I was talking with a good friend of mine the other day about work, money, and life. Due to the professions he and his wife are in, they both work long hours. He mentioned that he worked 6 days straight and his wife worked 7 days straight the past week and they often don’t see each other for days. I could tell that he was not enjoying this type of working arrangement and wanted to step back a bit.

“How much do you need to retire at age 45?” My friend asked.

“Is a million dollars enough? Two? Three? How much is enough?”

Contrary to popular belief, I don’t think the how much question can be answered by a set dollar amount in your bank account. As J. Money ingeniously stated, the most important factor determining your “number” is your SPENDING. A family spending $20,000 per year will certainly not need as much money to sustain similar lifestyle in retirement compared to a family spending $150,000 per year.

While I have calculated that we can reach financial independent in about 10 – 15 years based on The Early Retirement / Financial Independence Spreadsheet, it doesn’t tell me exactly how much money we need in our bank account (or rather, our investment portfolio) to retire early. So I decided to run some projections based on our spending from the last few years.

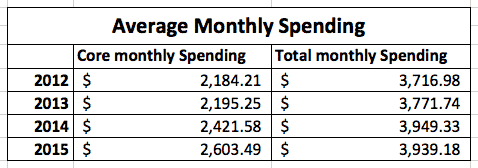

Since mid-2011, we have been tracking all of our expenses via a spreadsheet that we created. Below are our monthly core spending and total spending averages (2011 is not included because we didn’t have numbers for the full year). Some explanations first… By core spending I mean housing expenses, utilities, food, insurance, gas and other essential expenses. Expenses like donations, eating out, entertainment, educational courses, vacations, and some one time big items like a baby stroller have been excluded from core spending. I consider these expenses discretionary spending. We can probably reduce the number of vacations or how much we eat out in order to cut back on these discretionary expenses. But we spend money on these discretionary expenses as a way to enjoy our lives. I don’t believe you can enjoy life fully with extreme saving methods like eating ramen noodles every single day, or avoiding vacations by never setting foot outside of your home. Yes you can definitely save a lot of money but are you enjoying your life? Life is all abut having the right balance. Anyway, as I was explaining, the total spending amount includes these discretionary expenses. As you may know from my recent interview with Mr. 1500, I am a part time photographer and Mrs. T and I are operating a cookbook business. Mrs. T also has other business projects that she’s working on. Since some of these expenses are one time occurrences and the amounts are different each time, to keep things simple, we have excluded these business expenses from the total spending and track them separately.

From 2013 to 2014, our core spending have increased by 9.3%; from 2014 to 2015 the core spending increased again by 7.5%. Similarly, the total spending increased by 4.7% from 2013 to 2014 but stayed about the same from 2014 to 2015. The monthly core spending increase over the last couple of years can be contributed to having another person in the family, higher housing expenses when we moved from an apartment to a house, higher insurance cost, focusing on eating healthier, and some one time expenses like buying a chest freezer, LED light bulbs, and garden tools & plants. Ideally I’d like to see both our core spending and total spending monthly averages go down a bit this year. 🙂

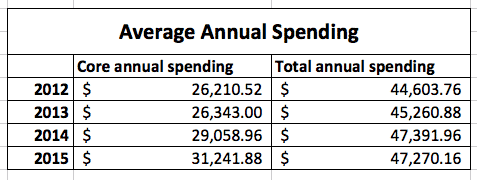

Based on these monthly average spending, our annual spending looks like this.

So an annual income of $32,000 will roughly cover our core expenses and we’ll need roughly $48,000 to cover all of our expenses, excluding business expenses. Since these two numbers are after tax amount, the actual pre-tax income needed to cover the total annual spending will be higher, depending on the income tax percentage.

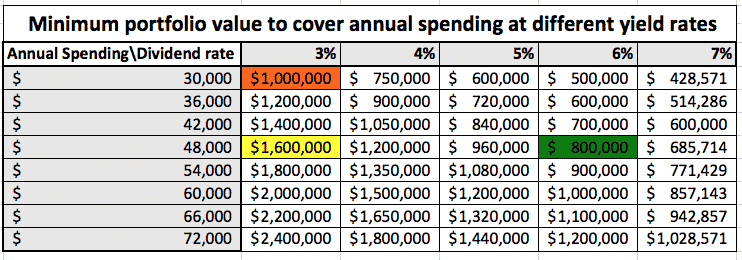

What dividend portfolio value do you need to retire?

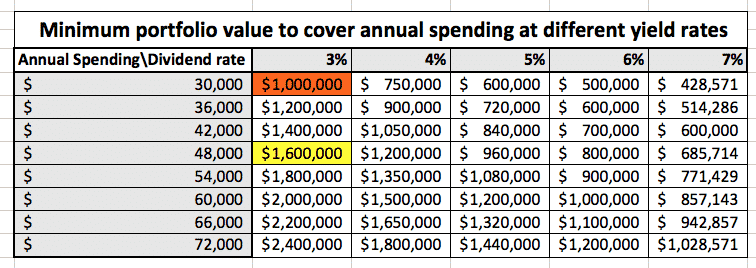

As we plan to use dividend income to cover most of our expenses once we reach early retirement (aka financial independence), let’s see how much money we need in our dividend portfolio to cover our annual spending. Below I ran a few different scenarios using different dividend yield rates.

