When I first started as a Canadian dividend growth investor, one of the first questions I had was where should I keep my dividend stocks. Given all the different types of accounts available to Canadians, finding the most tax-efficient way to hold dividend stocks can get confusing.

Before determining which accounts to keep your dividend stocks, first we need to understand the different accounts available to Canadians. In short there are 2 types of accounts you can hold dividend stocks in Canada – regular accounts and tax advantage accounts.

Regular Accounts

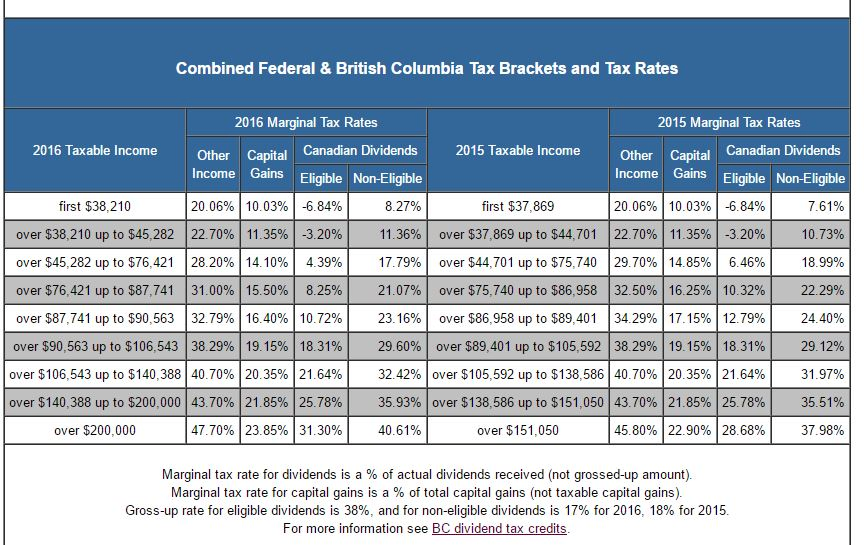

With regular accounts, capital gains and dividends are taxed. However both are taxed at a much lower rate than your working income. For the respective tax rate, this website is a great place to check out.

If you hold US stocks in a regular account, the US government will first collect a 15% withholding tax on any dividend income that you receive. Since US dividends do not qualify for the Canadian dividend tax credit, US dividends will be taxed like interest income (i.e. at your marginal tax rate). Not ideal but you do get a foreign credit for the amount withheld by the 15% withholding tax. The foreign credit can then be applied used for deduction when you file your Canadian income tax.

Tax Advantage Accounts

When it comes to tax advantage accounts, there are a few options available to Canadians. The most common tax advantage accounts are – RRSP, RESP, and TFSA.

RRSP – Registered Retirement Savings Plan

A quick note on opening a self-directed RRSP account. Some brokers will charge an annual fee unless you have certain amount of money in your RRSP account. If you think about it, It’s a silly fee since these brokers aren’t really doing anything for you. So definitely do your research prior to opening a self-directed RRSP.

With RRSP, you’re only taxed when you withdrawal from the account. What makes RRSP so awesome is you get a tax deduction at your marginal tax rate for money you put in. Furthermore, due to tax treaty between US and Canada, you are exempted from paying the 15% withholding tax on US dividends.

RESP – Registered Education Savings Plan

With RESP, you can contribute $50,000 per child until the child turns 31. RESP is meant for post secondary saving for your children. Although you don’t get tax deductions for RESP, the Canadian government will contribute to your child’s RESP to help their savings grow. Such contribution is called the Canada Education Savings Grant. The basic CESG provides up to a maximum of $500 on an annual contribution of $2,500. This grant is available up until the end of the calendar year in which the child turns 17. When RESP is withdrew, the amount is taxed on the recipient’s tax rate. Since RESP is meant for post secondary students, the recipient, in this case, the student, will usually pay little or no income tax due to tuition credits.

Unlike RRSP, you need to pay the 15% withholding tax on US dividend income.

TFSA – Tax Free Savings Account

TFSA is my favourite tax advantage account. The idea is very simple, each year the Canadian government announces the contribution limit. The money you put inside a TFSA can then grow tax free. If you withdraw any amount from TFSA, you won’t get taxed and you can contribute that amount again in the future plus any additional contribution limits. The beauty of TFSA is that any dividends and capital gains are tax free, making TFSA the perfect vehicle for Canadian dividend growth investors. Although TFSA is a registered account, if you receive US dividends, you will need to pay the 15% withholding taxes and will not receive any foreign tax credits.

Ever wonder what happens when you maxed out both your TFSA and RRSP contribution room?

Where should I keep my dividend stocks?

With so many accounts, which accounts should I use for dividend investing for maximum tax efficiency? After a bit of research and calculation, below is a quick summary.

Regular Accounts

- Best for holding Canadian dividend stocks that pay eligible dividends.

RRSP

- Best for holding US dividend paying stocks and US listed ETFs.

