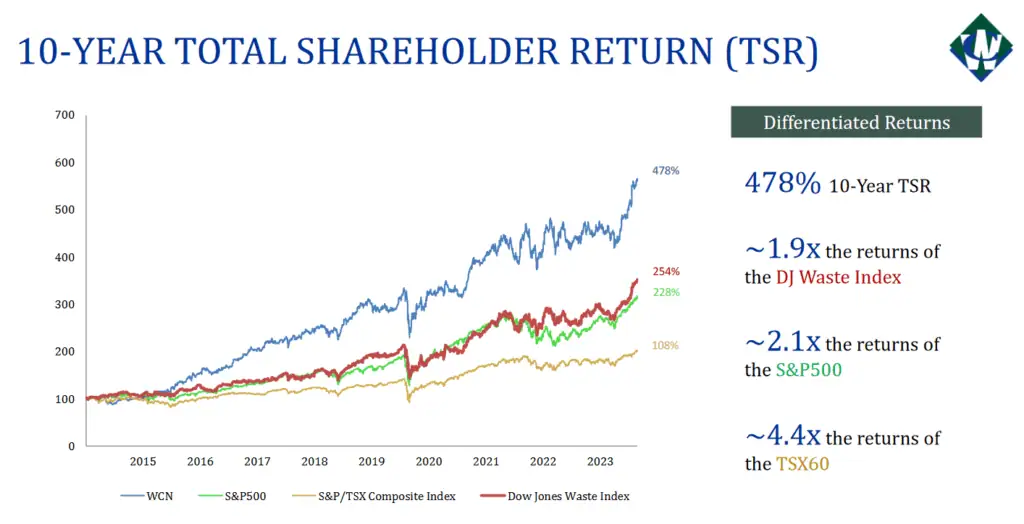

Waste Connections is an integrated solid waste services company that provides non-hazardous waste collection, transfer, and disposal services. Waste Connections also provides resource recovery through recycling and the generation of different renewable fuels. In 2023, the company generated $762.8M in net income and is on track to generate more than $1 billion in net income in 2024 thanks to serving approximately nine million residential, commercial, and industrial customers across 46 American states and six Canadian provinces.

The garbage business is quite profitable for Waste Connections as the company enjoys a +30% margin and continues to improve its margin every year.

The solid company performance shows up on the stock price and shareholders are rewarded handsomely.

Over the years, Waste Connections has been investing in technology and training to improve operational efficiency to further cut down its operational costs.

Although Waste Connections has a very low yield of less than 1%, adding more Waste Connections shares should help us on the total return front.

Potential Risks for Waste Connections

Although it takes a lot of money and investments to start a garbage disposal company servicing the US and Canadian markets, Waste Connections faces tough competition in the sector. One of the competitors is Waste Management, a well known brand in the garbage disposal space and a stock that we own in our dividend portfolio as well. Many of the disposal companies are servicing the same customers and bidding on similar service contracts. So while the business is quite profitable, Waste Connections needs to continue to put a heavy focus on operational efficiency, reduction of operational costs, and ensuring they win future service contracts.

The biggest risk for Waste Connections and other garbage disposal companies is changes in regulations and operational requirements. For example, the local government could impose specific restrictions and requirements that Waste Connections must follow which could increase overall operational cost for the company.

Valuation wise, Waste Connections is anything but cheap. At a PE ratio of over 50, nobody will argue that Waste Connections is not an undervalued stock. And it’s a question of whether the PE ratio will continue to hold steady at around 50 or we will see a share price pull back.

Consideration #2: Brookfield Asset Management

Currently, Brookfield Asset Management accounts for less than 2% of our dividend portfolio. I’d like to bring the overall exposure to somewhere between 3 to 4%. This is an ongoing effort on our part.

Brookfield continues to be one of the best managed companies in Canada. I was thoroughly impressed by the 2024 Investor Day presentation.

