June is here and we are finally getting summer weather in Vancouver. As you can see from pictures below, things are growing nicely in our garden. We are spending more and more time outside tending the garden and the yard. Baby T1.0 planted some peas and daikons in the garden in the spring and he is very excited about his growing plants.

When it comes to our stock investments, they take less time and attention compared to our garden & yard. For the most part, we have been putting our dividend portfolio on auto-pilot. We continue to buy dividend stocks whenever we see something at a discount and we continue to DRIP away on eligible stocks. Investment life is pretty simple this way.

The one thing I have been thinking lately is whether to trim down our portfolio holdings. As of today we own 72 dividend stocks and 2 index ETFs. I never had an “ideal number” in mind but perhaps 70+ individual dividend stocks is too many. We can probably consolidate a few positions. Does it make sense to hold the likes of Wal-Mart and Target given that online retailing is getting stronger and stronger? Maybe it’s time to sell Chevron and Kinder Morgan and forget about oil price recovery?

On the other hand, the benefit of having a portfolio with a large amount of stocks means we are not relying on one or two stocks for dividend income. What is your view on this on number of dividend stocks to hold? I would love to hear it.

May Dividend Income

In May 2017 we received dividend income from 25 companies:

- AbbView (ABV)

- Apple (AAPL)

- Pure Industrial REIT (AAR.UN)

- Bank of Montreal (BMO.TO)

- Corus Entertainment (CJR.B)

- Dream Office REIT (D.UN)

- Dream Global REIT (DRG.UN)

- Dream Industrial REIT (DIR.UN)

- Emera (EMA.TO)

- Enbridge Income Trust (ENF.TO)

- General Mills (GIS)

- H&R REIT (HR.UN)

- Inter Pipeline (IPL.TO)

- KEG Income Trust (KEG.UN)

- Kinder Morgan (KMI)

- National Bank (NA.TO)

- Omega Healthcare (OHI)

- Procter & Gamble (PG)

- Potash (POT.TO)

- Prairiesky Royalty (PSK.TO)

- RioCan REIT (REI.UN)

- Royal Bank (RY.TO)

- Smart REIT (SRU.UN)

- AT&T (T)

- Verizon (VZ)

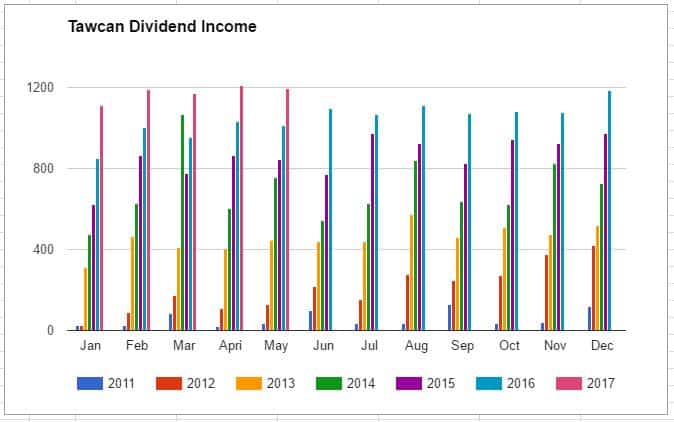

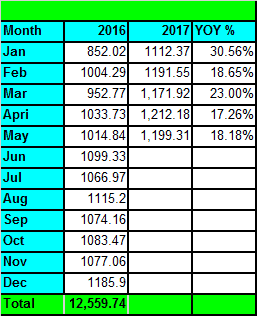

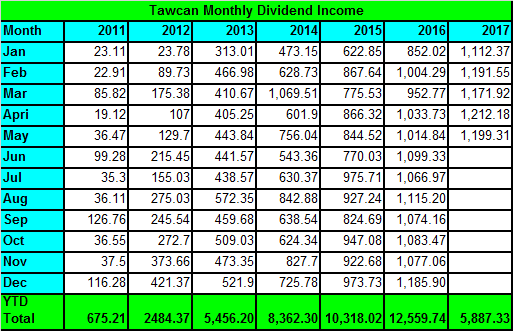

In total we received $1,199.31 in dividend income.