RESP

- Best for holding Canadian dividend stocks and Canadian income trusts & REITs.

TFSA

- Best for holding Canadian dividend stocks and Canadian income trusts & REITs.

Notice that I do not recommend holding Canadian income trusts & REITs in regular accounts. Income trusts and REITs typically pass their income, return of capital, interest, capital gain, foreign business income to the shareholders as part of the distribution (i.e. dividend). Each portion will then be taxed at a different rate. This results in complicated tax calculation, especially when you are enrolled in dividend reinvestment plan (DRIP) and sell the shares later. To avoid any headache and complicated math, keep income trusts and REITs inside a RRSP, RESP, or TFSA.

Dear readers, do you follow similar plan when it comes to holding your dividend paying stocks?

It really depends on how much tax-advantaged space you have and what else is in there. As you mention, dividends aren’t 100% tax-efficient but they’re more efficient that things like REITS or Bonds. It’s really all about maximizing tax-efficiency within your available space and if you’re not 100% full in your various tax-advantaged accounts in stocks or funds that are less tax-efficient then dividends should go in there for maximum growth. There’s nothing better than tax-free growth but dividends still have a ton of value in a taxable portfolio if the TA accounts are all full up.

Very true, you need to look into how much tax-advantaged space you have for sure. Would be nice to invest everything in a tax free account but there’s always a limit.

Hi tawcan,

Great post ,, but here in Singapore , since the dividend from REIT will not be tax ,,hence ,we could build our income portfolio including REIT n business trust . Anyway , same philosophy on income investing to achieve financial freedom ..

Cheers ,,,

That’s really cool that in Singapore dividend from REIT will not be taxed.

Non-Reg. contains only CDN dividend paying stocks.

TFSAs include only CDN dividend paying stocks and REITs.

RRSPs are mostly filled with US dividend paying stocks and US-listed ETFs.

Cheers!

Mark

Nice and simple. 🙂

Every interesting Tawcan and there’s a lot more choice than Australia that’s for sure. There’s only 1 type of account, Superannuation, and that’s it (and you can’t access it until you’re at least 60). You seem to have already figured out what’s the best way to approach things, so I hope this helps other Canadians facing the same dilemma.

Tristan

Interesting there’s only 1 account in Australia. I’m really glad that the Canadian government introduced TFSA a few years ago. It changed the retirement saving landscape. 🙂

Is there no way to touch Superannuation before you are 60? Any loopholes?

Very extreme circumstances such as:

You die, so your partner can access the funds (life insurance can also be bought inside this account)

You’re about to go bankrupt, so you can pay off your debts – only as a last, last resort though.

You are permanently leaving the country to live in another country.

We have no plans to need any of these 🙂

Tristan

Ahh very extreme cases. I suppose it would have been nice if Australian government were to introduce a tax free account. It would totally help with retirement planning.

Good info bud even if I’m south of the border

Thanks dividendsandhobbies. I think it’s very similar concept down south too.

Some similarities and some differences. A Roth IRA you can pull money out with no penalty as long as you don’t pull the interest it has earned.

I have two US securities in my TFSA (Target and Vanguard Mega-Cap ETF). I know I could’ve avoided the 15% tax withheld if I get them into my RRSP, however, I needed that liquidity and the ability to cash out to cover certain unexpected expenses.

I do take an advantage of the matching RRSP at work by maxing out my contribution, and trying to approach the $45000 taxable income bracket (15%) after all other deductibles (tuition, tax credits…etc). Ideally, I should aim for the maximum contribution limit (18% of income), however, I am having a hard time saving up for that, and there’s still room in my spouse’s TFSA.

Despite knowing the great advantages of RRSP, however, at this stage of my life, I am still having a hard time buying into it. One being my taxable income isn’t high enough to take the full advantage, and second being the variables in life. Sure it is great to save for retirement early, but putting all my money into that basket feels like I could miss out on other investment opportunities.

Hi Jack,

Makes sense when you talk about liquidity, but personally I would still hold Canadian ETFs and stocks in TFSA not only to avoid the 15% tax but also avoid the currency conversion. Not sure who you use but with some brokers you can’t hold US currency in your TFSA. So when you buy a US listed stock, you need to convert using Canadian cash. When you sell, the money is converted back to Canadian. You get dinged twice on currency exchange rate + bank exchange fees. Not ideal IMO.

Taking advantaging of RRSP at work is great idea. So many people say no to free money, I don’t get that. If you anticipate your tax rate to be higher in the future, makes sense to save up the RRSP contribution for later and focus on maximizing you and your spouse’s TFSA.

I totally feel your pain on currency exchange rate + bank exchange fees.

Unfortunately, my bank – TD Canada Trust doesn’t allow me to directly transfer USD into my TFSA or RRSP accounts, despite they have USD registered accounts. I guess because of tax issues, when transfer USD into the USD accounts, they will have to be converted to CAD then back to USD. (Painful!)