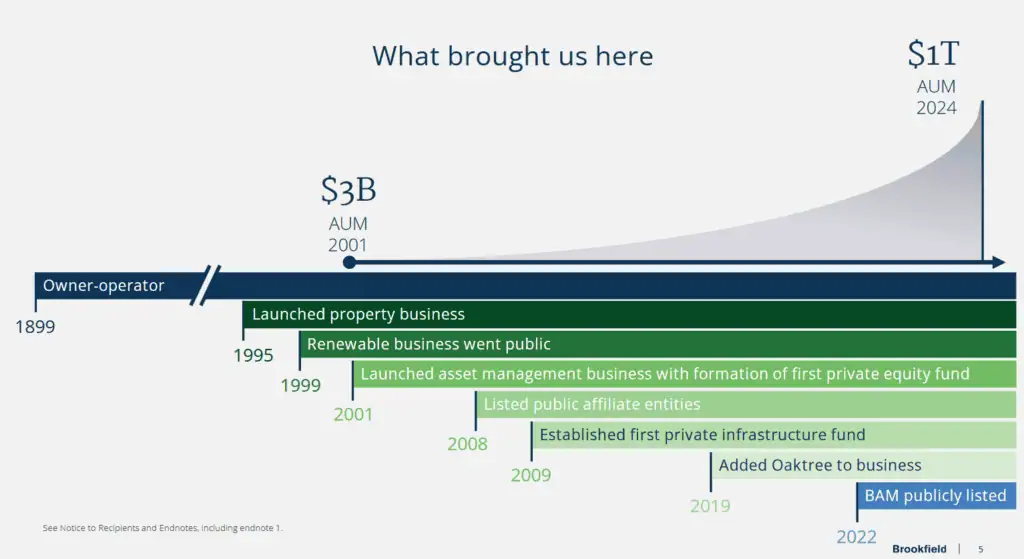

Over the years, Brookfield Asset Management has grown the AUM (assets under management) quite significantly – the company grew its AUM from $3 billion in 2001 to $850 billion in 2023 to over $1 trillion in 2024.

The $1 trillion assets under management span across renewable power & transition, infrastructure, private equity, real estate, and credit, operating in over 30 countries. Thanks to such high AUM, Brookfield Asset Management manages and owns assets and businesses that form the backbone of the global economy.

I picked Brookfield Asset Management over Brookfield Corporation because the yield is slightly higher for BAM. When Brookfield Asset Management and Brookfield Corporation split in 2022, Brookfield, the parent company, set up Brookfield Asset Management so around 90% of its free cash flow would be used for dividend distribution and growing – at a most impressive rate of 15% to 20% per annum – dividend payout.

Another key thing I want to point out is that I believe Brookfield Asset Management is quite under-valued given the vast potential to grow its AUM and dividends in the next five years. BAM plans to move its headquarters to New York city as a way to encourage the US index funds to purchase more BAM shares. If that does happen, it should drive up BAM’s share price.

Potential Risks for BAM.TO

Brookfield Asset Management is one of the many companies under the big umbrella called Brookfield. The Brookfield company structure is very complicated so it can get very confusing for investors that want to have a better understanding of the company structure and cash flow process.

Furthermore, due to the way BAM is set up, dividends will only be paid if the company is profitable and has free cash flow. Therefore, if there’s a recession or even a slight economic downturn, it is highly possible to see a decrease in dividend payout.

Having said that, I believe this is very unlikely to happen given BAM is projecting a double in cash flow over the next five years.

Consideration #3: Canadian National Railway

Many readers will recall that I have consistently listed Canadian National Railway in my Best Canadian Dividend Stocks list.

The biggest reason for purchasing more CNR shares is that the stock has struggled in the past year. So adding more shares will allow us to take advantage of the depressed share price and wait for a recovery.

With a network of approximately 20,000 route miles of track that spans Canada and mid-America, Canadian National Railway is an important company that creates the backbone of the US and Canadian economy.

Why? Because so many goods and services still rely on rail transportation. So when there’s a disruption in CNR services, there’s usually a significant financial hit as a result.

Over the years, CNR has demonstrated robust growth initiatives to drive revenue growth. I have no doubt the company will continue to grow and perform well in the future.

