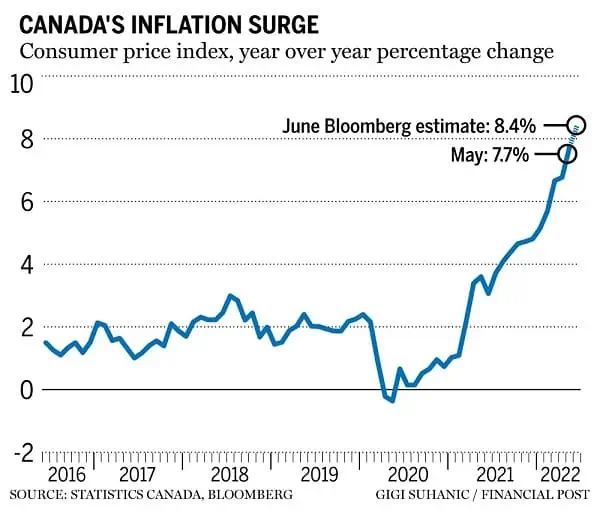

The May consumer price index increased 7.7% from a year ago. Bloomberg estimates that the June inflation rate might be 8.4%! The actual June inflation rate was 8.1%, making it the fastest annual increase since 1983. We certainly haven’t seen such a high inflation rate since the early 1980s.

Are we ever going to see the inflation rate go back down to the long term target of around three percent? That all depends on how central banks around the world do with the interest rates over the next little while.

Earlier this month, the Bank of Canada surprised everyone by hiking the benchmark interest rate by a full 100 basis points. At 2.5%, the benchmark interest rate is still relatively low. However, as the high inflation rate continues, the BoC will be forced to continue with the rate hike. I would not be surprised at all if we end up the year with the benchmark interest rate between 4 to 5%.

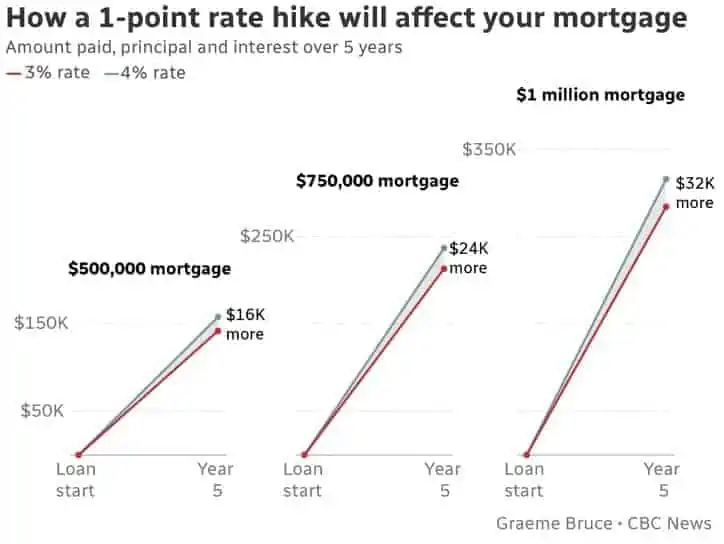

The recent rate hike will hurt many Canadians, especially those Canadians with variable-rate mortgages and Canadians that are already strapped with their expenses. Just how much a 1% rate hike will affect your mortgage? CBC provided a few good visual representation of the impact.

Are Canadians going to have the money to pay the extra interest? If you have a $500k mortgage, you need to pay extra $267 per month due to a 1% interest hike. Are we going to see more mortgage defaults and people losing their homes in Canada if interest rates keep going up? Even if you’re renting, chances are you might see some sort of rent increase as landlords may want to pass down the increased mortgage interest to renters.

In addition, there are rumblings that the job market appears to be getting cooler as more and more companies are slowing down on hiring spending.

Things are getting more expensive thanks to the higher inflation rate, borrowing money is going to cost more because of the higher interest rates, and a slower hiring spending may result in layoffs as companies try to cut operation expenses. All these factors combined, things may get ugly pretty quick!

So, is a recession coming?

I can’t predict the future but it certainly looks like a financial storm (aka recession) is brewing.

Recession or not, it is outside of our control. We really should stop worrying about it. Instead, I believe we need to focus on things that we can control to mitigate the potential risks. These things include but are not limited to:

- Spend less than you earn

- Diversify your income streams

- Have a well diversified portfolio

- Use TFSA & RRSP to minimize your taxes

- Focus on the long term – time in the market

- Set some cash aside, but avoid keeping too much on the sidelines

Good reads from the PF community

Here are some great articles I’ve come across from the personal finance community.