Ah, so close to $1,200, we were only off by $0.69! Oh well, hopefully we will cross the $1,200 mark again this month.

Out of the $1,199.29 dividend income that we received in May, $302.95 was in USD and $896.36 was in CAD. Please note, we use a 1 to 1 currency rate approach. Therefore, we do not convert dividends received in USD to CAD. We are ignoring exchange rate to keep the math simple. This is our way to avoid fluctuations in dividend income over time due to changes in the exchange rate.

The top 5 dividend payouts in May 2017 were Bank of Montreal, National Bank, Royal Bank, Omega Healthcare, and Procter & Gamble. The top 5 payouts accounted for 58.98% of our May dividend income.

Dividend Growth

Compared to May 2016 we saw a YOY growth of 18.18%. This performance matrix is a bit lower than expected. This is an indication that we need to work on adding more fresh capital to increase our dividend growth. Another area to focus on is owning stocks with high organic dividend growth. Rather than owning on high yield stocks with very little organic dividend growth, we should focus more on owning lower yield stocks with higher organic dividend growth.

After 5 months, we are tracking an overall 21.97% YOY growth rate. It would be great if we can continue to hold the overall YOY growth rate at above 20%.

Dividend Increases

In May a number of companies that we own in our portfolio announced dividend increases:

- Apple raised its dividend by 10.53% to $0.63 per share

- Hydro One raised its dividend by 4.76% to $0.22 per share

- Enbridge raised its dividend by 4.63% to $0.583 per share

- Telus raised its dividend 2.60% to $0.4925 per share

- Bank of Montreal raised its dividend 2.27% to $0.90 per share

- National Bank of Canada raised its dividend 3.57% to $0.58 per share

All the raises have increased our annual dividend income by $89.03.

Dividend Stock Purchases

In May we made one single purchase. We purchased 32 shares of Canadian Imperial Bank of Commerce (CM.TO). The purchase added $162.56 toward our annual dividend income.

CIBC currently has the lowest PE ratio out of all 5 major Canadian banks. This is mostly due to the uncertainties in the Canadian housing market and CIBC’s bid on PrivateBancorp. CIBC hiked up the bid for PrivateBancorp recently as an incentive to close the deal. I am optimistic that this deal will complete which will increase CIBC’s US exposure. While there are a lot of uncertainties in the short term, I believe CIBC will weather the storm and has a positive future outlook.

Summary

We had yet another great month for dividend income. It would have been nice to get over $1,200 in dividend income but we were very close regardless.

So far in 2017 we have received a total of $5,887.33 in dividend income. The plan is to hit $15,000 in dividend income for 2017. Therefore, we are slightly behind on this plan. However, this was a very ambitious plan/goal so if we close by end of the year, I would still be very happy.

Dear readers, how was your May dividend income?

There’s something so simple and pleasing to the eye with gardens. Maybe it’s the uniform way that you have to line crops up to make them grow better? I don’t know. Regardless, another great month for dividend income. While the number of holdings may be a little much in my opinion, you are right to wonder about whether consolidating will impact you with dividend payments. And at this time, if one company cuts, you’re okay. If you consolidate, it could be a bigger impact.

Not sure what Mrs. T did to make the crops grow so nicely, must be all the love and nutrients she’s putting in the garden. Will have to see about whether to consolidate some positions or not.

Hi pinch,

7% of my portfolio is cibc. That is sufficient for me for this company. My top 8 core stocks average 6 to 8% each of my portfolio. The rest of the stocks average 5% and less each.

My portfolio covers about 7 sectors.

Rn

I just love that dividend income graph – its such a great motivator to keep on investing!

Well, i only have a list of 21 canadian stocks, all dividend growth ones across different sectors (banks, insurance, telco, utlities, pipelines, consumer staple/discretionary, reits). I would like to add more stocks to my list but it’s hard to find stable dividend growth companies with good track records.

CIBC is at an attractive price now. I would have bought CIBC had I not already have quite a bit in my portfolio. Instead I bought some interpipeline shares.

