When I read Physician on Fire’s recent post on Financial Independence vs Financial Freedom my brain went wild (like spidey sense wild!) and I started wondering – Do we go through our life in different financial stages? Just like the well-known four stages of competency, I believe we do go through similar stages with our finance. Below are the four different stages of financial competency that I believe we all go through in life.

1. Financial incompetence

Most of us are financial incompetence at some point in our life. We have no clue about personal finance and we don’t manage our money well.

How do you know that you are financially incompetent?

- You spend more than what you earn (i.e. expenses > income)

- You think credit card is the saviour for all your financial problems

- You carry a large amount of consumer debt

- You celebrate when you receive an approval for another credit card, because you can put your current credit card balance on the new card, or you have more credits to spend

- Your retirement account has a lot of zeros -> $000,000.00!!! (imagine using this as a pick up line! Oh boy!!!)

- You fail to see the need to gain personal finance and retirement related knowledge

Fortunately, many people move out of this financial incompetent stage at some point.

2. Financial competence

The next stage is called financial competence. You finally realize that you are financially incompetent, so you start learning more about personal finance and investing. You start taking charge of your finance by making changes in your life.

You’re in the financial competence stage when…

- You start having a budget and track your expenses

- You pay yourself first

- You live below your means

- You pay credit card balance in full each month

- You start investing for retirement

- You look and ask for help to improve your finance

- You start reading books and articles on personal finance and retirement related topics

Unfortunately not everyone will end up moving to the 3rd stage of financial competency.

3. Financial independence

I have been focusing on this stage of competency a lot on this little blog of mine. To me, financial independence means more choices and more freedom in my life. I get to decide what to do with my time instead having to slave away at a job for 5 days each week just to get a pay cheque every 2 weeks.

How do you know that you are financially independent?

- Your investment is 25x of your annual expenses (If you’re using index ETFs)

- Your passive income equal or exceeds your expenses (dividend growth investors would go under here)

- You no longer worry about running out of money if you continue your current lifestyle

- If you are working, you can quit your job at anytime without having to worry about the lack of working income impacting your life

- You are working because you choose to, not because you have to

- You are completely debt free (some may argue this isn’t a requirement for being financial independent)

For us, I believe we can become financial independent with a dividend portfolio of about $800k. Still a bit of work to do that’s for sure!

4. Financial freedom

Before reading Physician on Fire’s article, I have been using the term financial independence and financial freedom interchangeably. I used to think they are the same thing but I had an epiphany. Financial freedom is the ultimate stage of financial competency! You have even more power and choices when you are in financial freedom than financial independence. You can decide to live slightly less frugal, you can travel more, you can spend a year traveling in high cost of living countries, you can stay at hotels when traveling rather than Airbnb and hostels, you can go to fancy restaurants and order the expensive items, and etc. You can do all these things without regret, without having to worry about money, because your investment or passive income can cover the extra expenses.

What is financial freedom? Physician on Fire defined it as:

- Your core spending + 2x discretionary spending

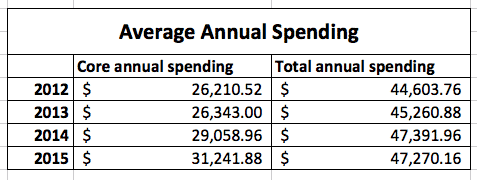

In our case where we tracked our expenses for the past number of years:

Based on 2015 our core annual spending was $31,241.88, discretionary spending was $16,028.28.

Using PoF’s formula, that means to be financially free, we would need $63,208.44 of passive income per year ( $31,241.88+ 2x ($16,028.28) ), or about $1.6 million (25 x $63,208.44).

When we made our financial independence assumptions, I estimated an annual core spending of $27,240 and an annual discretionary spending $11,400. Using these numbers, financially freedom means we would need $50,040, over $13k below the numbers based on our 2015 numbers.

Looking at our discretionary spending, I think our numbers are extremely low compared to other families.

So what does this mean?

- Our core and discretionary expenses are pretty low already

- We have very conservative financial independence assumptions

- Perhaps the 2x multiplier needs to be adjusted depending on your household expenses.

What if we change the multiplier to 5x?

Take our 2015 numbers, that would take us to $111,383.28. (~$2.8 million of assets needed).

Take our FI assumptions, that would take us to $84,240. (~$2.1 million of assets needed).

What’s the correct number to reach financial freedom? Honestly I don’t know but I think we would live in extreme luxury with an annual spending of $112k. Spending $112k per year seems like a dream! To do this, all I know is that we would need to continue to grow our dividend portfolio to reach financial freedom.

Dear readers, what’s your financial competency? What’s your magic number to achieve financial freedom?

We first try to reach stage#3. Part f our ideal life is to keep generating income. Maybe, one day we would reach stage#4. That would be awsome…

Doubling our discretionary spending could be fine. maybe, I would go for 3 times… Oh, what a dream

Our focus is stage #3 as well. 🙂

I came across this posting through PoF. I still haven’t hit Stage 3 yet, although I am guilty that I don’t track my spendings but am aware of my expenditures. My hunch is that my discretionary spendings are relatively high. Perhaps I will start tracking in 2017!

I think aware of your expenditures is juts as important as tracking your spending. It’s a great idea to start tracking expenses.

Working hard on #3 right now.

I believe I am at the pinnacle of my spending life having 3 young children in every sport and activity known to man.

Our total expenses for our family of five on a single income is just under $30,000 but I have no debt or mortgage.

I could probably drop this number down to the low 20s but I like to take the family on at least 2 good vacations a year.