I’ve followed Liquid from Freedom 35 Blog since around 2013 (possibly earlier?), way before I started this blog. So it was really amazing to see that he has quit his day job and outlined what he’s doing next – “What would it take for me to continue working? Right now I value my time at $200 per hour. So if I don’t get an offer for that price I won’t do it. There are exceptions of course. If Pixar offers me a job as a story board artist because they like my stick figure drawings I would probably bend my rate a bit for them, lol.” Congrats Liquid!

Matt, whom I had the pleasure to meet in person a few years ago, explained how to create wealth during a recession – “buy more assets at cheaper prices. This is the most universal, simple, and basic advice I got in this article: If you are young and in your wealth-building stage, a recession is a great opportunity for you to build more wealth faster. Dollar-cost average your way through a recession and embrace the discounts.” I can’t agree more!

Leif has his wife from Physician on FIRE have been homeschooling and worldschooling their two kids, demonstrating it is indeed possible to travel all over the world while giving your kids a solid education – “In a perfect world, I would spend our last year studying World War II history in Poland and Germany, followed by the trip to Southeast Asia that has been cancelled by the pandemic TWICE, stopover in New Zealand and Australia, and not miss out on Machu Picchu! I would force my whole family to study Spanish with more intensity and maybe even visit Guanajuato for Dia de los Muertos one last time…” I truly believe travelling is excellent to learn. For example, I was never a history person during high school but I certainly found it way more impactful to learn about WWI and WWII by walking through WWI trenches in Belgium and stepping foot inside a concentration camp.

Preet created a video on how to manage your emotions when the stock market is crashing.

The Fioneers got their campervan and wrote a very detailed post on why they chose Vanlife – “We love camping, immersing ourselves in the beautiful scenery, and being outdoors. We weren’t sure how comfortable we’d be with international travel in the near future, so we decided to go all-in on road-tripping, at least for the next few years. We know that we eventually wanted to do this, but the pandemic pushed the timeline earlier for us.”

Gean and Kristine from FIRE We Go discussed what to do with financial advisors, why they fired their financial advisor, and what questions you should ask if you want to hire a financial advisor.

Does financial independence mean giving up on work completely? Dave at Accidental Fire doesn’t think so. He thinks that Financial Independence is a hall pass for safe reinvention – “Why not just have a second career trying something totally different? Most of us are complex personalities with many interests, yet we often spend careers in just one field. Experiencing professional decline in your chosen field is just a queue to start the ball rolling on a new career. That’s what I did. I’m still in the muddy middle of pivoting from a long career in a pretty technical and stressful job for the Federal Government to being a solo-preneur producing and selling art and graphic designs.”

DGI&R explained Why you should use dividend yield as a valuation tool for stocks – “If you are looking for a reliable valuation tool, ideally you want one, like dividend yield, that has been shown to work for many decades and in all types of markets. Using dividend yield as a stock valuation tool seems to work and it’s been working for a long time. That said, no valuation method is perfect. When using dividend yield as a valuation tool there are 4 drawbacks to be aware of…“

I’ll wrap up this post with a great video from CBC explaining inflation and what’s really driving up prices.

Have a great weekend everyone!

Andrew did such an awesome job on the CBC story on inflation. Keeps it as concise and straight forward as possible on a complex subject. The humor and lay man terms helped too.

It was a great video, I enjoyed watching it.

Thanks for the great links.

I always prepare for the worst future scenario.

Bad news is now being a landlord in BC as Government limits rent increases to 1.5% a year yet inflation and mortgages are increasing massively and dramatically. Also government expanding ‘empty homes’ tax so it forces owners to rent their private property .

Luckily I just do passive investing.

Many people will have to rethink their FIRE ideas. I think people just hate their jobs so they want to FIRE.

My advice is to keep a job and career you like for decades as you’ll need the income and stability to eventually retire with your investments

Agree that the mentally of FIRE needs to change, I’ve been writing about that for years.

Inflation is a big problem for local businesses as it increases their input costs. It’s hard to say if a recession is coming, but I would bet we’ll see one sometime this year, if not in Canada then at least in the US.

One thing that’s definitely going to happen is home prices will fall here in Vancouver. But as Matt says the best time to buy investments is when prices are down. So maybe I’ll buy another rental property in 2023. Who knows. 🙂 Thanks for the mention and for being a very long time reader, lol.

You’re very welcome Liquid. Keep up the good work.

Can you explain the numbers behind this sentence? A 1333 monthly increase is huge.

“If you have a $500k mortgage, it may be hard to find an extra $1,333 per month to pay for the extra interests.”

Hi Dan,

Looks like I made a mistake and overlooked the chart from CBC. It said $16k more over 5 years with a $500k mortgage. I didn’t see the 5 year part. So it’d be extra $3,200 per year or $267 per month. I’ll fix in the article. Thanks for pointing this out.

Thank you for checking!

As always a great read, I guess I will have to get in touch with you and join your customers base for input on what to do next.

Thank you. Not sure what you meant by customer base, maybe you meant coaching?