When it comes to dividend income, one key point to note here is that dividend income is very tax efficient, as dividend income does not get taxed at the same rate as your typical working income here in Canada (US too, I’m unsure about other countries though). FrugalTrader has pointed out recently that BC does not tax anything on eligible dividend income until over $100,000, assuming the income is split between the couple. The beauty here is that, unlike earning income from a regular 9-5 job, divided income is taxed at a much lower rate. That means we only need the actual amount (i.e. $48,000) to cover all of our expenses from dividend income versus what we would need from a regular job, say with a 25% tax for example (i.e. ~$64,000).

[the_ad id=”1878″]

At a conservative dividend yield rate of 3%, we’d need $1.6 million (highlighted in yellow in table above) to cover our annual expenses of $48,000. Not going to lie, that number seems extremely big to me. But what if we look at core spending only? The portfolio needed, at 3% dividend yield, to cover our core expenses of $31,000, would reduce to about $1 million (highlighted in red in table above). That’s definitely a smaller number to aim for.

This is great, but how the heck are we suppose to save $1 million dollars?

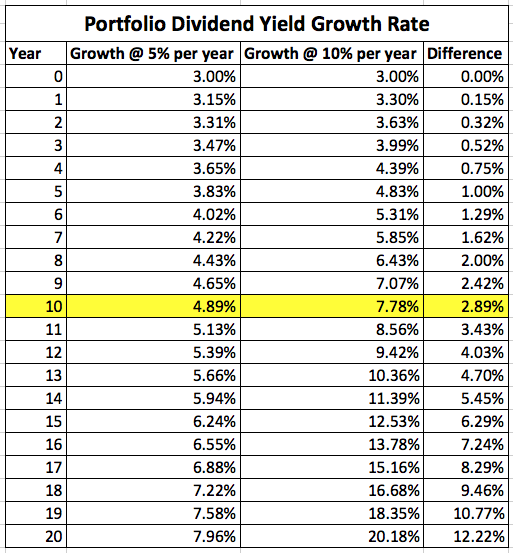

Well, here’s the reason why I love dividend growth investing. The dividend stocks that we hand-picked for our portfolio should increase the dividend payout each year. Solid dividend stocks like Johnson & Johnson, Target, Wal-Mart, have increased dividend payout for over 40 years. Our dividend portfolio may only yield at 3% today, this number should increase as demonstrated below.

As you can see from the table below, if our portfolio dividend payout grows at a 5% rate per year, the yield on cost will be 4.887% in 10 years; if our portfolio dividend payout grows at 10% rate each year, the yield on cost will be 7.781% in 10 years. The power of compound interest takes off as time goes by. Notice that the percentage difference between the two growth models becomes very significant after year 12. Can you imagine 20 years from now having a dividend portfolio with a 20% yield? Wow! This is without having to touch the principal at all. Furthermore, the yield on cost will continue to grow each year as long as the dividend stocks raise their dividend payout. Pretty amazing stuff if you think about it.

Since Rome wasn’t built in one day, neither will your dividend portfolio. If you build your dividend portfolio over time and allow the dividend payout to grow, I believe a 6% dividend yield is not unlikely in 10 years time. This is one of the reasons why we’re focusing on high growth dividend stocks nowadays whenever we buy a dividend stock. Given a yield on cost of 6% for our dividend portfolio 10 years from now, we’d only need $800,000 (highlighted in green below) to cover our $48,000 annual spending. This is significantly lower than the original $1.6 million estimate earlier – a $800,000 or a 50% difference! At this point we can call ourselves financial independent. The dividend income will sustain our expenses. We don’t need to sell any stocks to pay for our expenses. In other words, there’s no need to consider what withdraw rate to use in retirement. Furthermore, the dividend income should continue to grow, as dividend paying companies in our portfolio continue to raise their dividend payouts. In the ideal situation, we would never need to sell any stocks and just live off the dividend income. But we can always sell some stocks to cover one time expenses. Dividend growth investment strategy provides flexibility in retirement years.

What are the key lessons for dividend investors?

- You don’t need millions of dollars to retire early – no you really don’t, especially if your expenses are low. If you have no idea what your annual spendings are, it’s a great idea to start tracking it today. If your annual spending is high (i.e. in the hundred thousands range), you may want to look at the lesson below.

- Reduce & optimize your expenses – a $5 daily expense means an annual expense of $1,825. At 3% dividend yield, you’d need $60,834 in your dividend portfolio to generate enough income to cover this $5 daily expense every year. One way to reduce the core expenses is perhaps consider moving to a cheaper city. This is why Mrs. T and I are planning to travel around the world one day with our kids.

- Focus on dividend growth rather than initial yield – dividend growth rate is more important than the initial yield if your retirement timeline is 10 years or more. However, if you’re planning to retire in a year or two, perhaps you need to focus on the initial yield. When I first started investing, I definitely fell for the dividend yield rate trap. I purchased some stocks that didn’t have the fundamentals to sustain high dividend yield rate. Instead of growing dividend payout each year, some companies couldn’t grow their dividends, some even had to cut their dividends.

Based on all the numbers provided in the multiple table and your annual spending amount, can you determine the magic number that you need to reach financial independence via dividend income?

P.S. Aren’t spreadsheets awesome?

P.P.S. : As pointed out by some readers, YOC may not be 100% accurate since your new investments may not grow at the same rate as original/older investments. The key point of this article is that given the need of $48k annual dividend income to cover our expenses, we don’t need $1.6M in our dividend portfolio. Since we will investing over a long period of time, dividend growth means the actual amount of money needed to generate $48k annual dividend income will fall somewhere between $800k and $1.6M.