Potential Risks for Canadian National Railway

CNR has faced labour challenges over the years. There have been labour disruptions that negatively impacted the company’s bottom line. Until CNR can ensure no labour disruptions, labour issues will continue to be a significant risk for CNR investors.

The consistently rising labour cost (labourers want higher pay) and higher pension costs will decrease CNR’s profitability. In addition, with a large rail network and a vast amount of machinery, CNR needs to spend a lot of money on maintenance. One potential risk for the company is significant and unexpected maintenance costs.

In other words, CNR needs to continue to improve its operational efficiency, reduce maintenance costs, and ensure its labour cost is in check.

Consideration #4: Telus

Some readers may be surprised by this consideration but please remember that I included Telus in My Five Highest Conviction Positions post a few weeks ago for many reasons.

Yes, Telus has struggled in terms of share price performance over the years but I’m considering Telus for the following reasons (mentioned in the conviction post):

- Telus, like Rogers and Bell, operate in an oligopoly for the Canadian telecommunication space

- Unlike Rogers and Bell, Telus does not have a media business so that puts Telus on a better footing

- It will take a number of years for Telus to build out its 5G stand-alone networks across Canada and this will take more capital investment. However, I believe Telus is in a good position to capture cellular-related revenues moving forward once the 5G network is available across Canada.

- Telus can provide and expand telecommunication-related services like security, healthcare, connected devices, etc to generate more revenues. The technology is a lot more resource efficient than 4G LTE so cost per bit is cheaper for operators like Telus.

- Telus CEO Darren Entwistle announced in May that he would forgo his cash salary in favour of shares to demonstrate confidence in the financial health of Telus. You can say this is a bit of a showy gimmick but for me, when a CEO does that, it says a lot about the long-term strategy of the company.

- Although satellite internet is getting more prominent (i.e. Starlink), I strongly believe most customers will remain with cellular technology. Furthermore, it is not convenient for the Internet of Things (IoT) devices to switch to satellite technology due to regulations. Therefore, I do not believe satellite technology will replace Telus’s cellular based services.

- Finally, Telus, like the other telcos, will continue to benefit from the high immigration to Canada (over one million last year). One of the first things a very high proportion of those new arrivals will need is a phone and a service provider.

Furthermore, with the interest rates expected to continue to drop, Telus should benefit greatly.

Another attractive point for Telus is its high dividend yield and the company plans to continue to consistently grow its dividend payout, usually announcing two dividend increases per year.

Potential Risks for Telus

The biggest risk for Telus is its level of debt and this is the number one reason why Telus’s share price has struggled compared to the TSX over the past several years – investors are very concerned with the high level of debt, the high dividend yield, and the company’s cash flow.

However, as I pointed out in the previous section, with the interest rates dropping and expected to continue to drop, Telus should be able to take advantage and consolidate its debt.

At this point, I think the benefits of adding more Telus shares outweigh the potential risks. I put my trust in Telus’ management to get the share price moving in the right direction.

Consideration #5: Alimentation Couche-Tard

In January, we added 93 shares of ATD with our TFAS contribution. Although I wanted to add more ATD shares, I didn’t manage to do so. Alimentation Couche-Tard currently makes up less than 1.5% of our dividend portfolio and I’d like to increase that to between 2 to 2.5%.

As mentioned, we’d like to increase the weighting of ATD in our dividend portfolio. I continue to like ATD from a long-term growth point of view.

When travelling in Denmark, Iceland, Sweden, and Hong Kong, I consistently saw Circle K convenience stores, demonstrating Alimentation Couche-Tard’s powerful footprint outside of North America. This would be one of the top reasons why we’d like to purchase more ATD shares.

