I receive investment-related questions from readers regularly via emails. I really welcome these emails as they are a great method for me to interact with my readers. Furthermore, I really enjoy these emails as they allow me to explore investment ideas that I may have not encountered or explored. Therefore, if you’re a reader and have investment-related questions, feel free to send me an email with your questions.

Today I will go over a few investment questions that I have received over the last few months.

Please remember, I am not a financial advisor. I am simply expressing my opinions. Please buy and sell investments on your own judgment.

Q1. What do you think about investing in non-Canadian government bonds that offer much higher yields?

Here’s a bit of background on this question before I provide my answer.

The reader wanted to diversify his investments and improve his returns. He was looking at the government bond yields and found a lot of countries offer really high rates. For example, Mexico, Bangladesh, India, Brazil, and Pakistan offer 6 to 12% across the entire range of potential maturities. In comparison, the Canadian government bonds have around 1.5% yields.

As you may recall, a bond represents a loan made by an investor to a borrower (i.e. government). Bonds are typically used by governments and corporations as a way to borrow money to finance projects and operations. Bonds have an end date when the principal must be paid and there are usually variable or fixed interest payments throughout the borrowing period.

Government bonds that have really high yields are typically from countries that are in financial distress. As a result, there are risks purchasing government bonds from these countries.

For one, the government is likely to default on the bond you purchased. When a loan defaults, you won’t get your principals back. Imagine buying a 10-year government bond for $10,000 that yields 12% annually. You are supposed to receive $1,200 per year, or $12,000 in total when the bond matures (this is a simplified example). What happens if the government defaults in the third year? You have received $3,600 in interest payments but you’d be in the red for $6,400. You would lose more money if you were to re-invest the interests each year and purchase more bonds.

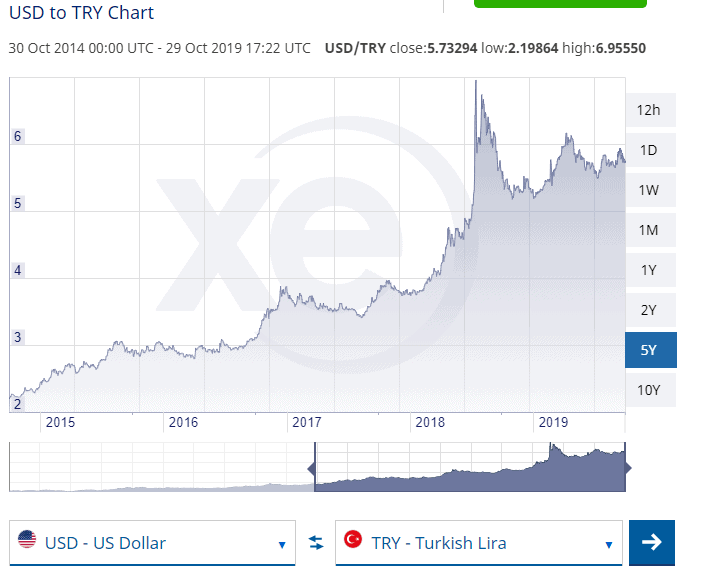

But what about countries that are unlikely to default? Another very important factor to consider is currency risk. Mexico’s government bonds are yielding around 7% currently, but what happens if the peso were to depreciate by 10%? The entire yield from the Mexico government bond would be cleaned out (since the bond is in peso). Some people invested in Turkey bonds back in 2018. The bonds had decent yields but any gains were completely offset by a major devaluation of the currency.

Another problem is when the country is in hyperinflation. In a hyperinflation, the currency used to make those cash payments is worth much less than the original. This essentially makes a bond worthless. In addition, during hyperinflation, a country’s currency gets devalued greatly as well. As a foreign investor, you will end up losing a lot of money.

Be careful with these high-yield government bonds!

Q2. Are there drawbacks to investing in a large number of stocks (i.e. 100 or more)?

The reader asked this question because he was wondering about portfolio diversification. His rationale is that when you hold more than 100 stocks, you are spread out across more stock which should minimize your overall risks in case a company falls into bad times.