RN

Hi RN,

How do you define ‘already have quite a bit’? How much money in % do you invest per stock/sector? How many sectors do your 21 stocks cover?

Regards, Pinch

Tawcan –

26 companies aka complete domination here! $1,200 is insane in an off-month, can’t imagine what June will be like. I believe you’ll end up being on target after two more months of dividend collection. Love the balance you have, keep it up as your income would more than cover my housing expenses!

-Lanny

Thanks Lanny, it would be nice if we were able to cut our expenses more so dividend income can cover more of our monthly expenses. 🙂

Tawcan, what nore can I say besides….HOLY FREKAING COW. Another great month in 2017 and the results continue to inspire me. Keep up the great work and keep on hustling. Love the garden as well. I’ll need some pointers from you haha

Bert

Hi Bert,

Thanks, glad to see that you shared my excitement. 😀

Great month! Those 2017 dividend numbers are outstanding!

Scott

Thanks Scott.

@pinchthepennies…on those numbers. Is that 24 holdings in combined in the tax advantaged pension account + 50 holdings in a non-pension account making it 74 holdings in total over two accounts?

Are there duplicate holdings (same stocks, ETF’s etc) in all accounts?

What is your average yearly dividend yield percentage across all accounts

IMO, a total combined 74 holdings is way too many.

I’d have problems with 10, possibly 5 maybe

Hi John,

Sorry, I thought that was clear from the post with the nunbers – but maybe it didn’t come out clear enough among all of those figures, apologies for that.

Pension: 24 holdings

Non-Pension: 50 holdings

Duplicated holdings across both accounts: 4

Pension forecast yield: 4.07%

Non-Pension forecast yield: 4.15%

On the topic of how many holdings to have I think we both have to agree to disagree.

Regards, Pinch

@PTP, thanks for replying & forgive it it was a dumb question, it’s just that the specific points in that last reply cleared it up for me…thanks

On your question to me…

As Bob the owner of this blog is aware, my/our situation is slightly different to most of those on the FI journey in that we are seniors fully retired aged 70. We are mortgage free. On an annual basis since 2012 every penny spent YOY is between 30%-33% of our annual joint income. We don’t have RRSP/RIFF (401K) these were meltdown prior to reaching age 65, we do have TFSA (Roth IRA). In the TFSA are just TWO (2) holdings which are the same ones that we’ve held since we retired in 2012 as seniors. The two positions were bought at the time discounted & yield double digits on the initial book value we bought them at & continue to do so to this day, they have never been DRIP or added to. If it ain’t broke, don’t mess with it is our moto. The market value of those two positions today is higher than their book value. We have till this year made the maximum annual contribution to the TFSA (Roth IRA) account. We shall no longer be doing this.

In a non-retirement/non-registered brokerage account there is always a small amount of cash sitting at the end of each year, which in the spring of each year we top to approx $50k +/- a few bucks to do a once a year pick/splurge (normally a one pick dividend stock with options), that we exit the position by the end of the year…always

Life is simple, investing is simple, our income is 99.9% guaranteed unless there is another depression. We have/keep in cash (real cash dollars) 7 years worth of expenses at all times.

Hi Bob,

That’s a good question you’re asking – What is your view on this on number of dividend stocks to hold? I am looking at it this way:

At some point in the future I want to be able to use the incoming dividends to pay for some/most/all of my living costs whether they be musts (food, utility bills) or would be nice to haves (how about a cruise every now and then?) or possible other future expenses (medical, care home) or anything in between.

Therefore I asked myself how much money (as a percentage) I would be prepared to lose out on if any of my holdings stopped paying dividends – regardless of the fact that I’d be replacing that lost income immediately with another dividend-paying holding and also may sell or keep the non-paying holding depending on how I judge their future prospects.

For me the answer is: between 3% and 5% of the total 100% of all dividends paid. With these numbers in mind I arrived at 20 holdings minimum up to 34 holdings for my portfolio. In the main part of my portfolio I am currently holding 34 holdings and I am fine with it. All but one stock are paying dividend and the one holding which isn’t currently paying will restart their dividend within the next 12 months.