I’m not sure when I would move to number 4. I’m not in a huge hurry but it would be nice to sleep in for a change 🙂

Wow $30k for a family of 5 is pretty amazing! And I thought our numbers are pretty low… time to go back to the drawing board.

I definitely see the appeal of moving from #3 to #4 — what a luxury to never again worry about money or fret over relatively small fluctuations in spending! The challenge, of course, would be that it would be mighty easy to get used to that lifestyle, and pretty soon the indulgences could be just part of your normal routine.

It’s definitely appealing to move from #3 to #4… but if your expenses keeps going up as you try to reach #4, you may never reach that point and may end up falling back to #2.

I’m definitely in stage 2…but I retreat to stage 1 when it comes to investing more than I care to admit! I don’t know what our numbers are because I’m still not sure that we would actually leave the classroom early. Though with the state of public education in the States, it might not be a total choice to stick it out. This is fascinating. I’m bookmarking this post to do some number crunching this weekend!

Would love to see your numbers. 🙂

I like to think in simple terms and financial independence means freedom to me in that I never have to worry about starving or having a place to sleep. As long as my passive income covers my core expenses i can sleep at night. As far as my discretionary spending goes I still generate passive income my “fun money” and I spend it all on fun experiences for me and my family. I really don’t save anymore but invest my active income in things that interest me. If I need more fun money I just work a little extra. Simple and sweet!

That’s a great way to put it. If you need more fun money, just work a little extra. 🙂

I definitely like the idea of a systematic buffer above and beyond the 4% rule, if only to account for the fact that expenses might rise quite a bit in the next 5 or 6 decades. Financial Freedom has a nice way of doing that.

As with everything, systems, systems, systems are the key to success.

Agree that everything comes down to having a system that works for you. What works for you might not work for me though. That’s the beauty and fun of personal finance. It is personal!

Hey Tawcan,

Nice post! 112k in annual income would be fantastic!

For me there is this one magic number. I think I can stop working if I would have 300.000 in my brokerage account.

Based on a calculation of 1 percent yield per month this would generate 3000 gross income a month.

keep it up!

best regards

Chri

How did you get 1% yield per month on $300,000? That’s 12% yield, is that realistic?

Hey Tawcan,

this the advantage of options trading in a dividend portfolio.

In november my yield on capital was at 3,8%. yield to date 27%.

a 12% annualized yield is more than conservative trading options. Nobody would do it if the yield was lower.

best regards

Chri

I loved PoF’s article on this and had a similar “aha” moment as I was using both terms to mean the same thing. Our spending is similar to yours and I can’t imagine spending over $100K a year either! But we should be in a position with pensions, SS, and rental income to actually make close to that a year at some point down the road. I considered that level “independence” but now the “freedom” makes more sense too!

That’s great you have pensions, SS and rental income that will eventually allow you to reach $100k per year. That’s fantastic!

For me, financial freedom came when I realized I could stop budgeting, stop tracking my expenditures, and stop watching the stock market. I can stay off the corporate ladder, and have fun traversing the corporate lattice. I can afford anything that brings me value or improves my health, wealth and happiness, but I also don’t feel any desire to buy things just to show others my financial status. I have the freedom to journey the world instead of just travel. It is the ultimate of peace, harmony and discovery in my life.

That’s a good way to define financial freedom. Sounds like you have the right idea in your mind. Freedom to journey the world and have peace and harmony in life is great.

Interesting to make a difference in stages. We currently spend around €40K a year, this also including discretionary (like Mr. Tako).

The beauty of growing dividends is that if we reach financial independence, our income continues to grow. So we could basically ‘retire’ and just wait until we reach financial freedom.

2x discretionary spending on top of the core spending will probably suffice. Although when our mortgage will be paid off, our core spending will be that much lower we might want to up our discretionary spending a bit.

Agree about growing dividends. That’s one of the reasons I like dividend income so much. The idea that dividend income will keep up with inflation is pretty enticing. 2x discretionary spending on top of core spending should be sufficient but if you plan to travel more, maybe you need to budget a bit more.

Nicely done, Tawcan.

One caveat I’d like to emphasize is that you can gain financial freedom and promptly lose it if you actually double your “discretionary” spending. If you become accustomed to the higher level of spending on luxuries, that becomes the norm and you’re now back to plain vanilla financial indpendence.

The concepts of the hedonic treadmill and Make it a Treat still apply.

Cheers!

-PoF

Yeah the idea of doubling your discretionary spending right away is idiotic. If you do that, you probably will never achieve FI in the first place.

Pretty good stuff! I haven’t through about financial freedom in that context. We spend about $55k per year currently. The discretionary part is not that big. I’ll have to check how much it is. Probably around $15k to $20k. The problem with basing the formula on discretionary spending is that it can be unstable. We’ve started traveling internationally again over the last 2 years and that increased our discretionary spending. We’re at a comfortable level now and I don’t really want to spend more.

Hi Joe,

Totally agree that basing the formula on discretionary spending is unstable and unsustainable. It’s finding a level that you’re comfortable with and stick with it.

We currently spend about $50k per year, but almost half of that is “discretionary”….mainly it’s spent on the kids.

I think to feel really financially free, I’d like to have some of that money to spend on myself so 2x on discretionary income sounds good. That would be about $75k per year….

I don’t think we’ve ever spent that (even before kids), so we’d probably have to work pretty hard to spend that much!

Yeah same for us, we are naturally quite frugal. Hard to imagine spending over $100k per year.