Fortunately, Questrade is able to make direct transactions with USD on any of the registered accounts. As a result, whenever I trade USD securities, I use Questrade. Plus their commission is $5 cheaper than major banks, and free with ETF (when buying).

I am looking for diversification with my portfolio at the moment, and I am having a hard find that solely on TSE. Especially in the sector of Technology and Healthcare.

Wouldn’t transferring USD into registered accounts making it slightly complicated when calculating how much contribution room you still have left?

Oh ya, I did in fact slightly over contributed to my TFSA because of currency conversion. However, with the spreadsheet right now, I can monitor and control it a bit better. I always leave a little bit of buffer in case of discrepancies.

If you slightly over contributed to your TFSA, have you received letters from CRA about the 1% penalty?

No, no penalty letter from CRA yet. We’ll see how it goes near the end of this year. Now I am very careful not to mess with the TFSA limit.

The CRA probably won’t bother sending a letter for a small amount over contribution. We received a couple letters before – https://tawcan.com/over-contribution-of-tfsa-what-to-do/

I can only speak for US accounts, but here we would say that any investment that produces dividends as the primary gains (e.g. – bonds or dividend-centric stocks) are probably better off in a tax advantaged account like a 401k or IRA. Dividends are taxed more punitively (i.e. -as regular income) than capital gains (either 15%, or, if you can get clever with your income in early retirement, 0%), and are less tax efficient investments than, say, your regular old S&P500 index fund.

I think Canada accounts are very similar to US accounts. Not sure how many Americans invest in Canadian dividend paying stocks… from what I understand, if you do that you want to invest in your 401K or IRA.

The caveat is that if you’re planning on living strictly off the dividends from your investments, it might be better for you to have those be accessible somehow. Putting dividends into your 401k or IRA is tax efficient, but it might also be a bad idea for you if you want to access that money.

That’s very true about living strictly off the dividends. Having said that, there are ways to access RRSP before age of 71. Yes you need to pay taxes but if most of your income is from dividends, the marginal tax rate will be low.

I’m not familiar with these type of accounts Tawcan, but I’m curious about withdrawal. Can you withdraw from these at any time, or are there limits/tax disadvantages.

Your focus on this post seems to be about saving, not the withdrawing. Does the round trip change any of those tax implications?

Hi Mr. Tako,

For TFSA you can withdraw at anytime. It’s very different than Roth IRA in US.

For RESP you are only allowed to withdraw $5,000 of accumulated income in the first 13 weeks of post secondary school. After that you can withdraw as much as you like. If your child does not attend post secondary, you can collapse the plan. The contributions are tax free, anything else (accumulate income) is added to the subscriber’s gross income for tax purposes (taxed at 20%). You can also transfer the amount to your RRSP, providing there’s enough RRSP contribution limit. Again if you do that some portions are taxed.

For RRSP you can hold it until age 71. At 71 you can either withdraw RRSP, transfer into a RRIF (Registered Retirement Income Fund), or purchase an annuity. For RRIF option, the Canadian government has set withdrawal rate & amount each year (increases every year). For someone like me who plan to use RRSP before I turn 71, you can withdraw money from RRSP. But you will need to pay withholding tax – 10% on amount up to $5,000, 20% on amount between $5,000 to $15,000, 30% for amount over $15,000. The left over money is than taxed at your marginal tax rate. RRSP is a bit complicated but if your income bracket is low, you should be able to recover quite a bit of the withholding tax.

I follow a very similar plan as this but one thing I struggle with is should you design your portfolio this way right off the bat or start with maximising the registered accounts?

For example I have dividend paying Canadian companies in a TFSA that belong in the non registered account. I wanted to maximise the account first before opening a non-registered account. Now I ask myself if I should sell and repurchase in a taxable account to make room for Canadian REITs in the TFSA.

Does anyone have any insight?

Hi Q,

I would maximizing the registered accounts first. There’s nothing wrong with holding dividend paying Canadian companies in a TFSA. In fact, we do that as well. All I’m saying is that if you decided to hold REITs and income trusts, hold them in your TFSA rather than in a taxable account.

Say for example I wanted a portfolio consisting of 50% ETFs and 50% DGI. What I meant was should the portfolio be constructed with the end goal in mind meaning that eventually ETF’s inside a TFSA will be $46500 and the DGI portfolio (non registered) is also $46500?

Or do I maximize the TFSA first (let’s say 50% ETF and 50% DGI) and then transition to the overall portfolio design?

My thoughts are in the beginning taxes are saved however as the transition happens more commissions will be incurred.

For the sake of simplicity, I have ignored the RSP because the question applies to this account as well.

Hi Q,

If I were you I’d maximize the TFSA first at 50% ETF and 50% DGI. Once TFSA is maximized, I would implement the same strategy in non registered accounts. Having said that, this is really a personal decision as you need to take commission fee into consideration. You also need to consider whether you will eventually sell these stocks or not and the capital gain consequences.