However, if I had any family to look out for (wife, girlfriend, children) then I would accept even less loss of income thereby pushing the number of holdings required up a bit.

Regards, Pinch

Sorry, forgot to add some figures:

I am holding 2 tax-advantaged accounts one of which is a pension.

Pension account

24 holdings (1 ETF, 1 Fund, 22 individual stocks)

Pension dividend

Fund: accumulation units – no dividend payout,

1 indiv stock pays 2x per year,

ETF + all remaining indiv stocks pay 4x per year (quarterly)

Non-Pension account

Total holdings in account: 50 – breakdown below

High Yield portfolio: 34 individual stocks

HY dividend

6 indiv stocks pay quarterly dividend,

27 indiv stocks pay 2x per year,

1 indiv stock will restart dividend within 12 months

Non-High Yield: 16 holdings (1 ETF, 15 individual holdings)

N-HY dividend

ETF pays 4x per year (quarterly)

15 indiv stocks pay 2x per year

Regards, Pinch

Pinchthepennies,

I have 36 dividend paying stocks in my DGI portfolio, roughly equal weighted by income. I have been averaging around 8% organic dividend growth annually. It would take a major catastrophe for my YOY income to lessen. For this to transpire 3 of my holdings would have to completely suspend paying their dividends. OR, for the same effect, 6 of my holdings would have to cut their dividends by 50%. My policy is to sell and replace dividend cutters. On occasion I have sold dividend growth stocks I owned which did not raise their dividends over a 2 year period.

Hi Bernie,

Completely agree with you hence I am holding rather more stocks than the pure math suggests is necessary. However, I have seen portfolios with over 100 stocks and people still feeling uncomfortable about the impact a stopped dividend from one of their holdings may have.

That’s a good way to put it. I like the idea of between 3-5% per holding that would contribute to your dividend income. It’s way too much if a position is paying out 20+% of your total dividend income.

Excellent result, keep up the good work. Very much like watching your progress over the years. Keep up the excellent work, you are inspiration to people like myself. Cheers

Thank you very much for the encouragement.

Congrats on another fine month. Your dividends are growing as fast as your garden ;-).

Thanks, it’d be awesome if our dividends are growing as fast as the garden.

I just found your blog today! I always enjoy reading other Canadian finance blogs. Also congrats on another great month!

Are all your dividends currently being reinvested or do you use them to purchase other stocks?

Good luck the rest of the year!

PS – If you’d like to do a blogroll swap let me know 🙂

We DRIP whenever we are eligible. For dividend income that can’t be DRIP’ed, we wait till we have around $1,000 to purchase other stocks.

Great job growing your dividend over the years. Really impressive gain since 2011. Good record keeping too. My record is a mess…

Your garden is awesome. You must spend a lot of time on it. Very nice job.

Thanks Joe, we’ve been focusing a lot on our dividend income and it shows. 🙂

Hi Bob,

Have you written a post (or can you write a blog post) about where you hold your stocks or what is the best way to allocate your stocks? I see some of your dividends are US companies so I’m guessing the best place to hold those would be in non registered accounts while your BMO or Canadian dividends would be best held in a TFSA or RRSP? It would be great for those of us getting started if you could write a post on the best way to allocate your investments between non-reg, TFSA, and RRSP. Thanks!!

The Dividend FAQ has you covered. 🙂

https://www.tawcan.com/dividend-faq/

Excellent post, thanks!!

Nice dividends and nice garden too Bob! It’s absolutely flourishing. Our climates should be quite similar (we’re only a couple hours away from each other), but your garden is doing way better than ours.

What’s your secret?

Haha must be from the kids peeing in the garden lol (kidding!)

We put compost on the garden at beginning of the year, maybe that was the trick.

Impressive garden… That should yield well over the coming months. Yesterday, I ate our first raspberries…

The 1 k mark is clearly behind you now. Fingers crossed for the next one.