There have been a lot of studies on the number of stocks to hold to give the best portfolio diversification. Research suggests as little as 12-18 stocks can provide sufficient diversification.

Now you may be able to diversify more if you hold more than 100 stocks, but you may end up spending a lot more time to monitor these stocks. In that case, maybe it makes more sense to simply purchase a passive index ETF so you can have more free time on your hands.

If I look at our dividend portfolio, we currently hold 60 individual dividend stocks. This is more than what research recommends. We can probably trim a number of stocks out of our portfolio. At the same time, I don’t mind spending time monitoring how these companies are doing.

I suppose how many individual stocks you hold is really a personal preference.

A bit of terminology first. An option is a contract that gives the buyer the right, but no obligation to buy or sell the underlying asset at a specific price on or before a certain date. A call option gives the holder the right to buy a stock and a put option gives the holder the right to sell a stock.

What makes things a little bit confusing is that you can also sell calls and puts. Allow me to explain a bit more…

When you buy a call option, you have the right to buy shares at the strike price until the option contract expires. When you sell a call option it means you will sell the shares at a specific price. How does it work? Imagine an investor purchased a call option on Royal Bank with a strike price at $100, expiring in three months. This gives the call buyer the right to exercise the option of paying $100 per share and receive the shares (in 100 shares quantities). The seller of the call would have the obligation to deliver those shares and be happy receiving $100 for them. A call buyer seeks to make a profit. The buyer wants to see the share price rise. So if Royal Bank’s price goes to $120 before the contract expires, the buyer can exercise the contract, purchase the shares for $100, and immediately get a $20 profit per share. On the other hand, the call seller is making the opposite bet, hoping for Royal Bank’s stock price to decline. Say Royal Bank’s stock price is below $100 by the time the option contract expires, the contract is unlikely to be exercised. The call seller then pockets the premium.

Put options work the opposite.

When you buy a put option, you have the right to sell the underlying stock at a predetermined strike price until a fixed expiry date. A strategy for dividend growth investors is to buy put options to “protect” their gains and any downside risk. For example, imagine you hold Visa with a book value of $15 and Visa’s price today is $185. You may be concerned about Visa’s performance near term, so you buy a put with a strike price of $180 that expires in 2 months. Essentially, you are buying the right, until the option contract expires, to sell your shares for $180. The investor that sells the same put contract would have the obligation to purchase the shares for $180.

Now you know a little bit about option terms. Covered call ETFs sell call options on a portion of the securities they own. It’s called “covered” call because the ETF already owns the stocks on which the call contracts are written. This lowers the overall risk slightly.

When an ETF sells a call option, it then collects a premium from the option buyer. The premium then gets used by the ETF for the monthly dividend payout to its investors.

Generally speaking, when the market is volatile, covered call ETFs should exhibit less volatility than the broader market. The benefits of holding covered call ETFs are that during a volatile market, the monthly dividend should increase and covered calls provide some downside protection.

Sounds great, right? Who doesn’t want to get paid 7-10%? What’s the risk?

However, in a bull market where the stock price is going up, you may lose potential profits by selling covered calls.

For example, say Royal Bank’s price is $100 and the ETF sells a covered call option on Royal Bank shares for $105 at a specific date and receives a premium for this option contract. As long as Royal Bank’s price doesn’t go above $105, you are good. But if Royal Bank’s price jumps to say $120 because of the crazy bull market frenzy, then you can lose out on a gain of $15.

So what do I think about these covered call ETFs overall? Well you can take a look at this article I wrote called Should I invest in high yield covered call ETFs.

Overall, I think there is validity to take a closer look at these covered call ETFs as an income supplement with a combination of passive index ETFs and individual dividend growth stocks. But don’t get hooked on the high yield. Just like individual dividend stocks, higher yield means higher risk. Therefore, it may make sense to purchase small positions of QYLD or RYLD and monitor them closely to see how the ETFs perform over time.

Dear readers, what do you think about my answers? Do you agree or disagree? I’d love to hear your thoughts.