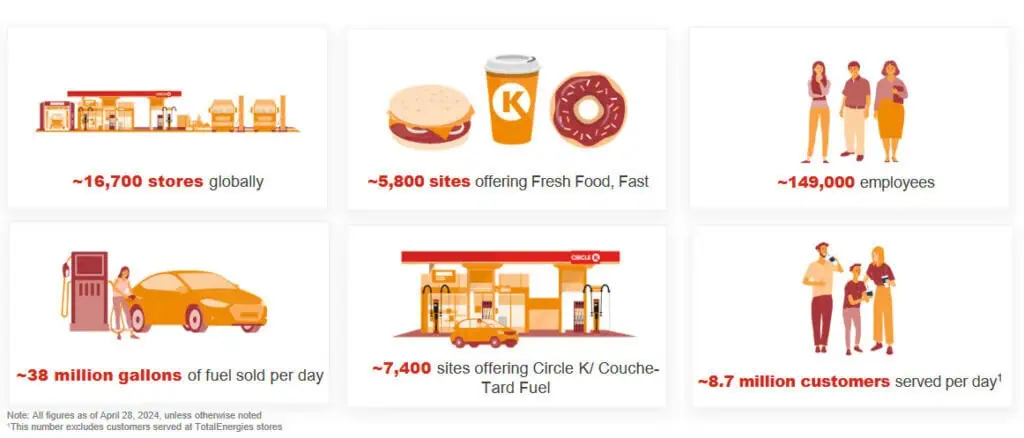

In case you’re curious, Alimentation Couche-Tard operates in 31 countries with over 16,700 stores. ATD and its different convenience store brands provide consumers fuels and convenience internationally.

Since people use convenience stores for “convenience,” ATD’s overall business is relatively recession-resilient.

The convenience food market is more than $700 billion across North America and Europe with 59% of fast-food customers considering purchasing a meal from a convenience store. Not surprisingly, ATD has identified this space as a growth opportunity and has expanded its fresh fast food service in over 5,800 stores globally.

In addition, ATD has expanded and installed new cooler solutions in more than 4,000 stores to capture and retain customers. ATD is also installing EV charging stations to attract traffic to its convenience stores.

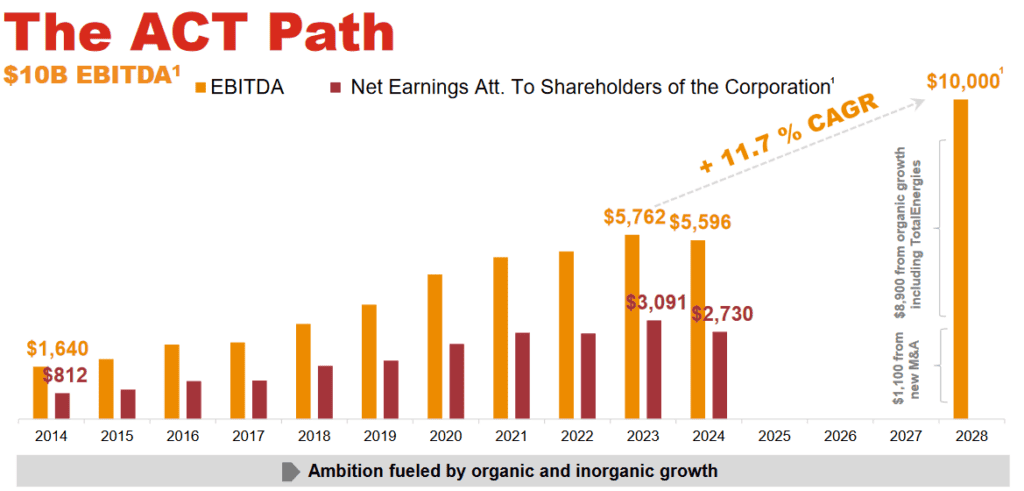

According to ATD’s Q1 investor presentation, the company has a goal to achieve $10 billion EBITA by 2028 which would correspond to a 11.7% CAGR from 2024. Assuming the company can deliver on this goal, shareholders should get rewarded as a result.

Potential Risks for Alimentation Couche-Tard

I believe the biggest risk for ATD is its mergers and acquisitions (M&A) plans.