The downside of stock with higher growth yield might be that the short term dividend is lower and thus the short term you growth could temporary slow down.

We’ve been having strawberries here and there but the production will go through the roof soon! 🙂

Another very good month in dividend income and superb vegetable garden photos! The greenhouse / garden combo is brilliant.

Re number of stock holdings, DI is not my primary strategy, but with diversification benefits occurring mostly between the 12-20th holding, anything further perhaps add as incidental or opportunistic (e.g. a bargain price). Or, given there are about a dozen sectors, one might argue to hold a few equities from each, and be overweight in some thematic ones. Which would land a portfolio at around 40 stocks.

Perhaps as you’ve got quite a few holdings, just steadily trim as you see fit. Holding a small wad of cash to deploy and get a huge increase on YOC following the next bear market, seems to me a tantalising long term plan.

Those are some great numbers. Very well done.

Looking to hit $15K as well this year inside our non-reg. and TFSAs. I hope we can do it!

Cheers,

Mark

Thanks Mark. Looks like we are still behind you in terms of dividend income. 🙂

Looking good, almost hit that 1200.. 😉

As to the number of stock holdings in a portfolio, I don’t really believe you can set an ideal number on it. Selling stocks for the reason to trim it down, is not the best reason in my view. However if you think you the money that’s invested in certain stocks can give better returns when invested somewhere else, it makes perfect sense.

One of the things of portfolio management is to keep on evaluating and adjusting accordingly. I have not placed a number on dividend stocks to hold? But then again, I only have about twenty 😉

I’m curious of the steps you will make going forward, and how it will play out. Great update!

Yes so close on $1,200! Next month!

What you said about invest in stocks with better returns by selling existing current security is absolutely correct, that’s why I’m reconsidering about our holdings in the oil & gas sector.

Another month, another impressive total for passive income earned. Looks like you are still making those double digit year over year gains which just shows that you are still very much on the right path. Selling positions is never easy. While I don’t subscribe to an arbitrary number for total holdings in my portfolio I can understand you wanting to trim positions if a) you do not like their future prospects and b) it’s too much to manage. I guess my magic number is somewhere around 50 stocks but with many spin offs I’m still holding that number grew. Thanks for sharing. Awesome garden too!

Thanks Keith. You’re right, selling position is never easy but maybe some money in oil & retails are better going somewhere else. Will have to see what I can do. You’re right though, with spin offs, the number of holdings just get bigger. A number of the spin off shares I have aren’t huge, commission fee would be larger than 5% to sell the position.

Nicely done! You mentioned your YOY dividend income was 18.18%. Was this percentage enhanced with new money added in? If so, would you know what your organic DGR is over the same period?

Sorry I meant to say your YOY dividend income was “increased” by 18.18%.

I would say about ~60% of the growth is from new money added in. It would be interesting to do some deeper analysis on the organic DGR over the same period. Will have to see if I can write about it in the future.

Thanks for sharing. Ours was ok; like I said previously, bulk of my stuff is in ETF’s and Index Funds. So it’s between 2-3% div yield. The closer to 3% is from my emerging market allocation. Which is nice because it’s super low valuation as well. I feel like I’m double dipping =)

2-3% yield for ETFs is actually pretty decent. Congrats.

looking good – onward & upward, keep it building month after month. Not much I can add other than trim your holdings (72 is way too many) as well as learn how to ‘smartly hedge’ to get get an even higher dividend return rate.

Thanks, will have to look into “smartly hedging.” Like I said in the post, I don’t have an ideal number for our portfolio but maybe 72 + 2 index ETFs is too many.

Nice comparison of your garden and your stock portfolio! You have the garden I’ve been dreaming about. I don’t have any stocks, but I plan to plant something this summer. I can’t wait until I’m able to harvest the sweet fruit and green veggies!

It’s so fulfilling being able to eat veggies and herbs from our garden. It’s good to know it’s truly “organic”

Good job. Looks like you are solidly over 1000. If you can get close to 2000 this month you won’t be to far off. From your goal. Keep it up

Thanks we are solidly over $1,000 this year for sure. 🙂