In early August, Alimentation Couche-Tard announced it made a preliminary non-binding proposal to buy 7-Eleven owner Seven & i Holdings Co in Japan. When the news broke, the share price dropped quite a bit and hasn’t recovered yet.

Although the deal has been rejected by the Japanese owner, ATD hasn’t given up on the idea. Let’s not forget this isn’t the first time that ATD failed to complete an acquisition (ATD tried and failed to acquire Speedway in 2020).

In an acquisition, if the acquirer decides to pull out of the deal, it typically needs to pay a hefty amount of money to the one being acquired. Therefore, Alimentation Couche-Tard needs to be very careful on who they decide to acquire and what price they pay.

Since M&As are costly and take a lot of time and effort to integrate the acquired companies – as well having to obtain regulatory approval – ATD shareholders must be aware of the potential volatility in share price as a result.

Furthermore, although ATD is installing EV chargers to attract traffic, it remains to be seen whether this strategy will generate more revenues or not.

Summary – 2025 TFSA contribution dividend stocks we’re considering

As you can see, Waste Connections, Brookfield Asset Management, Telus, Alimentation Couche-Tard, and Canadian National Railway are five Canadian dividend stocks we’re considering buying more shares of with our 2025 TFSA contribution rooms. With the exception of Telus and Brookfield Asset Management, the other three stocks have relatively low dividend yields.

Please note, dividend yield and dividend income aren’t everything. The focus for every investor should be total return.

Dear readers, which Canadian dividend stocks are you considering adding to your TFSA in 2025?

I find it funny how year after year, you leave US stocks off your TFSA list.

Just because you have a 15% withholding tax on the TFSA US holdings is shortsighted as to the growth they generate.

From your 5 picks, two of them should be considered US stocks, BAM.TO and WCN.TO, frankly both of these pay dividends in USD and are then given to you in CDN at the rate of exchange.

My entire TFSA has not one single Canadian stock in it, I see no benefit from doing that.

About the easiest way to explain it is this.

Say you could have held 1 share of BRK-A in your Investing, RRSP and TFSA since 2009 and you both died tomorrow(not that you died, hypothetically, funds are now part of your estate to the children), what are the tax implications to your children at that time?

That 1 share at todays price and exchange is worth $688,500@1,4375 =$989718,75Canadian 50% capital gains simplified cost of share TFSA contribution 2009 $5000 CDN or 4138.73 US

That single share will have your children handing the government a cheque for roughly $218166.14 if in investment, $425771,98 if RRSP and $0 in TFSA.

I look at my TFSA as an investment machine where quite frankly, if I lost it all tomorrow, I could survive without it. The contribution limit is less than most people’s RRSP contribution limit and that limit only starts once you turn 18 not when you start working.

If you base your argument on what you wrote in your article Does it make sense to invest US dividend stocks in TFSA from May 8, 2023 then that is not considered sound investment advice.

I want to achieve moderate to maximum growth inside of my TFSA and then convert that return into Canadian dividend stocks to generate income once I retire if I wish to keep a legacy.

If not I can just convert my US holdings into CDN by buying canadian banks and do Norbert.

My RRSP will be long gone before that happens and I want to achieve NIGAR or No Income Government Assisted Retirement

In other words, my TFSA does not show as income. Withdrawals, dividends the lot are tax free and therefore not income. As long as my pension and OAS are below the threshholds set for Pharmacare and whatever else low income Canadians get, I am also entilted to it. The best part, that contribution room that my US holdings generated up until now, is there for eternity or until the Canadian government removes TFSAs all together and considers them taxable. My bet, that will happen sooner than later.

Now this may sound crass and it may be, but you don’t get rich by spending your own money.

You keep trying to limit your exposure to taxes and maximizing the amount you get from an OAS.

That TFSA properly invested is exactly the ticket to do it.

Thanks for your input, will take that into future consideration.

The ATD deal with 711 makes sense for me at the right price- an iconic brand and the same line of business. Seems like it could give them a larger moat.

Like your list. Do not have BAM, only BEP. Did not buy due to small overlap. Why not BN instead of BAM?

I have a position in CNR- are you concerned about the possibility of large tariffs from the US and how it might impact this stock since it’s largely tied to the Canadian economy?

You’re right, BN and BAM are pretty close. Picked BAM over BN due to the slightly higher yield.

CNR & tarries…. yes that could hurt CNR but we need to wait and see what happens.

Great List Bob!

Personally for 2025 I will keep it simple and just invest the $7k into XEQT.

That’s a simple and great plan!

I’ve been buying into CNR and CP monthly. I’ve been doing the same with VFV but on a bi-weekly schedule instead. Everything else though is bought when I feel they are reasonably priced.

The CNR/CP buying is an experiment to see which will be in a better position in a decade from now. It’s a competition between my son and I. Most likely I’ll pass down the funds once he graduates college/university, about 10 yrs from now perhaps. It’s only $100 per railroad, per month. I didn’t want to exceed that since I started buying early 2023

On the CAD side on the TFSA, I had also invested in BN, NA, RY, and CNQ. I have a very small position in CCL.B which I may drop before year end. Everything else is USD

I haven’t added to BN in some time as its up 84%, but I’m still watching it.

I had a nice pre-carrefour position in ATD, but had to sell something to cover a sewer repair. I feel bad about it as it did move up plenty since then, but the value was what I needed to cover the repair. It was a 48% gain though. I needed an additional 11k at the time. I didn’t have a good enough emergency fund. That’s important, lesson learned

I used to hold Telus, but that debt seems to be too much for comfort. I also had TD, and I can’t see them gaining growth as easily prior to recent troubles. I’m good with NA and RY. I’m hoping that NA succeeds with that CWB acquisition that’s to close later next year. It’s the largest CAD position with no plans to add more.

I feel that I’m in an okay position now. It’s a work in progress. Recently paid off the house in under 13yrs. No debt for the past 3 weeks since. I still find myself hesitant in buying stocks though with the ‘mortgage’ money. I don’t have a plan on top of the VFV and CNR/CP continual set buying. Sometimes I feel stuck.

Thanks David for your comment. BN is attractive but after up so much this year it can be a little hard to pull the buy trigger.

I’ve been thinking of dumping CNR. It’s down 15% this year and in the 3 years I’ve owned it, has not performed well. In the new year I plan on buying more Dollarama, BN, BAM and VFV. I’ll hang on to what Telus I have but not buying anymore. Thanks for sharing your thoughts. Merry Christmas and all the best in the new year.

Interesting that you’re considering dumping CNR. I like your list. 🙂

It’s purely anecdotal, but I like the garbage mentality. It’s recession proof. I own gfl. was just lucky with a nice increase (most companies increased, so was it unique or a rising tide?.)

Ever see a Costco not busy?

How many amazon trucks did you see on your street today? (they ARE the internet shop)

Do you think Mastercard or

Visa will ever be replaced?

Etc.

thanks for the great blog this year. All the best to you and the readers.

You’re welcome Jeff, thank you for your support.

You may consider putting the tax efficient dividend payers in a non-registered account, if you have other, less-tax efficient investments to put in the TFSA. If you have no other investments to make, then the TFSA is fine: no tax is better than little tax.

Yup, being tax efficient is very important.

Like your growthy ideas (ATD, WCN, BAM in that order based on history and looking forward) for a TFSA. Both CN and T have been “meh” in the last decade (or worse in the case of T unless you sold out in the mid 30’s of valuation madness). T was a beautiful thing pre-Great Recession and even in recovering from the GR but not Why not consider even growthier ideas like CP, GSY, or CSU? Personally, I only have high growth businesses in my TFSA.

Good point on high growth businesses.

If those CNR would be good. Everything else at ATH. Will wait until January. Also hopefully a lot of tax loss selling in Dec so may be some deals soon

Agreed! Hopefully we’ll see some attractive prices in early January.

Great choices on your list.

I would also consider TIH. Great long term returns, +30 Dividend Increases, and the current value is best it’s been in a long time.

Thank you, will need to take a look at TIH.